CHAPTER 10 SCHEDULE M-1 AUDIT TECHNIQUES

Page 10-1

Chapter 10

Schedule M-1 Audit Techniques

By Ken Johnson (Central Mountain)

And

Alta Chesney, (Gulf Coast) and Fred Sanchez (Gulf Coast), Reviewers

INTERNAL REVENUE SERVICE

TAX EXEMPT AND GOVERNMENT ENTITIES

Table of Contents

TABLE OF CONTENTS ---------------------------------------------------------------------------------------------------------1

OVERVIEW ------------------------------------------------------------------------------------------------------------------------3

I

NTRODUCTION----------------------------------------------------------------------------------------------------------------------- 3

O

BJECTIVES--------------------------------------------------------------------------------------------------------------------------- 3

BASIC INFORMATION ---------------------------------------------------------------------------------------------------------4

L

INK OR BRIDGE --------------------------------------------------------------------------------------------------------------------- 4

S

CHEDULE M-1 DIFFERENCES ----------------------------------------------------------------------------------------------------- 4

4 G

ENERAL CATEGORIES ----------------------------------------------------------------------------------------------------------- 4

TIMING DIFFERENCES--------------------------------------------------------------------------------------------------------5

T

IMING DIFFERENCES --------------------------------------------------------------------------------------------------------------- 5

PERMANENT DIFFERENCES ------------------------------------------------------------------------------------------------5

P

ERMANENT DIFFERENCES--------------------------------------------------------------------------------------------------------- 5

SCHEDULE M-1 MECHANICS -----------------------------------------------------------------------------------------------6

S

CHEDULE M-1 ---------------------------------------------------------------------------------------------------------------------- 6

D

ISCUSSION OF SCHEDULE M-1 --------------------------------------------------------------------------------------------------- 7

S

CHEDULE M-1 PRINCIPLES -------------------------------------------------------------------------------------------------------- 7

SCHEDULE M-1 LINE ITEMS ------------------------------------------------------------------------------------------------8

L

INE 1 --------------------------------------------------------------------------------------------------------------------------------- 8

L

INE 2 --------------------------------------------------------------------------------------------------------------------------------- 8

L

INE 3 --------------------------------------------------------------------------------------------------------------------------------- 8

L

INE 4 --------------------------------------------------------------------------------------------------------------------------------- 9

L

INE 5 -------------------------------------------------------------------------------------------------------------------------------- 10

L

INE 6 -------------------------------------------------------------------------------------------------------------------------------- 10

L

INE 7 -------------------------------------------------------------------------------------------------------------------------------- 11

L

INE 8 -------------------------------------------------------------------------------------------------------------------------------- 11

L

INE 9 -------------------------------------------------------------------------------------------------------------------------------- 11

L

INE 10 -------------------------------------------------------------------------------------------------------------------------------11

Continued on next page

CHAPTER 10 SCHEDULE M-1 AUDIT TECHNIQUES

Page 10-2

Table of Contents, Continued

AUDITING TECHNIQUES --------------------------------------------------------------------------------------------------- 12

M

ECHANICAL ERRORS ------------------------------------------------------------------------------------------------------------- 12

B

OOK EXPENSE NOT ON TAX RETURN------------------------------------------------------------------------------------------- 13

N

ETTING ITEMS --------------------------------------------------------------------------------------------------------------------- 13

S

IMPLE MISTAKES ------------------------------------------------------------------------------------------------------------------ 13

O

MITTED ITEMS --------------------------------------------------------------------------------------------------------------------- 13

FASB'

S ------------------------------------------------------------------------------------------------------------------------------- 13

C

ONSISTENCY ----------------------------------------------------------------------------------------------------------------------- 13

A

DJUSTING JOURNAL ENTRIES --------------------------------------------------------------------------------------------------- 14

I

NCORRECT ACCOUNT BALANCES ----------------------------------------------------------------------------------------------- 14

R

EVERSING DIFFERENCES --------------------------------------------------------------------------------------------------------- 14

SAMPLE IDR'S ------------------------------------------------------------------------------------------------------------------ 15

E

XHIBIT 1 ---------------------------------------------------------------------------------------------------------------------------- 15

E

XHIBIT 2 ---------------------------------------------------------------------------------------------------------------------------- 15

E

XHIBIT 3 ---------------------------------------------------------------------------------------------------------------------------- 16

EMPLOYEE PLANS SCHEDULE M-1'S ---------------------------------------------------------------------------------- 16

D

EFERRED COMP. ARRANGEMENTS--------------------------------------------------------------------------------------------16

Q

UALIFIED PLAN IRC 404(A)(5) ------------------------------------------------------------------------------------------------- 16

N

ONQUALIFIED DEFERRED COMP. PLANS IRC 404(A)(6) ------------------------------------------------------------------- 17

C

OMP. ABSENCES IRC 404(A)(5) ----------------------------------------------------------------------------------------------- 18

SUMMARY ----------------------------------------------------------------------------------------------------------------------- 19

S

UMMARY --------------------------------------------------------------------------------------------------------------------------- 19

SCHEDULE M-1 EXAMPLE ------------------------------------------------------------------------------------------------- 20

T

AX RETURN ------------------------------------------------------------------------------------------------------------------------ 20

L

INE 1 -------------------------------------------------------------------------------------------------------------------------------- 20

L

INE 2 -------------------------------------------------------------------------------------------------------------------------------- 20

L

INE 3 -------------------------------------------------------------------------------------------------------------------------------- 20

L

INE 4 -------------------------------------------------------------------------------------------------------------------------------- 21

L

INE 5 -------------------------------------------------------------------------------------------------------------------------------- 21

L

INE 6 -------------------------------------------------------------------------------------------------------------------------------- 21

L

INE 7 -------------------------------------------------------------------------------------------------------------------------------- 21

L

INE 8 -------------------------------------------------------------------------------------------------------------------------------- 22

L

INE 9 -------------------------------------------------------------------------------------------------------------------------------- 22

L

INE 10 -------------------------------------------------------------------------------------------------------------------------------22

R

ECONCILE LINE 24 OF FORM 1120 TO THE EMPLOYER’S SET OF BOOKS ------------------------------------------------- 22

E

XPLANATION----------------------------------------------------------------------------------------------------------------------- 23

L

INE 4 -------------------------------------------------------------------------------------------------------------------------------- 23

SCHEDULE M-1 RECONCILIATION ------------------------------------------------------------------------------------- 24

S

TOCK OPTIONS 1,409,395 ------------------------------------------------------------------------------------------------------ 24

CHAPTER 10 SCHEDULE M-1 AUDIT TECHNIQUES

Page 10-3

Overview

Introduction

Taxpayers have different objectives when they prepare the financial

statements and when they complete their tax return. The financial statements

are prepared with an objective of maximizing income and thus increasing the

net worth of the shareholders, while maintaining conformity with GAAP.

The tax return is prepared with the objective of minimizing taxable income

and thus reducing taxes paid, while maintaining compliance with tax law.

The books and records of a corporation are kept in accordance with GAAP

and not in accordance with tax law. The result of these differing objectives is

a large disparity between book income and taxable income. Schedule M-1 is

the bridge (reconciliation) between the books and records of a corporation and

its income tax return. Items included on this schedule will not be found in the

corporate books and must be analyzed from workpapers prepared by the

taxpayer.

Objectives

At the end of this chapter, you will be able to:

· Compute taxable income using book income and Schedule M-1;

· Identify potential issues by analyzing Schedule M-1, and;

· List some audit procedures for Schedule M-1.

CHAPTER 10 SCHEDULE M-1 AUDIT TECHNIQUES

Page 10-4

Basic Information

Link or Bridge

Schedule M-1 of the Corporate Income Tax Return, Form 1120 is the link or

bridge between financial accounting and tax reporting. The tax return is

prepared after completing Schedule M-1 adjustments. Understanding

Schedule M-1 is a crucial part of the examination of a corporate income tax

return.

Schedule M-1

Differences

As mentioned previously, there are different rules for determining the

taxpayer’s financial income under GAAP and for determining taxable

income. These rules result in differences that can be:

· Timing differences that are reported for tax purposes in a different

accounting period, and;

· Permanent differences that are never reported for tax purposes.

4 General

Categories

Both types of differences result in M-1 adjustments which fall into four

general categories:

· Income subject to tax but not recorded on the books this year;

· Expenses recorded on the books this year but not deducted on this return;

· Income recorded on the books this year but not included on this return, and;

· Deductions on the tax return but not charged against book income this year.

Most of the GAAP and tax differences fall into one of the four general

categories. Schedule M-1 adjustments are found in the taxpayer’s supporting

workpapers for nearly every line item.

For consolidated returns, you will also need to analyze separately the M-1

entries for each member of the controlled group. The principles covered in

this lesson thus apply to all entities regardless of form.

CHAPTER 10 SCHEDULE M-1 AUDIT TECHNIQUES

Page 10-5

Timing Differences

Timing

Differences

Timing differences occur because tax laws require the recognition of some

income and expenses in a different period than that required for book

purposes. Timing differences originate in one period and reverse or terminate

in one or more subsequent periods.

There are four basic categories of timing differences:

· Income recognized in financial statements before it is taxable;

· Income taxable before it is recognized in financial statements;

· Expenses recognized in financial statements before they are deducted on the

tax return, and;

· Expenses deducible on the tax return before they are recognized on

financial statements.

Permanent Differences

Permanent

Differences

Permanent differences between book and tax income result from transactions

that (under applicable tax laws and regulations) will not be offset by any

corresponding differences in other periods.

If a permanent Schedule M-1 difference is missed on an examination, it will

be lost forever. If a timing difference is missed, there will likely be no

permanent loss of tax revenue.

CHAPTER 10 SCHEDULE M-1 AUDIT TECHNIQUES

Page 10-6

Schedule M-1 Mechanics

Schedule M-1

Schedule M-1 Reconciliation of Income (Loss) per Books With Income per

Return

1.Net income (loss) per books

2 Federal income tax

3.Excess of cap losses over cap gains

4.Income subject to tax not recorded on books this year (itemize):

5.Expenses recorded on books this year not deducted on this return

(itemize):

a. Depreciation $________ b. Contributions

carryover $________ c. Travel and

entertainment $_______

____________________________________________

6.Add lines 1 through 5

7.Income recorded on books this year not included on this return (itemize):

Tax-exempt

Interest $___________

8.Deductions on this return not charged against book income this year

(itemize)

a. Depreciation $______ b. Contributions

carryover. $______

________________________________________

9.Add lines 7 and 8

10.Income (line 28,

page 1) line 6 less 9

Continued on next page

CHAPTER 10 SCHEDULE M-1 AUDIT TECHNIQUES

Page 10-7

Schedule M-1 Mechanics, Continued

Discussion of

Schedule M-1

When looking at the Schedule M-1, line items in the left hand column (lines

2-5) are adjustments added to book income. This results in an increase to

taxable income. Line items in the right hand column (lines 7-8) are

adjustments reducing book income. Lines 7-8 decrease taxable income.

Taxpayers may show negative amounts on Schedule M-1. These have the

opposite effect on taxable income than that described above. Although

correct, negative amounts can be confusing when determining whether

income is increased or decreased.

Line items 4 and 8 of the Schedule M-1 contain items that appear on the tax

return but not on the books.

Line items 5 and 7 of the Schedule M-1 start with items on the books that are

then adjusted for tax purposes. These items appear on the financial

statements but will not be on the tax return.

Be alert for taxpayers combining multiple Schedule M-1 adjustments and be

aware that large amounts may be offset. On the surface, the net figure might

not warrant examination.

Schedule M-1

principles

The principles described above can be summarized as follows:

ITEMS--PLUS ITEMS-MINUS

Book Income (Starting Point)

Federal Income Tax Book Income not on Tax Return

Net Capital Loss Expenses for Tax not in the Books

Taxable Income not on the Books Book Expenses not on Tax Return

Taxable Income (Ending Point)

CHAPTER 10 SCHEDULE M-1 AUDIT TECHNIQUES

Page 10-8

Schedule M-1 Line Items

Line 1

Schedule M-1 starts with the net income per books (after the deduction for

income tax expense) as shown in the corporation’s profit or loss account. The

amount should be taken from the actual books, not from a set of workpapers.

Frequently, taxpayers will use an income amount that does not appear in the

company books, the annual report, or the financial statements. These

taxpayers have “off-book” adjustments, which do not appear on the Schedule

M-1. Any “off-book” adjustments should be closely scrutinized for potential

tax issues.

Line 2

The provisions for federal income tax (line 2 of Schedule M-1) should be

compared with the federal tax liability on Schedule J on Form 1120. Line 2

of Schedule M-1 represents the current federal tax provision for the book

income amount of the current year plus the deferred tax provision, which

recognizes future obligations and contingencies. Line 10 of Schedule J is the

net federal tax amount on taxable income of the current year.

An analysis of line 2 is important because the deferred tax liability should

include cumulative deferred adjustments. Deferred taxes are created by

timing differences that will eventually be reported on Schedule M-1. We will

discuss the deferred tax liability in more detail in another lesson when we

look at FASB 109, which deals with accounting for income taxes.

Line 3

This represents a timing difference since capital losses can be deducted on the

books. Under IRC section 1211, capital losses can only be deducted to the

extent of capital gains. The excess capital loss can be carried back three years

and forward five years for tax purposes. There is no limitation on losses

expensed for book purposes.

Continued on next page

CHAPTER 10 SCHEDULE M-1 AUDIT TECHNIQUES

Page 10-9

Schedule M-1 Line Items, Continued

Line 4

This line restores to taxable income those items, which because of timing or

other generally acceptable accounting provisions, have either:

· Been previously reported,

· Been used to reduce a balance sheet item, or

· Will be reported in some subsequent period.

Prepaid rental income is a good example. Advanced rents are timing

differences, which, for tax purposes, are included in taxable income in the

year of receipt, but are reported in the period earned for book purposes.

Prior year income represents an item included as book income in a prior year

but taxed in the current year. For example, insurance proceeds in excess of

basis on an involuntary conversion may not have been reinvested within the

prescribed time period. Treasury Regulation 1.1033(a)-2(c)(2) requires that

the tax liability for the year for which the election was made to be recomputed

if the converted property is not replaced within the required period of time.

Continued on next page

CHAPTER 10 SCHEDULE M-1 AUDIT TECHNIQUES

Page 10-10

Schedule M-1 Line Items, Continued

Line 5

This line contains both permanent and timing differences. Some of the more

common entries on this line are listed below.

· Book depreciation that exceeds the amount allowed for tax will be shown in

this section.

· Reserves for future expenses, which are not currently deductible for tax, are

a common entry on line 5.

· Expenses incurred to earn tax-exempt income are not allowed as a

deduction in the computation of taxable income. An analysis of

professional services account may indicate expenses incurred for the

production of tax-exempt income.

· Contributions in excess of the 10% of taxable income limitation would

result in a timing adjustment in this section.

· Officer’s life insurance premiums are not allowed as a deduction for tax

purposes in certain situations, but would be reflected as a book deduction.

For example, a company may maintain a life insurance policy on the life of

its CEO and other top management in which the company is named as

beneficiary. For book purpose, the premiums are expensed as incurred

(usually as insurance expense). If the policy provides for a cash surrender

value, the portion of the premium that relates to cash surrender value is

recorded as an asset. For tax purposes, under IRC 264(a)(1), no deduction

is allowed for premiums paid on any life insurance policy covering the life

of any officer/employee when the company is directly or indirectly the

beneficiary of the policy.

· The conservatism principle in accounting requires companies to recognize

liabilities when they become probable. Provisions for estimated expenses

are established for book purposes as contingencies, but they are not allowed

for tax purposes until they become fixed and determinable.

Line 6

This is the sum of lines 1 through 5.

Continued on next page

CHAPTER 10 SCHEDULE M-1 AUDIT TECHNIQUES

Page 10-11

Schedule M-1 Line Items, Continued

Line 7

The books may reflect current income for financial reporting while deferring

the item for tax purposes. This line also includes financial income not subject

to tax.

Examples include:

· Tax-exempt interest on municipal bonds,

· Officer's life insurance proceeds (since the premiums are not deductible,

income from the policy is exempt from tax), and

· Installment receipts, which show up as deferred gross profit on line 7.

Line 8

This includes all deductions claimed for tax purposes that are not recorded in

the corporation’s books. This is the opposite of line 5.

Examples include:

· Depreciation is the most common example. Generally, taxpayers are

allowed to use accelerated depreciation for tax purposes while using the

straight-line method for book purposes.

· The excess contribution carryover (not allowed as a deduction for tax

purposes in prior years) appears here as a timing difference.

Line 9

This is the sum of lines 7 and 8.

Line 10

This is line 6 minus line 9 and is the actual taxable income reported on Line

28 of page 1 of the income tax return. You should investigate any difference

between the amount reported on line 10 of the M-1 and line 28 of page 1.

CHAPTER 10 SCHEDULE M-1 AUDIT TECHNIQUES

Page 10-12

Auditing Techniques

Step Action

1 Request the workpapers and supporting documents used to prepare

the tax return, and reconcile the book income shown on line 1 of

the Schedule M-1 to the actual net profit or loss.

2 Reconcile the federal income tax on line 2 of the Schedule M-1 to

the amount reported on the books. (This amount includes current

and deferred taxes).

3 Secure a comparative analysis of each Schedule M-1 adjustment,

comparing the current year(s) Schedule M-1 to the prior and

subsequent years’ Schedule M-1. (See Exhibit 2-3).

4 Prepare workpapers to verify the propriety and accuracy of all

Schedule M-1 adjustments.

5 Secure all pertinent documentation to substantiate the computation

of the entries including:

· Books of original entry,

· Audited financial statements,

· Audit workpapers or schedules, and

Source documents such as invoices, contracts, agreements, etc.

6 Review book balance sheet and book profit and loss accounts for

possible omissions from Schedule M-1 increases to income.

7 Develop a list of expected items to be included on Schedule M-1.

Ask the taxpayer to explain the accounting treatment for such

items, for book and tax purposes, if the expected items are not

listed on Schedule M-1.

Mechanical

Errors

The entries on Schedule M-1 are not part of the taxpayer’s double-entry

accounting system. The normal accounting controls do not exist and

consequently, errors are frequent. An item may be deducted on the books and

then deducted again erroneously on Schedule M-1. Many times, numbers

will be transposed resulting in an erroneous adjustment. Seemingly innocent

adjustments have yielded large audit issues.

Continued on next page

CHAPTER 10 SCHEDULE M-1 AUDIT TECHNIQUES

Page 10-13

Auditing Techniques, Continued

Book Expense

not on Tax

Return

It is important to investigate expenses not deducted on the return. An expense

per books but not on the return could result in an incorrect amount on the

Schedule M-1. For Example, a $5,000 amount on line 4 or 5 does not mean

that the amount should not be $500,000. Review the accounts and account

numbers to determine if the taxpayer handled them correctly.

Netting Items

The taxpayer may inadvertently disguise the significance of the Schedule M-1

adjustment by combining or netting items, which would normally be reported

as a separate line item. Although there may not be an adjustment to income,

it does distort a realistic analysis of the Schedule M-1. Separately, an item

may stand out as an improper item.

Simple

Mistakes

Finding simple mistakes, like a Schedule M-1 entry on the wrong side of

Schedule M-1, often results in quick agreed adjustments. If a $300,000

Schedule M-1 entry for unallowable travel and entertainment was erroneously

made to decrease taxable income, there is a $600,000 adjustment.

Omitted Items

Omitted Schedule M-1 items can be found by investigating balance sheet

accounts (especially liabilities), which are not affected by Schedule M-1

adjustments on the tax return. Based on the titles to these accounts and other

information developed in the audit, determine if a book and tax difference

exists. The taxpayer often misses new general ledger accounts that should be

included in M-1 adjustments.

FASB's

There are numerous Financial Accounting Standards Board (FASB)

statements, which result in Schedule M-1 adjustments.

Consistency

For examinations involving a consolidated return or examination of separate

returns in the same industry, you should compare similar Schedule M-1

entries and similar trial balance accounts between the various companies.

Continued on next page

CHAPTER 10 SCHEDULE M-1 AUDIT TECHNIQUES

Page 10-14

Auditing Techniques, Continued

Adjusting

Journal Entries

Understanding adjusting journal entries (AJEs) and reclassification entries is

a vital part of examining a taxpayer’s books and may lead to Schedule M-1

adjustments. The following example shows how.

A taxpayer made the following year-end Adjusting journal entries (AJE):

Debit. Cost of Goods Sold $1,000,000

Credit. Inventory $1,000,000

The net effect of this AJE decreases net income. The taxpayer claims the AJE

was made to revalue discontinued or obsolete items due to financial

accounting requirements. For tax purposes, the revaluation is determined not

to be deductible. Therefore, a Schedule M-1 adjustment on line 5 should

appear on the tax return in the amount of $1,000,000.

Incorrect

Account

Balances

Examiners should look for Schedule M-1 entries that were computed by

reference to incorrect account balances. This can occur when the Schedule

M-1 entry was computed using book account balances believed to be accurate

but later altered by year-end adjusting journal entries. Additionally, look for

Schedule M-1 entries computed by reference to book account balances that

included adjusting entries not applicable to the year under examination.

Incorrect account balances can be illustrated as follows:

Current Year’s Adjusting Journal Entry Ignored

1998 1999

Tax depreciation $2,225,000 $2,219,000

Less Book Depreciation $1,118,000* $1,115,000

Taxpayer’s Sch. M-1 $1,107,000 $1,104,000

Correct Schedule M-1 $1,207,000 $1,104,000

Adjustment $100,000

*The 1998 book depreciation was actually $1,018,000 after a $100,000 credit in a 1998 year-end

adjusting journal entry

Reversing

Differences

It is important to remember that timing differences will reverse in subsequent

periods.

CHAPTER 10 SCHEDULE M-1 AUDIT TECHNIQUES

Page 10-15

Sample IDR's

Exhibit 1

Exhibit 1 is an example or template of an IDR requesting specific Schedule

M-1 information. A description of the documents requested follows.

· Please provide the consolidating tax assembly or tax grouping workpapers

that were prepared to arrive at the amount reflected for book income on

Schedule M-1, line 1.

· Please provide the reconciliation of the book income amount reflected on

Schedule M-1, line 1 to the net earnings amount reflected in the

consolidated statement of earnings prepared by the independent auditors.

· Indicate those entities, which were added to, or deleted from, the book

income amount in going to the statement of earnings amount.

Alternatively, indicate those entities, which were deleted from, or added to

the statement of earnings amount in going to the book income amount.

· Provide all journal entries, which were prepared in determining the

statement of earnings amount.

Exhibit 2

Exhibit 2 is an example or template of an IDR requesting Schedule M-1

information by line item. A description of the documents requested follows.

Please provide the workpapers, schedules, and other such information which

was used to prepare the following Schedule M-1 entries:

· Line 4 Entries: (List items here)

· Line 5 Entries: (List items here)

· Line 7 Entries: (List items here)

· Line 8 Entries: (List items here)

Continued on next page

CHAPTER 10 SCHEDULE M-1 AUDIT TECHNIQUES

Page 10-16

Sample IDR's, Continued

Exhibit 3

Exhibit 3 is an example or template of an IDR requesting information

regarding Schedule M-1 entries that may have been combined. A description

of the documents requested follows.

It would appear that line item entries on Schedule M-1 (lines 4, 5, 7, 8)

represent account information by the same name and description. To the

extent a Schedule M-1 entry actually represents a combination of accounts

and amounts of different names and descriptions, it will be necessary to

provide information and other data in support of such a Schedule M-1 entry.

Employee Plans Schedule M-1's

Deferred

Comp.

Arrangements

Deferred compensation arrangements can take many forms: qualified pension

and profit-sharing plans, incentive stock options, stock purchase plans,

nonstatutory stock options and nonqualified deferred compensation

agreements. For tax purposes, the timing of an employer deduction depends

on whether the plan is qualified under IRC 401.

Qualified Plan

IRC 404(a)(5)

A pension plan is an arrangement whereby an employer provides benefits

payments to employees after they retire. Because a pension is viewed as a

form of deferred compensation, it follows that the cost of the pension occurs

over the period that the employees provide services to the employer.

For book purposes, under FASB No. 87 and FASB No. 88, as the employees

work, pension expense is incurred and the company's liability increases. The

computation of pension cost is very complicated because it is a function of a

number of factors including service cost, interest, prior service costs, net gain

or loss on the value of plan assets and the actual return on plan assets.

Continued on next page

CHAPTER 10 SCHEDULE M-1 AUDIT TECHNIQUES

Page 10-17

Employee Plans Schedule M-1's, Continued

Qualified Plan

IRC 404(a)(5)

(continued)

For tax purposes, under IRC 404, a deduction is allowed for employer

contributions to a pension, profit-sharing or stock bonus plan that meet the tax

qualification rules of IRC 401, generally in the year in which paid to the plan,

subject to limitations determined under IRC 412. Under IRC 412, minimum

and maximum funding limits are determined. Any contribution in excess of

the maximum funding would be deferred and deducted in a subsequent year.

Under IRC 404(a)(6), a contribution for a qualified plan made after the close

of the taxable year is deemed made on the last day of the year if:

· it is made on account of such year and

· not later than the due date (including extensions) for the

employer's income tax return due for such year.

NonQualified

Deferred

Comp. Plans

IRC 404(a)(6)

In addition to, or in lieu of a qualified plan, a company may maintain

nonqualified deferred compensation agreements, also referred to as unfunded

deferred compensation. An unqualified plan does not require that an amount

be set aside to irrevocably fund the benefits for the employee. For example, a

company may pay cash bonuses to certain sales and management personnel.

The awards may be based on sales volume, sales quotas, etc. Subsequent to

the year in which the awards are earned, the company determines the exact

amount of the bonuses and pays the recipients.

For book purposes, under APB Opinion No. 12, deferred compensation is

expensed in the year earned by the recipients based on management's estimate

of the future liability. If long-term, the compensation must be accrued in a

systematic and rational manner over the period of active employment starting

with the contract date.

For tax purposes, under IRC 404(a)(5), cash bonus awards are considered to

be nonqualified deferred compensation, deductible in the taxable year in

which the compensation is included in the recipient's gross income.

However, Temp. Reg. 1.404(b)-1(T) provides that compensation paid to an

employee within two and one half (2 ½) months after the end of the

employer's taxable year in which it is earned is not considered to be deferred

compensation and is allowed as a deduction in the year in which it is earned.

Continued on next page

CHAPTER 10 SCHEDULE M-1 AUDIT TECHNIQUES

Page 10-18

Employee Plans Schedule M-1's, Continued

Comp.

Absences IRC

404(a)(5)

A compensated absence is an absence from employment due to vacation,

holiday, or illness for which it is expected that the employee will be paid. A

vested right exists when an employer has an obligation to make payment to an

employee even if that employee terminates. Accumulated rights are those

rights that can be carried forward to future periods if not used in the period in

which earned.

For book purposes, FASB No. 43 requires that a liability be accrued for the

cost of compensation for future absences where (1) the obligation relates to

services already rendered; (2) the rights vest or accumulate; (3) payment is

probable; and (4) the amount can be reasonably estimated. For tax purposes,

under IRC 404(a)(5), vested vacation pay that is paid more than two and one

half (2 ½) months after taxable year-end is treated as deferred compensation

and deducted when paid. Vested vacation pay paid during the year or within

two and one half (2 ½) months after taxable year-end is deducted currently.

Accordingly, the amount of the vacation pay accrual account at year-end over

the amount of the preceding year's accrued vacation pay account at year-end

results in an increase or decrease in the portion of the vacation pay accrual

that is not deductible for tax purposes.

One of the issues currently being pursued involves an arrangement whereby

the taxpayer purchases a letter of credit (or other similar financial instrument)

within two and one half (2 ½) months after the end of the taxable year in the

amount of the unpaid accrual at the time the letter of credit is purchased. The

taxpayer argues that this constitutes payment of the accrual for purposes of

accelerating the entire amount of the accrual as a deduction in the preceding

taxable year. It is the Government’s position that the purchase of the letter of

credit does not constitute payment of the benefits for purposes of avoiding the

application of the 2 ½-month rule.

Although the Tax Court rendered an adverse decision to the Government in

Schmidt Baking Company, 107 T.C. 271 (1996), the Service has NOT

acquiesced in this case. Therefore, examiners should NOT be conceding this

issue. It should also be noted that Congress introduced in 1998 specific

legislation to overturn the effects of the Schmidt decision, and has been

adopted in the Revenue Reconciliation Act of 1998 for years beginning after

7-20-98.

CHAPTER 10 SCHEDULE M-1 AUDIT TECHNIQUES

Page 10-19

Summary

Summary

You have learned in this chapter the comprehensive analysis of Schedule M-

1. It is imperative that you understand the differences between income and

expenses based on accounting principles that generate book income, and tax

laws, which generate taxable income.

The following key points were covered in this lesson:

· Schedule M-1 links the books to the tax return,

· Timing differences originate in one period and reverse in one or more

subsequent periods,

· Permanent differences do not reverse in other periods,

· Auditing techniques include verifying net profit or loss reported on

financial statements, performing comparative analyses, and substantiating

significant M-1 entries,

· Tracing reserve accounts to M-1 entries is an excellent source for potential

audit adjustments, and

· Timing differences result in M-1 entries that must be reversed in subsequent

periods.

CHAPTER 10 SCHEDULE M-1 AUDIT TECHNIQUES

Page 10-20

Schedule M-1 Example

Tax Return

Look to pages 22 through 25 for a copy of the tax return. Page 2 of the Form

1120 is not included because there was no cost of sales.

Line 1

In our example, Net Income (Loss) Per Books is $27,358,158. The EP Agent

verified the figure by reviewing the certified Financial Statement for the

period ended December 31, 2001.

Although this information was not provided as part of the tax return, the EP

Agent verified the pension expense per the certified Financial Statement for

the period ended December 31, 2001 as $6,246,075. A summary of the

various book accounts that make up the total of $6,246,075 requested and

provided as well.

Line 2

In our example, Federal Income Tax is $2,779,405. The provisions for

Federal Income Tax should be compared with the federal tax liability on

Schedule J on Form 1120.

Line 2 of Schedule M-1 represents the current federal tax provision for the

book income amount of the current year plus the deferred tax provision,

which recognizes future obligations and contingencies. Schedule J is where

the net federal tax amount on taxable income of the current year is computed.

Line 3

In our example, there were no Excess Capital Losses Over Capital Gains.

Excess Capital Losses Over Capital Gains represents a timing difference since

capital losses can be deducted on the books. Under IRC section 1211, capital

losses can only be deducted to the extent of capital gains. The excess capital

loss can be carried back three years and forward five years for tax purposes.

There is no limitation on losses expensed for book purposes.

Continued on next page

CHAPTER 10 SCHEDULE M-1 AUDIT TECHNIQUES

Page 10-21

Schedule M-1 Example, Continued

Line 4

In our example, Income Subject to Tax Not Recorded On Books This Year is

$94,846,491. This line restores to taxable income Deferred Intercompany

Gain, Gain on Sale of Asset, and Section 420 Transfer - Cash Balance Plan

per Statement 1 attached to Form 1120.

The Deferred Intercompany Gain is from the sale of an asset to a party

outside the consolidated group upon which an intercompany gain had been

reported for financial purposes in previous years. The Gain on Sale of Asset

is necessary due to accelerated depreciation for tax deduction purposes.

The item that would concern the EP Agent would be the Section 420 Transfer

- Cash Balance Plan entry of $4,646,938 that could impact Line 24 (pension

expense) on Form 1120.

Line 5

In our example, Expenses Recorded On Books This Year Not Deducted On

This Return is $51,701,102. This line restores to taxable income

Depreciation, Charitable Contributions, Travel and Entertainment, and other

miscellaneous items detailed on Statement 1 attached to Form 1120.

It is common to reverse the entire amount of depreciation. It is also possible

to net book and tax depreciation, which would result in only one Schedule M-

1 adjustment for depreciation. In this case, the entire amount of book

depreciation was reversed. The adjustment to Travel and Entertainment and

Charitable Contributions is necessary due to tax limitations on the deduction.

None of these expenses would appear to impact Line 24 (pension expense) on

Form 1120.

Line 6

In our example, the subtotal of Lines 1 through 5 is $176,685,156.

Line 7

In our example, Income Recorded On Books This Year Not Included On This

Return is $390,476. Per Statement 1 attached to Form 1120, this represents

unearned income that reduces taxable income and would not appear to impact

Line 24 (pension expense) on Form 1120.

Continued on next page

CHAPTER 10 SCHEDULE M-1 AUDIT TECHNIQUES

Page 10-22

Schedule M-1 Example, Continued

Line 8

In our example, Deductions On This Return Not Charged Against Book

Income This Year is $168,644,298. Tax Depreciation is adjusted here and

since tax and book depreciation were not netted, this adjustment reconciles to

Line 20 (depreciation expense) on Form 1120.

Per Statement 1 attached to Form 1120, many miscellaneous items reduce

taxable income. The only item that would appear to impact Line 24 (pension

expense) on Form 1120 would be the Additional Pension Expense of

$250,000 for funding of a 401(h) account.

Line 9

In our example, the subtotals of Lines 7 and 8 is $169,034,774.

Line 10

In our example, Income Per the Tax Return on Line 28 on Form 1120 is the

difference between Lines 6 and 9 and is $7,650,382.

You should investigate any difference between the amount reported on Line

10 of Schedule M-1 and Line 28 on Form 1120.

Reconcile Line

24 of Form

1120 to the

Employer’s set

of books

In our example, Line 24 on Form 1120 is $1,849,137. We also determined

when reviewing Line 1 on Schedule M-1 that book income was $6,246,075

for that same line item when various accounts were rolled up together.

Using Schedule M-1 adjustments that only impact Line 24 (pension expense)

on Form 1120, the pension plan expense per books can be reconciled to the

pension plan expense per the tax return.

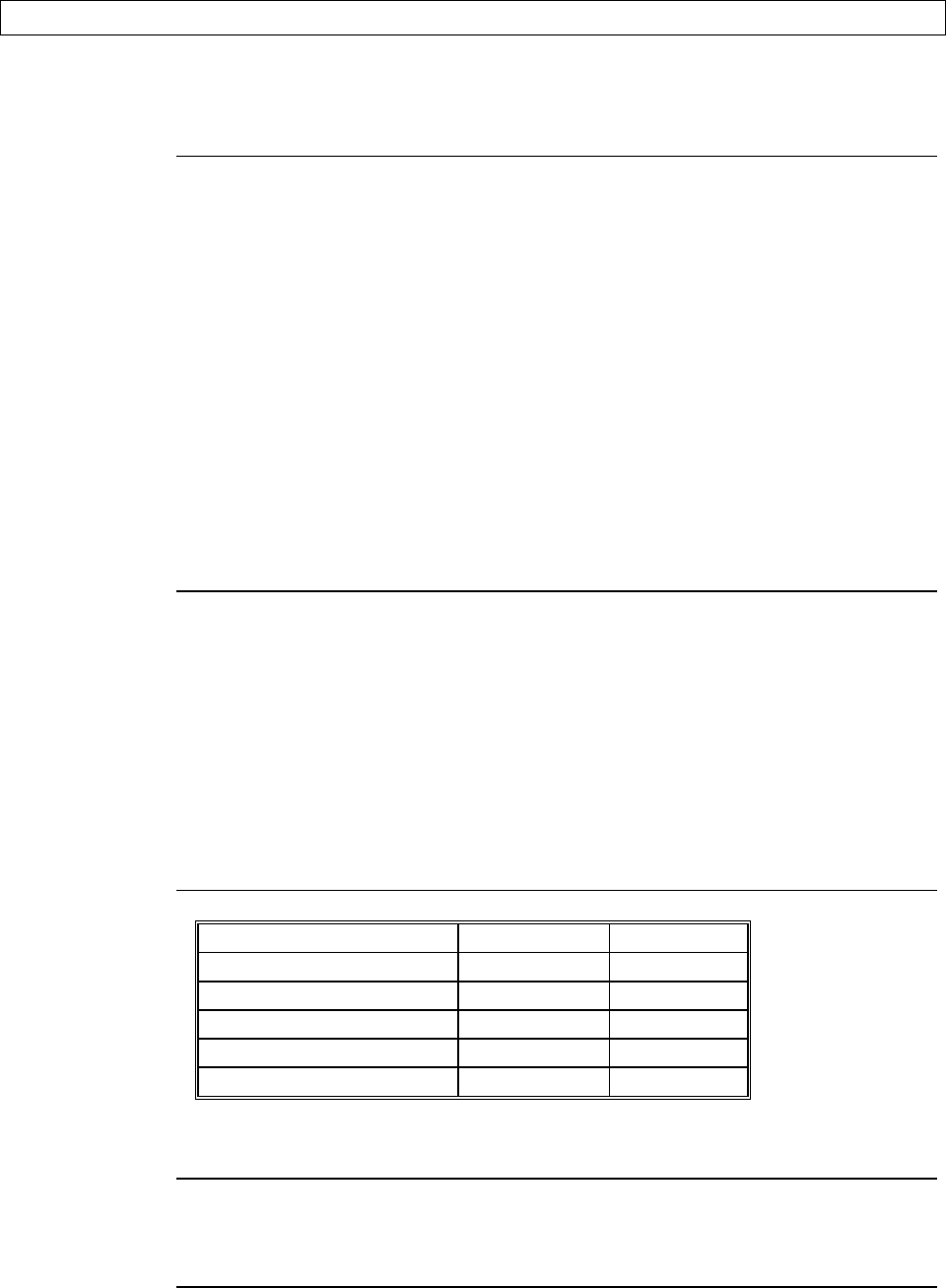

Schedule M-1 Reconciliation Total

Pension Plan Expense Per Books $6,246,075

Line 4 - Income Subject to Tax Not Recorded

on Books This Year

$(4,646,938)

Line 8 - Deductions on This Return Not

Charged Against Book Income This Year

$250,000

Pension Plan Expense Per Tax Return $1,849,137

Continued on next page

CHAPTER 10 SCHEDULE M-1 AUDIT TECHNIQUES

Page 10-23

Schedule M-1 Example, Continued

Explanation

Note that when applying Schedule M-1 principles to the pension plan expense

by itself, additions to taxable income on Schedule M-1 on Form 1120 would

decrease the pension expense while decreases to taxable income on Schedule

M-1 on Form 1120 would increase the pension plan expense.

Line 4

Line 4 - Section 420 Transfer - Cash Balance Plan is a combination of entries:

Description Amount

12-27-01 Cash $51,361,105

12-28-01 EPTA Inc. Common Stock $11,974,950

12-29-01 Misc. Assets $73,556

12-31-01 Cash $19,112,327

Subtotal $82,521,938

Gain Recorded On Books (AJE #24) $78,000,000

Subtotal $4,521,938

Dividend Received on Door Corporation

Terminated in 1994

$125,000

Section 420 Transfer - Cash Balance Plan $4,646,938

CHAPTER 10 SCHEDULE M-1 AUDIT TECHNIQUES

Page 10-24

Schedule M-1 Reconciliation

EPTA Inc.

Schedule M-1 Reconciliation

For the Year Ended December 31, 2001

Form 1120 US Corporation Income Tax Return Statement 1

Schedule M-1, Line 4 - Other Taxable Income

Deferred Intercompany Gain $5,498,124

Gain on Sale of Asset 84,701,429

Section 420 Transfer - Cash Balance Plan 4,646,938

Total $94,846,491

Schedule M-1, Line 5 - Other Book Expense

Non Deductible Contributions $22,500

Non Deductible Penalties 10,634

Miscellaneous Expense 14,398

Related Party Bonus 450,765

Specific Item Accrual 10,489

Total $508,786

Schedule M-1, Line 7 - Other Book Income

Unearned Revenue $390,476

Schedule M-1, Line 8 - Other Tax Expense

Tax Amortization $89,629

Deferred Compensation 59,490

Deferred Directors Fees 90,876

Deferred Executive Plan 976,493

Tax Loss from Asset Disposal 115,934

Bad Debt Reserve 4,907,289

State Taxes 50,923

Accrued Vacation 59,934

Accrued Bonus for Officers 250,693

Stock Options 1,409,395

Loss Reserve 1,972,234

Accrued Expense 465,585

Additional Pension Expense 250,000

Total $10,698,475