Page 1 - SFFAS 4 FASAB Handbook, Version 23 (9/24)

Statement of Federal Financial Accounting Standards 4:

Managerial Cost Accounting Standards and Concepts

Status

Summary

The managerial cost accounting concepts and standards contained in this statement are aimed

at providing reliable and timely information on the full cost of federal programs, their activities,

and outputs. The concepts of managerial cost accounting contained in this statement describe

the relationship among cost accounting, financial reporting, and budgeting. The five standards

set forth the fundamental elements of managerial cost accounting.

Managerial Cost Accounting Concepts

Managerial cost accounting should be a fundamental part of the financial management system

and, to the extent practicable, should be integrated with other parts of the system. Managerial

costing should use a basis of accounting, recognition, and measurement appropriate for the

intended purpose. Cost information developed for different purposes should be drawn from a

common data source, and output reports should be reconcilable to each other.

Managerial Cost Accounting Standards

Requirement for cost accounting - Each reporting entity should accumulate and report the costs

of its activities on a regular basis for management information purposes. Costs may be

Issued July 31, 1995

Effective Date For fiscal years beginning after September 30, 1996. Subsequently

modified to be for years beginning after September 30, 1997.

Affects None.

Affected by • SFFAS 9, Deferral of Implementation Date of SFFAS No. 4.

• SFFAS 30, Inter-Entity Cost Implementation, rescinds par. 110 and

amends par. 111 of SFFAS 4.

• SFFAS 55, Amending Inter-Entity Cost Provisions, rescinds SFFAS

30 which restored par. 110 and 111. SFFAS 55 then amends par. 110

and 111 and also added new disclosures in par. 113A.

Related Guidance • Interpretation 2, Accounting for Treasury Judgment Fund

Transactions TR 1, Audit Legal Letter Guidance

• Interpretation 6, Accounting for Imputed Intra-departmental Costs:

An Interpretation of SFFAS No. 4.

SFFAS 4

Page 2 - SFFAS 4 FASAB Handbook, Version 23 (9/24)

accumulated either through the use of cost accounting systems or through the use of cost finding

techniques.

Responsibility segments - Management of each reporting entity should define and establish

responsibility segments. Managerial cost accounting should be performed to measure and report

the costs of each segment’s outputs. Special cost studies, if necessary, should be performed to

determine the costs of outputs.

Full cost - Reporting entities should report the full costs of outputs in general purpose financial

reports. The full cost of an output produced by a responsibility segment is the sum of (1) the

costs of resources consumed by the segment that directly or indirectly contribute to the output,

and (2) the costs of identifiable supporting services provided by other responsibility segments

within the reporting entity, and by other reporting entities.

Inter-entity costs - Each entity’s full cost should incorporate the full cost of goods and services

that it receives from other entities. The entity providing the goods or services has the

responsibility to provide the receiving entity with information on the full cost of such goods or

services either through billing or other advice.

Recognition of inter-entity costs that are not fully reimbursed is limited to material items that (1)

are significant to the receiving entity, (2) form an integral or necessary part of the receiving

entity’s output, and (3) can be identified or matched to the receiving entity with reasonable

precision. Broad and general support services provided by an entity to all or most other entities

generally should not be recognized unless such services form a vital and integral part of the

operations or output of the receiving entity.

Costing methodology - Costs of resources consumed by responsibility segments should be

accumulated by type of resource. Outputs produced by responsibility segments should be

accumulated and, if practicable, measured in units. The full costs of resources that directly or

indirectly contribute to the production of outputs should be assigned to outputs through costing

methodologies or cost finding techniques that are most appropriate to the segment’s operating

environment and should be followed consistently.

The cost assignments should be performed using the following methods listed in the order of

preference: (a) directly tracing costs wherever feasible and economically practicable, (b)

assigning costs on a cause-and-effect basis, or (c) allocating costs on a reasonable and

consistent basis.

SFFAS 4

Page 3 - SFFAS 4 FASAB Handbook, Version 23 (9/24)

Table of Contents

Page

Summary 1

Executive Summary 4

Introduction 7

Managerial Cost Accounting Concepts 13

Managerial Cost Accounting Standards 20

Appendix A: Basis For Conclusions 47

Appendix B: Glossary [See Consolidated Glossary in Appendix E] 71

SFFAS 4

Page 4 - SFFAS 4 FASAB Handbook, Version 23 (9/24)

Executive Summary

1. The managerial cost accounting concepts and standards contained in this statement are

aimed at providing reliable and timely information on the full cost of federal programs, their

activities, and outputs. The cost information can be used by the Congress and federal

executives in making decisions about allocating federal resources, authorizing and

modifying programs, and evaluating program performance. The cost information can also

be used by program managers in making managerial decisions to improve operating

economy and efficiency.

2. The concepts of managerial cost accounting contained in this statement describe the

relationship among cost accounting, financial reporting, and budgeting. The five standards

set forth the fundamental elements of managerial cost accounting: (1) accumulating and

reporting costs of activities on a regular basis for management information purposes, (2)

establishing responsibility segments to match costs with outputs, (3) determining full costs

of government goods and services, (4) recognizing the costs of goods and services

provided among federal entities, and (5) using appropriate costing methodologies to

accumulate and assign costs to outputs.

3. These standards are based on sound cost accounting concepts and are broad enough to

allow maximum flexibility for agency managers to develop costing methods that are best

suited to their operational environment. Also, the managerial cost accounting standards and

practices will evolve and improve as agencies gain experience in using them. The following

is a summary of the concepts and standards contained in this statement.

Managerial Cost Accounting Concepts

4. Managerial cost accounting should be a fundamental part of the financial management

system and, to the extent practicable, should be integrated with other parts of the system.

Managerial costing should use a basis of accounting, recognition, and measurement

appropriate for the intended purpose. Cost information developed for different purposes

should be drawn from a common data source, and output reports should be reconcilable to

each other.

SFFAS 4

Page 5 - SFFAS 4 FASAB Handbook, Version 23 (9/24)

Managerial Cost Accounting Standards

Requirement for cost accounting

5. Each reporting entity should accumulate and report the costs of its activities on a regular

basis for management information purposes. Costs may be accumulated either through the

use of cost accounting systems or through the use of cost finding techniques.

Responsibility segments

6. Management of each reporting entity should define and establish responsibility segments.

Managerial cost accounting should be performed to measure and report the costs of each

segment’s outputs. Special cost studies, if necessary, should be performed to determine the

costs of outputs.

Full cost

7. Reporting entities should report the full costs of outputs in general purpose financial reports.

The full cost of an output produced by a responsibility segment is the sum of (1) the costs of

resources consumed by the segment that directly or indirectly contribute to the output, and

(2) the costs of identifiable supporting services provided by other responsibility segments

within the reporting entity, and by other reporting entities.

Inter-entity costs

8. Each entity’s full cost should incorporate the full cost of goods and services that it receives

from other entities. The entity providing the goods or services has the responsibility to

provide the receiving entity with information on the full cost of such goods or services either

through billing or other advice.

9. Recognition of inter-entity costs that are not fully reimbursed is limited to material items that

(1) are significant to the receiving entity, (2) form an integral or necessary part of the

receiving entity’s output, and (3) can be identified or matched to the receiving entity with

reasonable precision. Broad and general support services provided by an entity to all or

most other entities generally should not be recognized unless such services form a vital and

integral part of the operations or output of the receiving entity.

SFFAS 4

Page 6 - SFFAS 4 FASAB Handbook, Version 23 (9/24)

Costing methodology

10. Costs of resources consumed by responsibility segments should be accumulated by type of

resource. Outputs produced by responsibility segments should be accumulated and, if

practicable, measured in units. The full costs of resources that directly or indirectly

contribute to the production of outputs should be assigned to outputs through costing

methodologies or cost finding techniques that are most appropriate to the segment’s

operating environment and should be followed consistently.

11. The cost assignments should be performed using the following methods listed in the order

of preference: (a) directly tracing costs wherever feasible and economically practicable. (b)

assigning costs on a cause-and-effect basis, or (c) allocating costs on a reasonable and

consistent basis.

12. These accounting standards need not be applied to items that are qualitatively and

quantitatively immaterial. The Board recommends that the managerial accounting standards

of this Statement become effective for fiscal periods beginning after September 30, 1996.

Earlier implementation is encouraged.

SFFAS 4

Page 7 - SFFAS 4 FASAB Handbook, Version 23 (9/24)

Introduction

Background

13. Reliable information on the costs of federal programs and activities is crucial for effective

management of government operations. In Statement of Federal Financial Accounting

Concepts (SFFAC) No. 1, Objectives of Federal Financial Reporting, issued in 1993, it is

stated that the objectives of federal financial reporting are to provide useful information to

assist internal and external users in assessing the budget integrity, operating performance,

stewardship, and systems and control of the federal government.

1

14. Managerial cost accounting is especially important for fulfilling the objective of assessing

operating performance. In relation to that objective, it is stated in SFFAC No. 1 that federal

financial reporting should provide information that helps users to determine:

• Costs of specific programs and activities and the composition of, and changes in, those

costs;

• Efforts and accomplishments associated with federal programs and their changes over

time and in relation to costs; and

• Efficiency and effectiveness of the government’s management of its assets and

liabilities.

2

15. It is further stated in SFFAC No. 1 that “The topics of costs and performance measurement

are related because it is by associating cost with activities or cost objectives that accounting

can make much of its contribution to reporting on performance.”

3

“Cost” is the monetary

value of resources used or sacrificed or liabilities incurred to achieve an objective, such as

to acquire or produce a good or to perform an activity or service. Costs incurred may benefit

current and future periods. In financial accounting and reporting, the costs that apply to an

entity’s operations for the current accounting period are recognized as expenses of that

period.

1

Statement of Federal Financial Accounting Concepts No. 1, Objectives of Federal Financial Reporting (September 2,

1993), pars. 110 and 111.

2

Ibid., pars. 126-130.

3

Ibid., par. 192.

SFFAS 4

Page 8 - SFFAS 4 FASAB Handbook, Version 23 (9/24)

16. The Chief Financial Officers Act of 1990 includes among the functions of chief financial

officers “the development and reporting of cost information” and “the systematic

measurement of performance.”

4

In July 1993, Congress passed the Government

Performance and Results Act (GPRA) which mandates performance measurement by

federal agencies.

5

In September 1993, in his report to the President on the National

Performance Review (NPR), Vice President Al Gore recommended an action which

required the Federal Accounting Standards Advisory Board to issue a set of cost accounting

standards for all federal activities.

6

Those standards will provide a method for identifying the

unit cost of all government activities.

17. In early 1994, the Federal Accounting Standards Advisory Board (the Board) convened an

advisory group to help develop standards for managerial cost accounting in the federal

government. The group included members from government, business, and academe. Their

views and proposals have been considered by the Board, and their work contributed greatly

in developing this document.

Users Of Federal Cost Information

18. The cost of government is a concern to the public as well as to the federal government itself.

Most government service efforts and accomplishments cannot be measured in financial

terms alone. Unlike private business, there is no “bottom line” or profit index to help

measure public sector performance. However, government service efforts and

accomplishments can be evaluated using both financial and non-financial measures, and

“cost” is an important financial measure for government programs. Internal and external

federal information users identified below will find these standards helpful in assessing

operating performance, stewardship, systems, and control of the federal government.

19. Government managers are the primary users of cost information. They are responsible for

carrying out program objectives with resources entrusted to them. Reliable and timely cost

information helps them ensure that resources are spent to achieve expected results and

outputs, and alerts them to waste and inefficiency.

20. Congress and federal executives, including the President, make policy decisions on

program priorities and allocate resources among programs. These officials need cost

4

104 Stat. 2938 (See particularly 31 U.S.C. sec 902).

5

107 Stat. 285 (See particularly, 31 U.S.C. sections 1101, 1105, 1115, 1116-1119, 9703, 9704).

6

Vice President Al Gore, Creating A Government That Works Better & Costs Less, Accompanying Report of the

National Performance Review (September 1993), p. 59.

SFFAS 4

Page 9 - SFFAS 4 FASAB Handbook, Version 23 (9/24)

information to compare alternative courses of action and to make program authorization

decisions by assessing costs and benefits. They also need cost information to evaluate

program performance.

21. Citizens, including news media and interest groups, are concerned with the costs and

results of federal programs that affect their interests. They need program cost information to

judge whether resources are allocated to programs rationally and if the programs operate

efficiently and effectively.

Objectives

22. The managerial cost accounting concepts and standards presented here are intended for all

the user groups identified above. These standards are aimed at achieving three general

objectives:

• Provide program managers

7

with relevant and reliable information relating costs to

outputs and activities. Based on this information, program managers can respond to

inquiries about the costs of the activities they manage. The cost information will assist

them in improving operational economy and efficiency;

• Provide relevant and reliable cost information to assist the Congress and executives in

making decisions about allocating federal resources, authorizing and modifying

programs, and evaluating program performance; and

• Ensure consistency between costs reported in general purpose financial reports and

costs reported to program managers. This includes standardizing terminology for

managerial cost accounting to improve communication among federal organizations

and users of cost information.

Scope Of Standards

23. This statement contains managerial cost concepts and five standards for the federal

government. The five standards address the following topics:

(1) Requirement for cost accounting,

(2) Responsibility segments,

(3) Full cost,

7

Statement of Federal Financial Accounting Concepts No. 1, Objectives of Financial Reporting, defined “Program

managers” as individuals who manage federal programs, and stated that “Their concerns include operating plans,

program operations, and budget execution.” SFFAC No. 1, par. 85.

SFFAS 4

Page 10 - SFFAS 4 FASAB Handbook, Version 23 (9/24)

(4) Inter-entity costs, and

(5) Costing methodology.

The essence of each standard is briefly stated in a box followed by detailed explanations.

However, both the words in the boxes and the entire text of explanations constitute

the requirements of the standards.

24. These standards are based on sound cost accounting concepts and allow sufficient

flexibility for agencies to develop managerial cost accounting practices that are suited to

their specific operating environments. Also, it is expected that cost accounting standards

and practices will evolve and improve as agencies gain experience in using them.

25. Other Statements of Federal Financial Accounting Standards (SFFAS) address recognition

and measurement of assets and liabilities. For additional guidance, readers should consult:

SFFAS No. 1, Accounting for Selected Assets and Liabilities; SFFAS No. 2, Accounting for

Direct Loans and Loan Guarantees; and SFFAS No. 3, Accounting for Inventory and

Related Property. The Board is working on and will soon complete other recognition and

measurement projects related to revenues, liabilities, property, plant, and equipment, and

other elements of financial statements.

8

Terminology

26. Managerial cost accounting information, to be useful, must rely on consistent and uniform

terminology for concepts, practices, and techniques. Consistent and uniform use of

terminology can help avoid confusion and mis-communication among organizations and

individuals.

27. As a start toward developing consistent managerial cost accounting terminology within the

federal government, this statement includes a glossary of basic cost accounting terms.

Materiality

28. Except as otherwise noted, the accounting and reporting provisions of these accounting

standards need not be applied to items that are qualitatively or quantitatively immaterial.

8

See FASAB Exposure Drafts, Accounting for Liabilities of the Federal Government (November 7, 1994); Accounting

for Property, Plant, and Equipment (February 28, 1995); and Revenue and Other Financing Sources (Pending).

SFFAS 4

Page 11 - SFFAS 4 FASAB Handbook, Version 23 (9/24)

29. The determination of whether an item is material depends on the degree to which omitting

information about the item makes it probable that the judgment of a reasonable person

relying on the information would have been changed or influenced by the omission.

Effective Date

30. The managerial cost accounting standards prescribed in SFFAS No. 4 shall be effective for

fiscal periods beginning after September 30, 1997. Earlier implementation is encouraged.

Purposes Of Using Cost Information

31. There are many different purposes for which cost information may be used by the federal

government. The focus of this statement is on cost information needed to improve federal

financial management and managerial decision making.

32. In managing federal government programs, cost information is essential in the following five

areas: (1) budgeting and cost control, (2) performance measurement, (3) determining

reimbursements and setting fees and prices, (4) program evaluations, and (5) making

economic choice decisions. Each of these uses is discussed below.

Budgeting And Cost Control

33. Information on the costs of program activities can be used as a basis to estimate future

costs in preparing and reviewing budgets. Once budgets are approved and executed, cost

information serves as a feedback to budgets. Using cost information, federal managers can

control and reduce costs, and find and avoid waste. For example, with appropriate cost

information, federal managers can:

• Compare costs with known or assumed benefits of activities, identify value-added and

non-value-added activities, and make decisions to reduce resources devoted to

activities that are not cost-effective;

• Compare and determine reasons for variances between actual and budgeted costs of

an activity or a product;

• Compare cost changes over time and identify their causes;

• Identify and reduce excess capacity costs; and

• Compare costs of similar activities and find causes for cost differences, if any.

SFFAS 4

Page 12 - SFFAS 4 FASAB Handbook, Version 23 (9/24)

Performance Measurement

34. Measuring performance is a means of improving program efficiency, effectiveness, and

program results. One of the stated purposes of the GPRA of 1993 is to “. . .improve the

confidence of the American people in the capability of the federal government, by

systematically holding federal agencies accountable for achieving program results.”

35. Measuring costs is an integral part of measuring performance in terms of efficiency and

cost-effectiveness. Efficiency is measured by relating outputs to inputs. It is often expressed

by the cost per unit of output. While effectiveness in itself is measured by the outcome or the

degree to which a predetermined objective is met, it is commonly combined with cost

information to show “cost-effectiveness.” Thus, the service efforts and accomplishments of a

government entity can be evaluated with the following measures:

(1) Measures of service efforts which include the costs of resources used to provide the

services and non-financial measures;

(2) Measures of accomplishments which are outputs (the quantity of services provided)

and outcomes (the results of those services); and

(3) Measures that relate efforts to accomplishments, Such as cost per unit of output or

cost-effectiveness.

36. Thus, as stated previously, performance measurement requires both financial and non-

financial measures. Cost is a necessary element for performance measurement, but is not

the only element.

Determining Reimbursements And Setting Fees And Prices

37. Cost information is an important basis in setting fees and reimbursements. Pricing and

costing, however, are two different concepts. Setting prices is a policy matter, sometimes

governed by statutory provisions and regulations, and other times by managerial or public

policies. Thus, the price of a good or service does not necessarily equal the cost of the good

or the service determined under a particular set of principles. Nevertheless, cost is an

important consideration in setting government prices. With certain exceptions, OMB

requires:

9

9

OMB Circular A-25, User Charges (Revised July 8, 1993).

SFFAS 4

Page 13 - SFFAS 4 FASAB Handbook, Version 23 (9/24)

• With respect to goods and services that the government provides in its sovereign

capacity to a particular group of individuals as a special benefit, user charges should

be sufficient to recover the full cost of those goods and services; and

• With respect to goods and services that the government provides under business-like

conditions, user charges for those goods and services need not be limited to the

recovery of full cost and may yield a net revenue.

38. Also, cost information is important in calculating reimbursements for products and services

provided by one government agency to another. Even if fees or reimbursements do not

recover the full costs due to policy or economic constraints, management needs to be aware

of the difference between cost and price. With this information, program managers can

properly inform the public, the Congress, and federal executives about the costs of

providing the goods or services.

Program Evaluations

39. Costs of federal resources required by programs are an important factor in making policy

decisions related to program authorization, modification, and discontinuation. These

decisions are usually subject to policy constraints, and often require the consideration of

social and economic costs and benefits affecting different sectors of the economy and

society. Nevertheless, the costs of federal resources required are an important factor.

Information on program costs can be used as a basis for cost-benefit considerations.

Economic Choice Decisions

40. Often, agencies and programs face decisions involving choices among alternative actions,

such as whether to do a project in-house or contract it out; to accept or reject a proposal; or

to continue or drop a product or service. Making these decisions requires cost comparisons

among available alternatives.

Managerial Cost Accounting Concepts

Managerial cost accounting should be a fundamental part of the financial management system and, to the

extent practicable, should be integrated with other parts of the system. Managerial costing should use a

basis of accounting, recognition, and measurement appropriate for the intended purpose. Cost

information developed for different purposes should be drawn from a common data source, and output

reports should be reconcilable to each other.

SFFAS 4

Page 14 - SFFAS 4 FASAB Handbook, Version 23 (9/24)

41. Managerial cost accounting should be an essential element of proper financial planning,

control, and evaluation for any organization or activity that uses resources having monetary

value. Managerial cost accounting is a basic part of the financial management system in

that it supports and provides data to the budgetary and financial accounting functions and,

by itself, provides useful information for both internal and external users.

Role Of Managerial Cost Accounting In Financial Management

42. Managerial cost accounting is the process of accumulating, measuring, analyzing,

interpreting, and reporting cost information useful to both internal and external groups

concerned with the way in which the organization uses, accounts for, safeguards, and

controls its resources to meet its objectives. Managerial cost accounting, therefore, is the

servant of both budgetary and financial accounting and reporting because it assists those

systems in providing information. Also, it provides useful information directly to

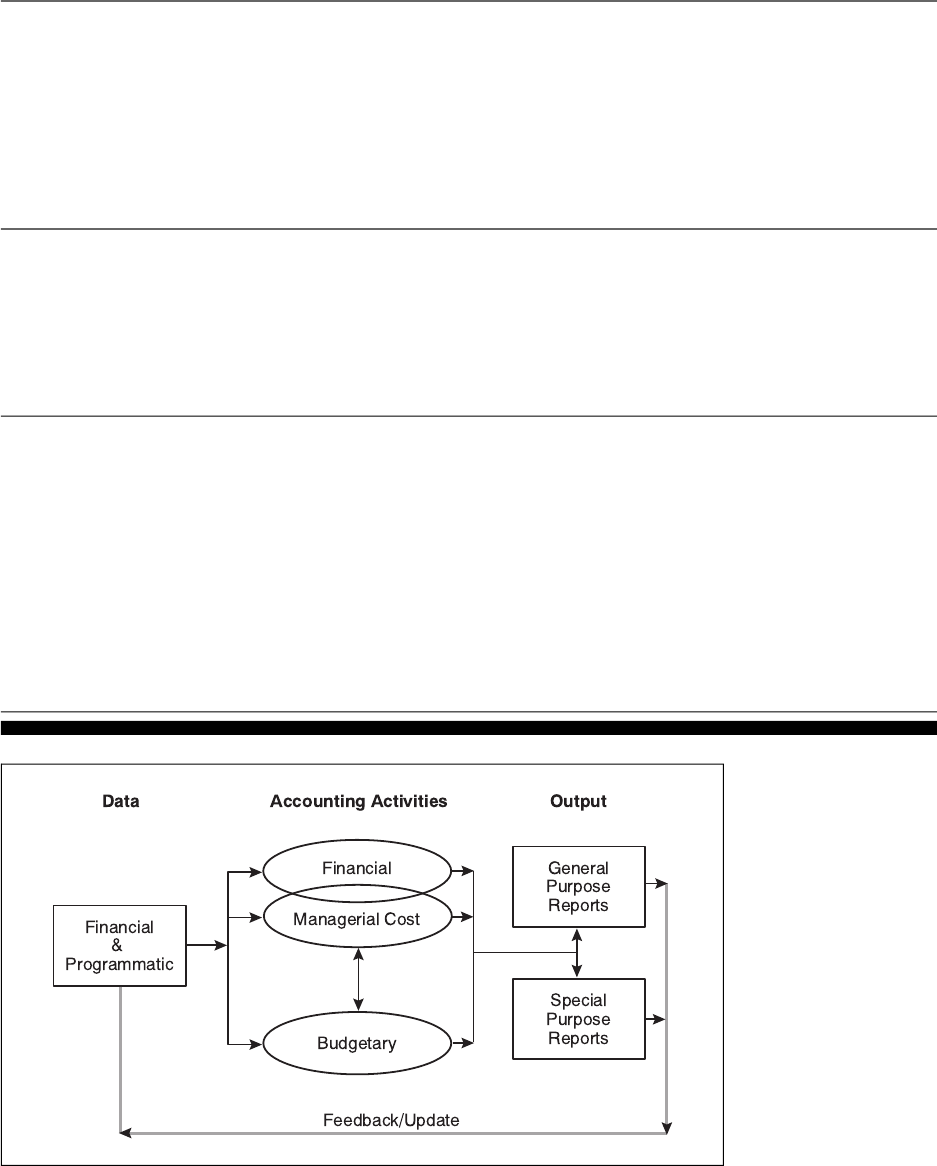

management. These relationships are shown in Figure 1.

Figure 1: Financial Management Information Framework

Common Data Source

43. The information flow within a financial management system begins with a basic information

pool or common data source. This data source consists of all financial and programmatic

information used by the budgetary, cost, and financial accounting processes. It includes all

SFFAS 4

Page 15 - SFFAS 4 FASAB Handbook, Version 23 (9/24)

financial and much non-financial data, such as environmental data, that are necessary for

budgeting and financial reporting.

10

The common data source also includes evaluation and

decision information developed as a result of prior reporting and feedback. Other types of

data may be included based upon perceived needs and purposes related to the ultimate

users of the information.

44. The common data source may include many different kinds of data. It is far more than the

information about financial transactions found in the standard general ledger, although that

is a significant part of the data source. Few organizations or entities maintain all these data

in any one system or location. Furthermore, the use of the term “data source” is not meant

to imply the use of computerized systems for source information. Instead, the term is used

in a broad way to include many sources of information.

45. Managerial cost accounting, financial accounting, and budgetary accounting draw

information as needed from the common data source. The data obtained by each of these is

processed to attain specific objectives by reporting useful information.

Relationship to Financial Accounting

46. As shown in Figure 1 by their overlap, managerial cost accounting and financial accounting

are closely related or integrated. To some degree, this is due to the historical development

of cost accounting as a method for more detailed scorekeeping with the requirement to

provide inventory values for external financial reporting purposes.

11

In part, it is because

cost information generally originates with transactions recorded for financial accounting

purposes.

47. While inventory valuation is still part of the fundamental relationship, managerial cost

accounting serves financial accounting in several other ways. Fundamentally, managerial

cost accounting should assist financial accounting in determining the results of operations

during a fiscal period by providing relevant data that are accumulated to produce operating

expenses. These data include the allocation of capitalized costs to periods of time or units of

usage.

48. Traditionally, managerial cost accounting information pertaining to financial accounting has

involved costs of past transactions and the assignment of transaction value to fiscal periods

10

The makeup of core data and environmental data is discussed in Statement of Federal Financial Accounting

Concepts No. 1, Objectives of Federal Financial Reporting, Chapter 7, and, therefore, a detailed discussion is not

provided here.

11

Coulthurst, Nigel and John Piper, “The State of Cost and Management Accounting,” Management Accounting, April

1986.

SFFAS 4

Page 16 - SFFAS 4 FASAB Handbook, Version 23 (9/24)

and outputs. These purposes and uses are closely aligned with the financial accounting

activity and traditional external financial reporting. This past cost aspect has been

acknowledged in Objectives of Federal Financial Reporting which states that “financial

accounting is largely concerned with assigning the value of past transactions to appropriate

time periods.”

12

Relationship to Budgetary Accounting

49. Managerial cost accounting should also provide budgetary accounting with cost information.

However, the two are not as closely aligned as is the case with financial accounting (see

Figure 1). Mostly, this is because costs are usually recorded, accumulated, and allocated by

managerial cost accounting on an accrual basis of accounting which is different from the

obligation or cash basis generally used in budgetary accounting.

50. Still, managerial cost accounting does provide cost information to budgetary accounting for

use in preparing yearly and long-term budgets for required materials, supplies, equipment,

human resources, and other resources needed to produce different levels of outputs.

Managerial cost accounting also helps in making many budgetary decisions such as those

concerning future capital expenditures and purchase/lease alternatives.

51. It is important to note that the Board’s authority does not extend to recommending

budgetary standards or budgetary concepts, and that is not the purpose of this statement.

13

However, the Board is committed to providing relevant and reliable cost accounting

information that supports budget planning, formulation, and execution.

Cost Information for Management Purposes

52. Managerial cost accounting produces information directly for management use, sometimes

employing data produced by the budgetary and financial accounting processes. Cost

information is used for many different purposes which can be generally classified into five

types: performance measurement; cost reduction and control; determination of

reimbursements and fee or price setting; program authorization, modification, and

discontinuation decisions; and decisions to contract out work or make other changes in the

methods of production.

53. To meet these needs, managerial cost accounting should use basic cost data and non-

financial or programmatic data. For example, it tracks units of output produced and input

12

Statement of Federal Financial Accounting Concepts No. 1, Objectives of Federal Financial Reporting, par. 168.

13

Memorandum of Understanding establishing the FASAB, October 10, 1990.

SFFAS 4

Page 17 - SFFAS 4 FASAB Handbook, Version 23 (9/24)

used including the amount of labor in terms of employees or employee-hours. Sometimes,

information from cost analysis is used to compare actual to predetermined or anticipated

costs. An organization may use cost estimates, cost studies, and cost finding techniques.

54. While managerial cost accounting is concerned not only with past costs and future costs,

one of its most important features is the use of present costs to assist management. This

current cost aspect of managerial cost accounting is referred to in the Objectives of Federal

Financial Reporting where is states that “accounting data may be further assigned,

allocated, or associated with units of activity or production, segments of organizations, etc.,

within the same time period. These kinds of intraperiod allocations are developed most

extensively in the branch of accounting called cost accounting. Neither the FASB nor the

GASB has devoted much attention to this branch of accounting, but the FASAB, because of

its unique mission, will need to do so.”

14

Managerial cost accounting information pertaining

to present costs is most often used for controlling and reducing those costs, controlling work

processes, and measuring current performance.

Reporting Relationships

55. Proper financial management requires that the three accounting processes work closely

together to provide useful reporting to both internal and external users. The internal-external

dual focus of federal reporting has been established in the Objectives of Federal Financial

Reporting. It states that “The FASAB and its sponsors believe that any description of federal

financial reporting objectives should consider the needs of both internal and external users

and the decisions they make.” In addition, it says that “the FASAB... considers the

information needs of both internal and external users. In part, this is because the distinction

between internal and external users is in many ways less significant for the federal

government than for other entities.” It goes on to classify the users of financial information

into four major groups: program managers, executives, the Congress, and citizens.

15

These

categories include both internal and external users.

56. Federal financial reporting encompasses general and special purpose reports to meet the

needs of the four user groups. Information produced by managerial cost accounting appears

in or influences both types of reports.

16

As discussed above, managerial cost accounting

should provide information for use by both financial accounting and budgetary accounting.

14

Statement of Federal Financial Accounting Concepts No. 1, Objectives of Federal Financial Reporting, par. 174.

15

Ibid., pars. 23, 25, and par. 75.

16

The types of general purpose and special purpose reports are discussed in Statement of Federal Financial

Accounting Concepts No. 1, Objectives of Federal Financial Reporting, Chapter 7.

SFFAS 4

Page 18 - SFFAS 4 FASAB Handbook, Version 23 (9/24)

That information is used by those processes in producing both general purpose and special

purpose reports.

57. Managerial cost accounting also results in reports of its own. Most often these are special

purpose reports designed for internal users, typically program and line managers. However,

they may be for groups generally considered external users.

58. One of the most important aspects of reporting in which managerial cost accounting plays a

large role is that of performance reporting. Measuring and reporting actual performance

against established goals is essential to assess governmental accountability. Cost

information is necessary in establishing strategic goals, measuring service efforts and

accomplishments, and relating efforts to accomplishments. The importance of cost

information in relation to performance measurement and performance reporting has been

recognized in the Objectives of Federal Financial Reporting, which said “One reason for

performing cost accounting is to assist in performance measurement” and it also stated that

“The topics of cost and performance measurement are related because it is by associating

cost with activities or ‘cost objectives’ that accounting can make much of its contribution to

reporting on performance.”

17

Basis Of Accounting And Recognition/measurement Methods

59. Costs may be measured, analyzed, and reported in many ways. A particular cost

measurement has meaning only when considering its purpose. The measurement of costs

can vary depending upon the circumstances and purpose for which the measurement is to

be used. In Objectives of Federal Financial Reporting, it is stated that “the Board’s own

focus is on developing generally accepted accounting standards for reporting on the

financial operations, financial position, and financial condition of the federal government and

its component entities and other useful financial information. This implies a variety of

measures of costs and other information that complements the information available in the

budget [emphasis added].”

18

60. In addition, it is stated that “In defining the proper measurement, assignment, and allocation

of cost for a given purpose, selecting the appropriate accounting method and whether to use

full costing should be carefully considered.”

19

Further, it added that “The accrual basis of

17

Ibid., par. 174 and par. 192.

18

Ibid., par. 191.

19

Ibid., par. 196.

SFFAS 4

Page 19 - SFFAS 4 FASAB Handbook, Version 23 (9/24)

accounting generally provides a better matching of costs to the production of goods and

services, but its use and application for any given purpose must be carefully evaluated.”

20

61. Therefore, managerial cost accounting should provide cost information using a basis of

accounting and recognition/measurement standards that are appropriate for the intended

use of the information. When managerial cost accounting is used to supply information for

use by financial accounting and financial reporting, that information should be consistent

with the basis of accounting and recognition/measurement standards required by federal

accounting principles. Traditionally this has meant the use of accrual accounting and

historical cost measurement, particularly in general purpose reports.

62. When managerial cost accounting is used to supply information for the preparation and

review of budgets, cost data should be consistent with the basis of accounting and

recognition/measurement used in financial reporting, but may be adjusted to meet the

budgetary information needs.

63. Special purpose cost studies and analyses are sometimes performed for decision making.

In those studies and analyses, management may need to develop cost data beyond those

currently reported in general purpose financial reports. For example, in making planning

decisions, management may develop replacement costs and capital costs. However, the

basis and methods used should be appropriate for the circumstances and consistent with

the intended purposes.

Reconciliation Of Information

64. Different bases of accounting will produce different costs for the same item, activity, or

entity. This can confuse users of cost information. Therefore, reports that use different

accounting bases or different recognition and measurement methods should be

reconcilable, and should fully explain those bases and methods. Regardless of the type of

report in which it is presented, cost information should ultimately be traceable back to the

original common data source.

65. To be reconcilable, the amount of the differences in the information reported should be

ascertainable and the reasons for the differences should be explainable. In some situations,

informational differences may be clearly understandable without further explanation.

However, other cases may require a narrative statement concerning the differences. In

complicated situations, a schedule or table may be required to fully explain the differences.

20

Ibid., par. 197.

SFFAS 4

Page 20 - SFFAS 4 FASAB Handbook, Version 23 (9/24)

66. Financial reporting has long recognized the necessity for reconciliation between information

reported on different accounting bases. Reconciliations have been required in federal

financial reports to show and explain significant differences between budget reports and

financial statements prepared in accordance with generally accepted accounting principles.

Managerial Cost Accounting Standards

Requirement For Cost Accounting

67. Cost information is essential to effective financial management and should play an

important role in federal financial reporting. Managerial cost accounting processes are the

means of providing cost information in an efficient and reliable manner on a continuing

basis.

Need For Consistent Cost Accounting On A Regular Basis

68. To perform managerial cost accounting on a “regular basis” means that entities should

establish procedures to accumulate and report costs continuously, routinely, and

consistently for management information purposes. Consistent and regular cost accounting

is needed to meet the second objective of federal financial reporting which states

information should be provided to help the user determine the costs of providing specific

programs and activities and the composition of, and changes in those costs. That objective

also requires the reporting of performance information of federal programs and the changes

over time in that performance in relation to the costs.

69. The requirement for managerial cost accounting on a regular and consistent basis supports

recent legislative actions. The CFO Act of 1990 states that agency CFOs shall provide for

the development and reporting of cost information and the periodic measurement of

performance. In addition, the GPRA of 1993 requires each agency, for each program, to

establish performance indicators and measure or assess relevant outputs, service levels,

and outcomes of each program as a basis for comparing actual results with established

Each reporting entity

21

should accumulate and report the cost of its activities on a regular basis for

management information purposes. Costs may be accumulated either through the use of cost accounting

systems or through the use of cost finding techniques.

21

The term “reporting entity” as used in this document conveys the same meaning as defined in FASAB Statement of

Recommended Accounting Concepts No. 2, Entity and Display (May 1995).

SFFAS 4

Page 21 - SFFAS 4 FASAB Handbook, Version 23 (9/24)

goals. The nature of these legislative mandates requires reporting entities to develop and

report cost information on a consistent and regular basis.

70. The managerial cost accounting processes consist of collecting data from the common data

source, processing that data, and reporting cost and output information in general purpose

and special purpose reports. Appropriate procedures and practices should also be

established to enable the collection, measurement, accumulation, analysis, interpretation,

and communication of cost information. This can be accomplished through the use of a cost

accounting system or the use of cost finding techniques and other cost studies and

analyses. A cost accounting “system” is an organized grouping of methods and activities

designed to consistently produce reliable cost information.

Basic Cost Accounting Processes

71. Regardless of whether a reporting entity uses a cost accounting system or cost finding

techniques, the methods and procedures followed should be designed to perform at least a

certain minimum level of cost accounting and provide a basic amount of cost information

necessary to accomplish the many objectives associated with planning, decision making,

control, and reporting. The more important of these minimum criteria for cost accounting are

associated with the standards in the remainder of this statement. Others are also important.

• Responsibility Segments - Cost information should be collected by responsibility

segments which have been identified by management and outputs should be defined

for each responsibility segment.

22

• Full Costing - Each reporting entity should measure the full cost of outputs so that total

operational costs and total unit costs of outputs can be determined. “Full cost” includes

the cost of goods or services provided by other entities when the applicable criteria are

met.

23

• Costing Methodology - The costing methodology used (e.g., activity-based costing, job

order costing, standard costing, etc.) should be appropriate for management’s needs

and the operating environment.

24

• Performance Measurement - Cost accounting should provide information needed to

determine and report service efforts and accomplishments and information necessary

to meet the requirements of the GPRA or interface with a system that provides such

22

See standard in this statement concerning responsibility segments.

23

See standard concerning full costs and standard concerning inter-entity costing.

24

See standard concerning costing methodology.

SFFAS 4

Page 22 - SFFAS 4 FASAB Handbook, Version 23 (9/24)

information. This includes the quantity of inputs and outputs and other non-financial

information needed in the measurement of performance.

• Reporting Frequency - Cost information should be reported in a timely manner and on

a regular basis consistent with the needs of management and the requirements of both

budgetary and financial reporting.

• Standard General Ledger - Managerial cost accounting should be integrated with

general financial accounting. Both depend on the standard general ledger for basic

financial transaction data.

• Precision of Information - Cost information supplied to internal and external users

should be reliable and useful in making evaluations or decisions. At the same time,

unnecessary precision and refinement of data should be avoided.

• Special Situations - The managerial cost accounting processes should be designed to

accommodate any of management’s special cost information needs that may arise due

to unusual or special situations or circumstances. If such cost information is needed on

a regular basis, appropriate procedures to provide it should be developed.

• Documentation - All managerial cost accounting activities, processes, and procedures

should be documented by a manual, handbook, or guidebook of applicable accounting

operations. This reference should outline the applicable activities, provide instructions

for procedures and practices to be followed, list the cost accounts and subsidiary

accounts related to the standard general ledger, and contain examples of forms and

other documents used.

Complexity Of Cost Accounting Processes

72. While each entity’s managerial cost accounting should meet the basics discussed above,

this standard does not specify the degree of complexity or sophistication of any managerial

cost accounting process. Each reporting entity should determine the appropriate detail for

its cost accounting processes and procedures based on several factors. These include the:

• nature of the entity’s operations;

• precision desired and needed in cost information;

• practicality of data collection and processing;

• availability of electronic data handling facilities;

• cost of installing, operating, and maintaining the cost accounting processes; and

• any specific information needs of management.

73. Some entities may find that they can purchase basic “off-the-shelf” cost accounting

programs, systems, or processes, or adapt those of other federal agencies. All entities

should consider using similar or compatible cost accounting processes throughout their

component units to facilitate comparison and consolidation of cost information.

SFFAS 4

Page 23 - SFFAS 4 FASAB Handbook, Version 23 (9/24)

Cost Findings, Studies, And Analyses

74. A cost accounting system is a continuous and systematic cost accounting process which

may be designed to accumulate and assign costs to a variety of objects routinely or as

desired by the management. Such a system may be best for some reporting entities.

75. Some entities may not need a sophisticated system to perform detailed cost accumulation

and assignment. They need to accumulate and report costs regularly as required by this

standard, but they may determine and analyze costs through special cost studies and

analyses. Also, some entities may use a combination of a system supplemented by cost

studies.

76. Cost information may be developed and savings achieved in some cases by the use of

special cost studies or cost analyses to develop information helpful in certain decision

making situations. In addition, cost finding techniques may be used to determine the cost of

products or services. Cost finding is a method for determining the cost of producing goods

or services using appropriate procedures. Cost finding techniques may also be useful for

computing costs in cases where the information is not needed on a recurring basis.

Responsibility Segments

77. The standard states that the management of each reporting entity should define and

establish responsibility segments. This section explains the concept of responsibility

segment, purposes of segmentation, and how responsibility segments can be structured.

Defining Responsibility Segments

78. A responsibility segment is a component of a reporting entity

25

that is responsible for

carrying out a mission, conducting a major line of activity, or producing one or a group of

related products or services. In addition, responsibility segments usually possess the

following characteristics:

(1) Their managers report to the entity’s top management directly;

Management of each reporting entity should define and establish responsibility segments. Managerial cost

accounting should be performed to measure and report the costs of each segment’s outputs. Special cost

studies, if necessary, should also be performed to determine the costs of outputs.

25

The term “reporting entity” referred to in this document conveys the same meaning as defined in FASAB Statement of

Recommended Accounting Concepts No. 2, Entity and Display (May 1995).

SFFAS 4

Page 24 - SFFAS 4 FASAB Handbook, Version 23 (9/24)

(2) Their resources and results of operations can be clearly distinguished from those of

other segments of the entity.

26

79. A responsibility segment is a unit for which managerial cost accounting is performed.

Entities may use a centralized accounting system or segment-based systems to provide

cost information for each segment. For each segment, managerial cost accounting should:

(1) Define and accumulate outputs, and if feasible, quantify each type of output in units;

(2) Accumulate costs and quantitative units of resources consumed in producing the

outputs; and

(3) Assign costs to outputs, and calculate the cost per unit of each type of output.

80. Some reporting entities may have only one responsibility segment, if they perform one

single mission or one type of service. Other reporting entities may have several

responsibility segments. Also, a sub-organization of the federal government may be a

reporting entity in itself and, at the same time, it may also be a responsibility segment of a

higher level reporting entity to which it belongs. The Forest Service, for example, may be a

reporting entity because it may meet the reporting entity criteria. As such, it may establish

responsibility segments for itself. At the same time, the Forest Service may be regarded as

a responsibility segment of the Department of Agriculture, of which it is a component.

81. However, for a given reporting entity, its management should establish one or more

responsibility segments to perform managerial cost accounting functions.

Purposes Of Segmentation

82. A basic purpose of dividing an entity into segments is to determine and report the costs of

services and products that each segment produces and delivers. Many federal departments

and agencies manage programs that produce a variety of goods and services. Accounting

for entity-wide revenues and expenses in aggregate would serve financial reporting for the

entity, but would not serve costing purposes. In order to determine the cost of each type of

service or product, it is necessary to divide an entity into segments such that each segment

is responsible for certain types of services or products. Each segment can then be used as

a vehicle for accumulating costs incurred by the segment to match with its outputs. Each

segment can use a cost methodology that is best suited to its operations.

26

These two characteristics make responsibility segments, as the term is used in this document, differ from cost

centers. A cost center can be at any level of an organization and may not report to the top management directly. As will

be explained later, a responsibility segment can contain cost centers in itself.

SFFAS 4

Page 25 - SFFAS 4 FASAB Handbook, Version 23 (9/24)

83. Another important purpose of segmentation is to facilitate cost control and management.

Cost information provided for each segment helps managers to examine costs of specific

resources consumed and activities performed in each segment. Managers can analyze cost

variances in both dollars and the units of resources consumed against budgets or

standards. Since each segment performs a particular pattern of processes and activities to

produce its output, managers can analyze those processes and activities to compare their

costs with the value they contribute to the output.

84. For entities that consist of components engaging in diverse lines of activities, it is desirable

to provide financial reports that display information for significant components individually

and of the entity in its entirety.

27

Some entities may find costs accumulated by segments

useful in support of financial reporting by components.

85. For internal management, segmentation could also facilitate performance measurement.

Since each segment is responsible for a mission, or a line of activity to produce a certain

type of output, performance goals can be set for each segment based on its specific tasks

and operating patterns. Information on costs, outputs, and outcomes related to each

segment can be used to measure its performance against the goals. The results of the

segment performance measurement could also support external reporting on performance

measures for the entire reporting entity or its major programs.

Structuring Responsibility Segments

86. Reporting entity management should define and structure its responsibility segments. The

designation of responsibility segments should be based on the following factors: (a) the

entity’s organization structure, (b) its lines of responsibilities and missions, (c) its outputs

(goods or services it delivers), and (d) budget accounts and funding authorities. However,

the predominant factor is the reporting entity’s organization structure and its existing

responsibility components, such as bureaus, administrations, offices, and divisions within a

department.

87. The U.S. General Services Administration, for example, provides five distinct services: (1)

managing public buildings, (2) distributing supplies, (3) providing travel and transportation

services, (4) managing information resources (including communication and data

processing services), and (5) disposal of real properties. Each of those service areas could

be designated as a responsibility segment. The Department of Veterans Affairs (VA), among

its other services, provides health care to veterans, pays veterans’ compensation and

27

This point is discussed in FASAB Statement of Recommended Accounting Concepts No. 2, Entity and Display, pars.

75-76.

SFFAS 4

Page 26 - SFFAS 4 FASAB Handbook, Version 23 (9/24)

pension benefits, and provides home loans and home loan guarantees to veterans. Each of

these program areas could constitute a responsibility segment.

88. Since responsibility segments are major parts of an entity, some segments may carry more

than one program. Some programs may be jointly managed by two or more segments.

Thus, each segment must accumulate costs for each type of output produced for various

programs. To accomplish this, a network of cost centers can be established within a

segment to accumulate costs. Managers of each cost center will be provided with

information to control and manage costs within their area of responsibility. Depending on

operational patterns and cost methods, cost centers can be structured along different

dimensions, such as organizational units, operating processes, and activities.

Full Cost

89. This standard states that reporting entities should measure and report the full costs of their

outputs in general purpose financial reports. “Outputs” means products and services

generated from the consumption of resources. The full cost of a responsibility segment’s

output is the total amount of resources used to produce the output. This includes direct and

indirect costs that contribute to the output, regardless of funding sources. It also includes

costs of supporting services provided by other responsibility segments or entities. The

standard does not require full cost reporting in federal entities’ internal reports or special

purpose cost studies. Entity management can decide on a case-by-case basis whether full

cost is appropriate and should be used for internal reporting and special purpose cost

studies.

Direct Costs

90. Direct costs are costs that can be specifically identified with an output. All direct costs

should be included in the full cost of outputs. Typical direct costs in the production of an

output include:

(a) Salaries and other benefits for employees who work directly on the output;

(b) Materials and supplies used in the work;

Reporting entities should report the full costs of outputs in general purpose financial reports. The full cost

of an output produced by a responsibility segment is the sum of (1) the costs of resources consumed by

the segment that directly or indirectly contribute to the output, and (2) the costs of identifiable supporting

services provided by other responsibility segments within the reporting entity, and by other reporting

entities.

SFFAS 4

Page 27 - SFFAS 4 FASAB Handbook, Version 23 (9/24)

(c) Various costs associated with office space, equipment, facilities, and utilities that are

used exclusively to produce the output; and

(d) Costs of goods or services received from other segments or entities that are used to

produce the output (See discussions and explanations in the next section on “Inter-

Entity Costs”).

Indirect Costs

91. Indirect costs are costs of resources that are jointly or commonly used to produce two or

more types of outputs but are not specifically identifiable with any of the outputs. Typical

examples of indirect costs include costs of general administrative services, general research

and technical support, security, rent, employee health and recreation facilities, and

operating and maintenance costs for buildings, equipment, and utilities. There are two levels

of indirect costs:

(a) Indirect costs incurred within a responsibility segment. These indirect costs should be

assigned to outputs on a cause-and-effect basis, if such an assignment is economically

feasible, or through reasonable allocations. (See discussions on cost assignments in

the “Costing Methodology” section.)

(b) Costs of support services that a responsibility segment receives from other segments

or entities. The support costs should be first directly traced or assigned to various

segments that receive the support services. They should then be assigned to outputs.

92. A reporting entity and its responsibility segments may incur general management and

administrative support costs that cannot be traced, assigned, or allocated to segments and

their outputs. These unassigned costs are part of the organization costs, and they should be

reported on the entity’s financial statements (such as the Statement of Net Costs) as costs

not assigned to programs.

28

Certain Cost Elements

Costs of Employees’ Benefits

93. Employee benefits include:

28

A similar explanation is provided in FASAB Statement of Recommended Accounting Concepts No. 2, Entity and

Display, par. 95.

SFFAS 4

Page 28 - SFFAS 4 FASAB Handbook, Version 23 (9/24)

(a) Health and life insurance benefits for current employees covered in part by the

government’s contribution to health and life insurance premiums;

(b) Pension benefits for employees, their survivors, and dependents, covered by defined

pension plans such as Civil Service Retirement System (CSRS), Federal Employees

Retirement Plan (FERS), and Military Retirement System (MRS);

(c) Health and life insurance benefits for retired employees, their survivors and

dependents, covered in part by the government’s contribution to health and life

insurance premiums, and referred to as “other retirement benefits” (ORB) in this

document;

(d) Other postemployment benefits (OPEB) for terminated and inactive employees, which

include severance payments, training and counseling, continued health care, and

unemployment and workers compensation.

94. Most of the employee benefit programs are covered by trust funds administered by the

Office of Personnel Management (OPM) and the Department of Defense (DoD).

Contributions to the trust funds come from three sources: current and retired employees,

employing agencies, and direct appropriations. The management expenses of the trust

funds are paid with the funds’ receipts.

95. Federal financial accounting standards require that the employing entity accrue the costs to

the federal government of providing pension and ORB benefits to employees and recognize

the costs as an expense when the benefits are earned.

29

The employing entity should

recognize those expenses regardless of whether the benefits are funded by the reporting

entity or by direct appropriations to the trust funds. This principle should also be applied to

health and life insurance benefits for current employees and comparable benefits for military

personnel. The costs of employee benefits incurred by responsibility segments should be

directly traced or assigned to outputs.

96. OPEB costs include severance payments, counseling and training, health care, and workers

compensation benefits paid to former or inactive employees. OPEB costs are often incurred

as a result of such events as reductions in force or on-the-job injuries of employees. Federal

financial accounting standards require that OPEB costs be reported as an expense for the

period during which a future outflow or other sacrifice of resources is probable and

measurable on the basis of events occurring on or before the accounting date.

30

29

FASAB Exposure Draft, Accounting for Liabilities of the Federal Government

(November 7, 1994), pars. 62-99.

30

Ibid., pars. 100-102.

SFFAS 4

Page 29 - SFFAS 4 FASAB Handbook, Version 23 (9/24)

97. Since the recognition of OPEB costs is linked to the occurrence of an OPEB event rather

then the production of output, in many instances, assigning OPEB costs recognized for a

period to output of that period would distort the cost of output. In special purpose cost

studies or cost findings, management may distribute OPEB costs over a number of years in

the past to determine the costs of the outputs that the OPEB recipients helped to produce.

Costs of Public Assistance and Social Insurance Programs

98. Major costs of welfare, insurance, and grant programs are the costs of resources transferred

from the federal government to individuals and state and local governments. Some of them

are referred to as “transfer payments.” The following are some typical public assistance and

insurance programs:

• Grants, such as aid to state and local governments;

• Subsidies, such as agricultural commodity price support and stabilization programs;

• Credit and insurance costs, such as the Family Education Loan Program and Savings

Association Insurance;

• Welfare payments such as Aid to Families with Dependent Children (AFDC); and,

• Social insurance, such as the Old Age, Survivors, and Disability Insurance Program.

99. The full cost of such a program includes: (a) the costs of federal resources that have been

or will be transferred to individuals and state/local governments, and (b) the costs of

operating the programs. These two types of costs should be recognized on a basis of

accounting that is prescribed within the Federal Financial Accounting Standards. These two

types of costs should be separately identified so that each can be used for different analytic

purposes.

100. The costs resulting from transfer payments are determined by the level of grants, subsidies,

entitlement benefits, credit subsidies, or loss payments made under insurance and

guarantee agreements. They are also determined by the number of eligible persons who

receive the transfer payments. The program cost of AFDC, for example, depends on the

average payment per family, the number of eligible families, and the federal government’s

share in the payments (some payments are made by state and local governments).

Information on this type of cost is useful for making policy decisions about levels of

subsidies or benefits, eligibility of recipients, and how transfer payments are made. This cost

information is also useful for measuring the cost-effectiveness of a transfer payment

program.

101. Program operating costs, on the other hand, are costs of managing the program and

delivering the payments. They include the costs of personnel, supplies, equipment, and

offices. The costs are related to such activities as screening benefit recipients for eligibility,

SFFAS 4

Page 30 - SFFAS 4 FASAB Handbook, Version 23 (9/24)

keeping their accounts, making payments and collections, answering inquiries, etc.

Information on this type of cost is useful in measuring the efficiency of program operations.

Costs related to Property, Plant and Equipment

102. Depreciation expense. General property, plant, and equipment are used in the production

of goods and services. Their consumption is recognized as depreciation expense. The

depreciation expense incurred by responsibility segments should be included in the full

costs of the goods and services that the segments produce.

103. Recognizing property acquisition costs as expenses. The costs of acquiring or

constructing federal mission and heritage property, plant, and equipment may be charged to

expenses at the time the acquisition costs are incurred.

31

Since the recognition of these

expenses is linked to property acquisition rather than production of goods and services,

those expenses should not be included in the full costs of goods and services. However,

they are part of the costs of the entity or the program that makes the property acquisitions.

Non-production costs

104. A responsibility segment may incur and recognize costs that are linked to events other than

the production of goods and services. Two examples of these non-production costs were

discussed earlier: (1) OPEB costs that are recognized as expenses when an OPEB event

occurs, and (2) certain property acquisition costs that are recognized as expenses at the

time of acquisition. Other non-production costs include reorganization costs, and

nonrecurring cleanup costs resulting from facility abandonments that are not accrued. Since

these costs are recognized for a period in which a particular event occurs, assigning these

costs to goods and service produced in that period would distort the production costs. In

special purpose cost studies, management may have reasons to determine historical output

costs by distributing some of these costs to outputs over a number of past periods. Such

distribution may be appropriate when: (a) experience shows that the costs are recurring in a

regular pattern, and

(b) a nexus can be established between the costs and the production of

outputs that may have benefited from those costs.

31

In FASAB Exposure Draft, Accounting for Property, Plant, and Equipment, the Board proposed that the costs of

acquiring or constructing “federal mission” and “heritage” property, plant, and equipment be recognized as expenses

when the costs are incurred. See the ED, pars. 98-117, pages 29-34.

SFFAS 4

Page 31 - SFFAS 4 FASAB Handbook, Version 23 (9/24)

Inter-entity Costs

105. As stated in the preceding standard, to fully account for the costs of the goods and services

they produce, reporting entities should include the cost of goods and services received from

other entities. Knowledge of these costs is helpful to top level management in controlling

and assessing the operating environment. It is also helpful to other users in evaluating

overall program costs and performance and in making decisions about resource allocations

and changes in programs.

Inter-entity Activities

106. Within the federal government, some reporting entities rely on other federal entities to help

them achieve their missions. Often this involves support services, but may include the

provision of goods. Sometimes these arrangements may be stipulated by law, but others are

established by mutual agreement of the entities involved. Such relationships can be

classified into two types depending upon funding methods.

• Provision of goods or services with reimbursement

—In this situation, one entity agrees

to provide goods or services to another with reimbursement at an agreed-upon price.

The reimbursement price may or may not be enough to recover full costs. Usually the

agreement is voluntarily established through an inter-agency agreement. Revolving

funds can also be included in this group, because they are usually established to

recover costs through sale of their outputs to other government entities. They are

usually meant to be self-sustaining through their sales, without receiving additional

appropriations. However, they do not always charge enough to cover full costs.

• Provision of goods or services without reimbursement

—One entity provides goods or

services to another entity free of charge. The agreement may be voluntary, legally

mandated, or inherently established in the mission of the providing entity.

107. Recently, consideration has been given to expanding the concept of inter-entity support

within the federal government. Under this concept, entities could sell their outputs on a

competitive basis. Entities would have the authority to purchase goods or services from any

federal or private provider. This is seen as a way to improve government efficiency through

Each entity’s full cost should incorporate the full cost of goods and services that it receives from other

entities. The entity providing the goods or services has the responsibility to provide the receiving entity

with information on the full cost of such goods or services either through billing or other advice.

Recognition of inter-entity costs that are not fully reimbursed is limited to material items that (1) are

significant to the receiving entity, (2) form an integral or necessary part of the receiving entity’s output, and

(3) can be identified or matched to the receiving entity with reasonable precision. Broad and general

support services provided by an entity to all or most other entities should not be recognized unless such

services form a vital and integral part of the operations or output of the receiving entity.

SFFAS 4

Page 32 - SFFAS 4 FASAB Handbook, Version 23 (9/24)

competition since inefficient government providers would be forced to improve or stop

providing these goods or services. This could result in consolidating support services in

fewer governmental entities. Underlying this concept is the requirement that all costs be

recognized in developing the price at which goods and services would be sold to other

entities.

Accounting And Implementation Guidance

31A

108. If an entity provides goods or services to another entity, regardless of whether full

reimbursement is received, the providing entity should continue to recognize in its

accounting records the full cost of those goods or services. The full costs of the goods or

services provided should also be reported to the receiving entity by the providing entity.

109. The receiving entity should recognize in its accounting records the full cost of the goods or

services it receives as an expense or, if appropriate, as an asset (such as work-in-process

inventory). The information on costs of non-reimbursed or under-reimbursed goods or

services should be available from the providing entity. However, if such cost information is

not provided, or is partially provided, a reasonable estimate may be used by the receiving

entity. The estimate should be of the cost of the goods or services received (the estimate