exception \ik- sep-sh n\ n ... 2: one that is excepted;

esp : a case to which a rule does not apply

Webster’s 9th Edition

e

,

Maximum Assessed Value Manual

There are always exceptions...

150-303-438 (Rev. 05-18)

i

Section 1: Maximum assessed value and assessed value ............................................................................... 1-1

Section 2: Introduction to property classication. ........................................................................................... 2-1

Section 3: Changes to property and the changed property ratio .................................................................. 3-1

Section 4: New property or new improvements ............................................................................................. 4-1

Section 5: General ongoing maintenance and repair (GOMAR) ................................................................... 5-1

Section 6: Minor construction ............................................................................................................................ 6-1

Section 7: Rezoned and used consistently with the rezoning ....................................................................... 7-1

Section 8: Subdivided or partitioned property ................................................................................................ 8-1

Section 9: Omitted property ............................................................................................................................... 9-1

Section 10: Exemption, partial exemption, and special assessment ............................................................. 10-1

Section 11: Lot line adjustments .........................................................................................................................11-1

Section 12: Destroyed or damaged property ................................................................................................... 12-1

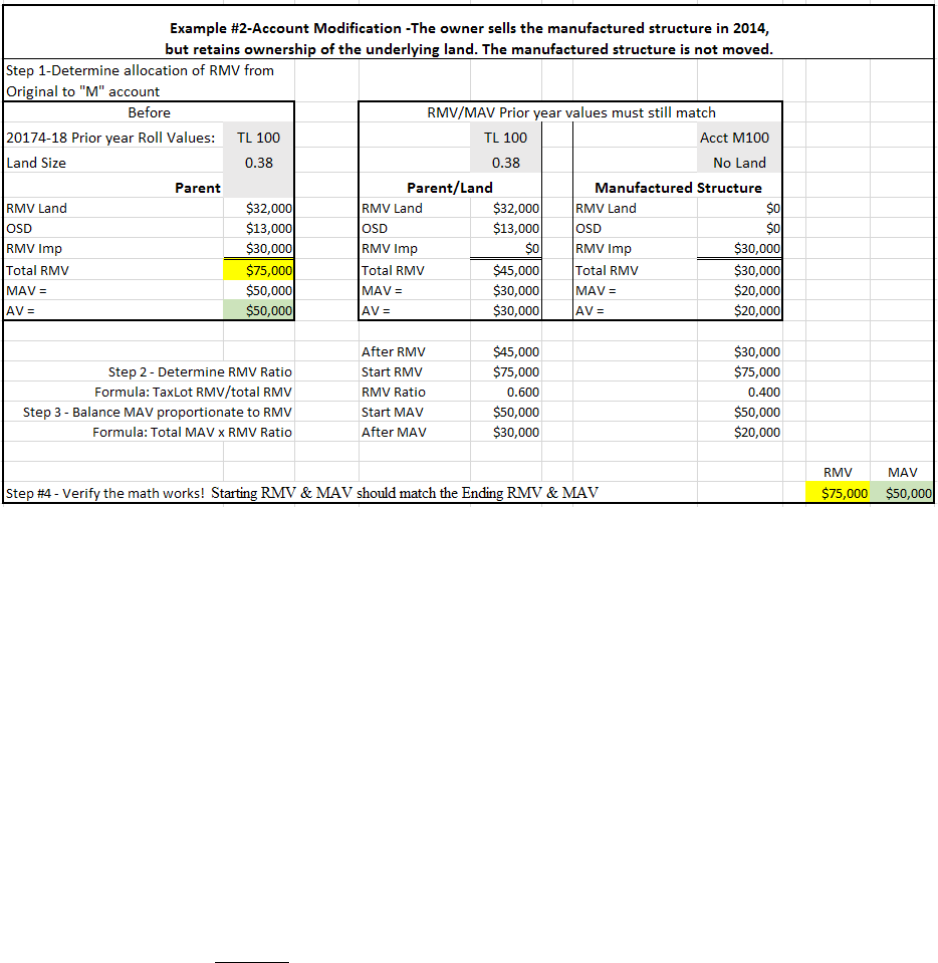

Section 13: Property tax account modications ............................................................................................... 13-1

Section 14: Maximum assessed value corrections ........................................................................................... 14-1

Section 15: Manufactured structure exception guidelines ............................................................................. 15-1

Section 16: Calculation ordering when multiple exceptions occur .............................................................. 16-1

Section 17: Appendix ........................................................................................................................................... 17-1

Table of contents

150-303-438 (Rev. 05-18)

150-303-438 (Rev. 05-18)

1-1

In November 1996, Oregon voters passed Measure 47, a citizen initiative and constitutional amendment.

It rolled back property taxes for each property in the state (not assessed values) for the 1997–98 tax year

to the 1995–96 level and restricted increases in taxes to no more than 3 percent per year. There were a

number of technical problems with Measure 47, so the 1997 Legislature drafted Measure 50 to replace it.

Measure 50 was passed by voters in May 1997.

Measure 50 replicated the tax cuts intended by Measure 47, but focused on taxable values and tax rates,

rather than taxes. The principal features of the measure were a “cut” and “cap.” The “cut” rolled back a

property’s taxable value and reduced taxing district levies. In addition, most local government tax levies

were replaced with permanent tax rates. Measure 50 introduced maximum assessed value, which acts as

a “cap” on the growth of taxable (assessed) value for most property.

How it works:

Measure 50 initially established MAV for all assessable properties as 10 percent less than the 1995–96 real

market value (RMV). MAV growth is limited to 3 percent per year. Combined with permanent tax rates,

Measure 50 effectively limited tax increases, except under specific circumstances.

Maximum assessed value defined ORS 308.146 (1)

Property: All property included within a single property tax account, except for property centrally

assessed by the department, for which property means the total statewide value.

Property tax account: The division of property for purposes of listing it on the assessment roll.

Each property that isn’t exempt or specially assessed has a MAV and an assessed value (AV) as described

in statute:

ORS 308.146 (1). The maximum assessed value of property equals 103 percent of the property’s assessed

value from the prior year or 100 percent of the property’s maximum assessed value from the prior year,

whichever is greater.

Based on the statute, there are only two possible outcomes to what value becomes the MAV; it’s either the

prior year’s assessed value multiplied by 1.03 or the prior year’s MAV—whichever is greater. In addition,

the following conditions apply:

• MAV can’t increase by more than three percent (the maximum); or

• MAV may increase anywhere between -0- and 3 percent each year; or

• MAV can’t change (it freezes) in the year after RMV falls over 3 percent below MAV.

Let’s demonstrate how MAV is calculated so we can test these conditions and provide some concrete

examples. This is the first test and it is often referred to as “The 103 percent test”.

Maximum Assessed Value (MAV). The 103 percent test:

• Calculate the prior year’s assessed value x 1.03.

• Compare to prior year’s maximum assessed value.

• Whichever is greater becomes the current maximum mssessed value (MAV).

Section 1—Maximum assessed value (MAV)

and Assessed value (AV)

150-303-438 (Rev. 05-18)

1-2

MAV Chart 1: The 103 percent test; “Prior year AV x 1.03” is greater than “Prior MAV”,

therefore the prior year Av x 1.03 becomes the current MAV.

Explanation of MAV Chart 1:

• Column (1) shows the prior year assessed value (AV) of $229,068.

• Column (2) shows the calculation to establish current MAV: Prior year AV ($229,068) multiplied by 1.03

equals $235,940.

• Column (3) shows the prior year maximum assessed value (MAV) ($229,068).

• Compare column (2) to column (3), whichever one is greater becomes the new MAV ($235,940).

• In this instance, the prior year AV x 1.03 is greater than the prior MAV and prior year AV x 1.03 becomes

current (new) MAV (4).

In the above example, MAV increased to the maximum 3% allowed by law.

MAV Chart 2: The 103 percent test; “Prior MAV” is greater than “Prior AV x 1.03”,

therefore the prior MAV becomes the current MAV.

150-303-438 (Rev. 05-18)

1-3

Explanation of MAV Chart 2:

• Column (1) shows the prior year assessed value (AV) of $198,568.

• Column (2) shows calculation: Prior year AV ($198,568) multiplied by 1.03 equals $204,525.

• Column (3) shows the prior year maximum assessed value (MAV) (226,518).

• Compare column (2) to column (3), whichever one is greater becomes the new MAV ($226,518).

• In this instance, the prior year MAV is greater and becomes the current MAV (4).

Note: MAV can’t change in a year after RMV falls below MAV.

There are conditions when MAV doesn’t increase the full 3% and when MAV will freeze until the

market/RMV increases above MAV.

MAV Chart 3: The 103 Percent Test; MAV Increases by less than 3%:

One MAV per account

Oregon Revised Statute (ORS) 308.215 requires that RMV of land be listed on the assessment roll

separately from all buildings, structures, and improvements on the land. However, Measure 50 provides

that MAV be established for each unit of property in the state. By requiring each unit of property to have

an MAV, the Supreme Court determined that each tax account will have an MAV. MAV isn’t separately

determined for the land and the buildings within the tax accounts. Refer to Flavorland Foods v. Washington

County Assessor and Dept. of Revenue, 344 Or. 562, 54 P.3d 582 (2002) in the appendix.

Uniformity in taxation not required for MAV

The Oregon Constitution requires that any assessment of taxes be done uniformly on the same class of

subjects throughout the state. However, Measure 50 added another section to the Oregon Constitution

that exempts itself from the uniformity requirements.

MAV is strictly driven by a mathematical formula. After it’s established, it’s no longer linked to RMV

beyond the possible effect of the 103 percent test. Because of this, the framers of Measure 50 understood

that it’s somewhat artificial and arbitrary.

For a variety of reasons, two houses side-by-side with the same RMV may have dramatically different

MAVs, and, therefore, dramatically different tax burdens.

Assessed value defined

AV equals either MAV or RMV, whichever is less.

AV is the value used to calculate the taxes assessed on property. For most properties, RMV is substantially

greater than MAV, so AV is limited to equaling MAV. However, for various reasons, including a declining

market, a property’s RMV may be less than MAV. In that case, the property is assessed at its RMV.

AV must be calculated after MAV.

150-303-438 (Rev. 05-18)

1-4

After maximum assessed value (MAV) is calculated (103 percent test), perform the second test—

whichever is less wins this test:

• Compare current maximum assessed value (MAV) to RMV.

• Whichever one is less becomes the New Assessed Value (AV).

• AV is the value used to calculate the taxes assessed on property and can’t exceed RMV.

Just remember: Whichever is less wins this test.

AV Chart 5: The Second Test: Which is less? Current MAV or RMV?

Current MAV is less than RMV and becomes New AV.

Explanation of AV Chart 5:

Tax year 09–10:

• Column (4) shows the current MAV ($219,920) (The 103 percent test result).

• Column (5) shows the RMV ($224,624) compare, and

• Whichever is less wins this test and becomes the new AV (column 6).

• Result: For year 09–10, Current MAV is less and becomes new AV ($219,920).

150-303-438 (Rev. 05-18)

1-5

AV Chart 6: The second test: Which is less? Current MAV or RMV?

Current RMV is less than MAV and becomes the new AV.

Explanation of AV Chart 6:

Tax year 10–11:

• Column (4) shows the current MAV ($226,518) (The 103 percent test result).

• Column (5) shows the RMV ($190,931) compare and discover that the RMV is less.

• Whichever is less wins this test and becomes the new AV.

• Result: For tax year 10–11, RMV is less and becomes new AV ($190,931) (column 6).

Note: When a property or market is declining, a property’s RMV may fall below or be less than the MAV.

When this occurs, the RMV becomes the AV and MAV freezes and doesn’t change in a year after RMV

falls more than 3% below MAV. If RMV is below MAV, but is within 3%, then MAV may increase by less

than 3%.

Note: What happens in tax year 11–12 and tax year 12–13?

Both Tax Years indicate the RMV is less than the MAV. Remember that AV can’t exceed RMV and that

MAV “freezes” and doesn’t change in a year after RMV falls more than 3% below MAV.

150-303-438 (Rev. 05-18)

1-6

AV Chart 7: The Second Test: Which is less? Current MAV or RMV?

Current MAV is less than RMV and becomes the new AV.

Explanation of AV Chart 7:

Tax year 13–14:

• Column (4) shows the current MAV ($229,068) (The 103 percent test result).

• Column (5) shows the RMV ($249,084). Compare and discover that the current MAV is now less.

• Whichever is less wins this test and becomes the new AV.

• Result: For tax year 13–14, current MAV is less and becomes new AV ($229,068) (column 6).

Note: Since the RMV is greater, MAV is no longer “Frozen” and can continue to increase up to the 3%

limit.

150-303-438 (Rev. 05-18)

1-7

Relationship of RMV, MAV, and AV

Using one property as an example, real market value has been plotted on the chart below.

The RMV, as assessed, in year 2003–04 was approximately $260,000 and, over the course of the next 11

years, the RMV went as high as $330,000 and as low as $190,000 ending the timeframe illustrated at

$300,000.

2003–04

2004–05

2005–06

2006–07

2007–08

2008–09

2009–10

2010–11

2011–12

2012–13

2013–14

2014–15

$160,000

$180,000

$200,000

$220,000

$240,000

$260,000

$280,000

$300,000

$320,000

$340,000

Value

RMV

Tax year

150-303-438 (Rev. 05-18)

1-8

By adding MAV to our chart (in Red), the relationship of MAV and RMV becomes clearer. When the RMV

is below MAV, MAV is primarily a straight and level line. By definition, MAV is determined by comparing

103 percent of the previous year’s AV to the previous year’s MAV. The greater amount becomes the new

MAV. Since MAV can always be, at a minimum, equal to its prior year’s MAV, it will never go down in the

“normal” course of events’ such as if the property doesn’t change, meaning that a qualifying event that

allows the MAV to increase or decrease hasn’t occurred.

In 2003–04, this property’s MAV was approximately $190,000. The MAV steadily increased from -0- to 3

percent (when allowed) over the next 14 years to approximately $245,000 in MAV for 2014–15.

RMV vs MAV

RMV

MAV

2003–04

2004–05

2005–06

2006–07

2007–08

2008–09

2009–10

2010–11

2011–12

2012–13

2013–14

2014–15

$160,000

$180,000

$200,000

$220,000

$240,000

$260,000

$280,000

$300,000

$320,000

$340,000

Value

Tax year

Note the following:

In 2008–09 MAV = $220,000 (approximate values)

In 2009–10 MAV = $226,800

In 2010–11 MAV = $226,800

In 2011–12 MAV = $226,800

In 2012–13 MAV = $231,500

Why did the MAV stop increasing in Tax years 2009–10, 2010–11, and 2011–12?

When the RMV dips below MAV, MAV “freezes” and doesn’t change in a year after RMV falls at least 3%

below MAV. In 2012–13, RMV increases well above the MAV. However, due to a second test, determining

AV, MAV didn’t increase the full 3%. Let’s take a look at the second test.

150-303-438 (Rev. 05-18)

1-9

The next chart adds the third component, AV (represented in yellow). This is established by comparing

RMV to MAV, whichever is less wins this test and becomes the new AV.

RMV vs MAV vs AV

RMV

MAV

AV

2003–04

2004–05

2005–06

2006–07

2007–08

2008–09

2009–10

2010–11

2011–12

2012–13

2013–14

2014–15

$160,000

$180,000

$200,000

$220,000

$240,000

$260,000

$280,000

$300,000

$320,000

$340,000

Value

Tax year

150-303-438 (Rev. 05-18)

1-10

From 2003–04, AV follows the MAV line up to the point it crosses RMV in 2008–09, then it follows the

RMV—the RMV is less and wins the 2nd test).

Historically, in 2003–04, this property’s taxes were based on approximately $190,000 in AV. Notice that the

RMV was $260,000 and the MAV became the AV as MAV was less. The RMV increased significantly in the

next few years and yet, due to Measure 50, the property’s MAV had a maximum 3% increase over those same

years and the MAV became the AV as it was the lesser value in the 2nd test.

When the RMV (market) declined (from 2006 through 2009–10), the MAV won the test and became the AV

because it was still less than the RMV. MAV continued to increase by 3% until the RMV declined below the

MAV, then MAV “froze” and the RMV won the test and became the new AV.

In 2008–09, the RMV significantly dropped below MAV and the RMV became the basis for calculating

the AV for taxes; approximately 14% less than the previous year. This illustrates that AV isn’t tied to the 3%

increase in MAV. From 2009 through 2010–11, the taxpayer continued to benefit from lower taxes because the

RMV was lower.

In 2011–12, the RMV came within 3% of RMV. In 2012–13 MAV did increase but not up to the maximum 3%.

Then the RMV began increasing rapidly; it crossed back above the MAV allowing the MAV to begin

increasing up to the 3% limit as designed by Measure 50.

This next chart is a close-up of a single property that experienced large fluctuations over 4 years. For

illustration purposes, values have been added and are approximate.

Two things are illustrated in this very short period of time: MAV may increase by less than the 3% and AV

can increase or decrease more than the 3% MAV limit because AV is calculated based on the previous year’s

AV or RMV, whichever is less.

150-303-438 (Rev. 05-18)

1-11

Both tests are performed annually:

In year 1: First test; Prior MAV ($220,000) is greater than prior years AV x 1.03 = $219,000. MAV is greater

and becomes new MAV. RMV plunged downward from $227,000 to $190,000. Second test: Compare RMV

($190,000) to the new MAV ($220,000); RMV is less and becomes new AV. This is roughly an 18% decline in

assessed value.

In year 2: First test: Prior year’s MAV ($220,000) is greater than prior years AV ($190,000) x 1.03. Prior year

MAV ($220,000) becomes the new MAV and MAV doesn’t increase; it can’t change in the year after RMV

remains over 3 percent below MAV. RMV compared to new MAV, which is less? RMV becomes assessed

value.

In year 3, First test: Prior year’s MAV is greater than prior year AV x 1.03. Prior year MAV becomes the new

MAV. RMV, which is slightly less than MAV, becomes AV. Note that AV increased by approximately 12%.

In year 4, two things occurred:

• RMV increased above prior year’s MAV allowing MAV to begin to move again.

• Prior AV x 1.03 was higher than existing MAV so MAV increased, but by less than 3%. AV increased by 3%.

This last chart is an example of the convergence of the three values and illustrates that MAV may increase

any amount between -0- and the maximum 3 percent. In this scenario, MAV increased only 1 percent

between years 2 and 3. In year 3, RMV crossed above the MAV and increased well above 3 percent which

allowed the MAV to continue upward increasing at the maximum 3% in year 4.

RMV

MAV

AV

Time

RMV

Year 1 Year 2

Year 3

Year 4

AV set by

the RMV

AV set by

the MAV

Recap: Measure 50 established the 1997–98 maximum assessed value (MAV) as 90% of a property’s

1995–96 real market value (RMV) and established assessed value (AV) which can’t be greater than RMV.

Each year the two tests are performed to establish MAV and AV for each account that requires MAV in

the assessment year.

150-303-438 (Rev. 05-18)

1-12

Test 1: Establish MAV: The 103 Percent Test:

• Calculate the prior year’s assessed value x 1.03.

• Compare to prior year’s maximum assessed value.

• Whichever is greater becomes the current maximum assessed value (MAV).

• MAV can’t increase by more than three percent (the maximum); or

• MAV may increase anywhere between -0- and 3 percent each year; or

• MAV can’t change (freezes) in the year after RMV falls more than 3% below MAV.

Test 2: Establish AV: Second test; Whichever is less wins this test:

• Compare current maximum assessed value (MAV) to RMV.

• Whichever one is less becomes the new assessed value (AV).

In addition:

• MAV is strictly driven by a mathematical formula.

• MAV will never go down in the normal course of events.

• MAV isn’t fair. For a variety of reasons, two houses side-by-side with the same RMV may have dramati-

cally different MAV’s and, therefore, dramatically different tax burdens:

• AV can increase or decrease more than the 3% MAV limit.

• Measure 50 also changed the property tax system from “levy based” to a permanent rate based system.

150-303-438 (Rev. 05-18)

2-1

Section 2—Introduction to basic property

classification

Before we can delve into exceptions to the MAV limitation, we must cover some basic foundational

practices. It may seem strange to begin our discussion on exceptions to MAV by looking at the property

classification system but being able to understand how each individual parcel of property is classified is

necessary to fundamentally ensure that properties are treated uniformly. In order to assess the thousands

of properties that exist in each county the assessor must classify and assign a property classification code

number that supports the highest and best use of the property. For example, single family homes that are

being used as a home are identified as residential use, whereas a retail grocery store would be identified

as commercial use a different property classification entirely.

Property classification has a rational basis and helps to protect the uniformity of classification of

property. Once assigned, most parcels of property maintain the same property class annually. These

classifications organize the data for future observations, calculations and annual studies.

OAR 150-308-0310 governs property classification. The assessment roll must include the property

classification code number for each parcel of real property in the county, except for those properties

assessed by the department under ORS 308.505 to 308.665 (utilities, railcars). All classifications must be

based upon highest and best use of the property. The term “highest and best use” is defined in OARs

150-308-0240 and 150-308-0260. The class associated with the property may or may not be its current use.

(8) Denitions for property classication system:

The property classification system uses a three-digit number to represent all property types and the

assessor is required to maintain the proper classification on each parcel of property based on highest and

best use of the property.

The first digit of the property class system also determines “primary type of use” of the property. The Property

class is the basis for compiling the data for calculating the changed property ratio (CPR). In order to compute

the exception MAV and add the associated increase in exception value to the assessment role, the RMV and

150-303-438 (Rev. 05-18)

2-2

MAV of all the unchanged properties in each property class is arrived at first. Without this information, it

wouldn’t be possible to calculate the exception ratio (CPR) for all the properties that have changed.

In addition, there are some instances when the property classification on record changes in a given year

as outlined in:

OAR 150-308-0100 Determining maximum assessed value when the property class is

changed.

(1) The single act of changing the property classification, described in OAR 150-308-0310, to better

reflect the highest and best use of the property, doesn’t qualify as an exception to the 3 percent limitation

on growth in the maximum assessed value (MAV), as described in ORS 308.146(1).

(2) Any exception value added to the base MAV after the change is made to the property class will be

calculated by applying the changed property ratio of the current property class to the real market value of

any qualified exception identified in ORS 308.146.

This rule illustrates that more than just the “single act” of changing the property classification need to

occur in order to qualify for an exception to MAV increase. It does outline which property class will be

utilized when making the adjustments. This may be an occasion when the new property class CPR would

be appropriate for calculating the exception MAV when a qualifying event has occurred.

More on these types of exceptions will be covered in later sections.

Recap: Property classification is foundational; if you have the correct classification, you can ascertain the

overall value of each property and, when properties are deemed affected by allowed exceptions, the correct

adjustments to maximum assessed value can be achieved.

The first digit of the property class determines the property type and this is used for calculating the CPR

for each property class and allows for new property to receive the benefit of Measure 50.

150-303-438 (Rev. 05-18)

3-1

Specific types of changes to the property that increase RMV can change MAV more than the 3 percent

limit. These changes are referred to as “exceptions” because they represent exceptions to the normal 3

percent limit. For a change to qualify as an exception, it must fall within one of the following:

• New property or new improvements to property.

• The property has been partitioned or subdivided.

• The property has been rezoned and is being used consistent with the rezoning.

• Previously omitted property has now been taken into account.

• The property has been disqualified from exemption, partial exemption, or special assessment.

• A lot line adjustment is made, but the total assessed value of all property affected by the adjustment

won’t exceed the total MAV the property would have had if the lot line adjustment hadn’t occurred.

Changed property ratio (CPR)

To determine the adjustment to MAV for an exception, the general rule is to multiply the RMV of the

exception (the value of the changed property) by the CPR and add the product to MAV. This provides the

changed property the same Measure 50 benefits as property that originally existed in 1995.

The classification system described in Section 2 organizes the data for the calculation of the CPR.

However, only the first digit of the property class (representing highest and best use) needs to be

considered for purposes of calculating the CPR. Therefore xx represent the second and third digits in the

following list of classifications:

0xx—Miscellaneous 1xx—Residential

2xx—Commercial 3xx—Industrial

4xx—Tract 5xx—Farm

6xx—Forest 7xx—Multi-family

8xx—Recreation

The CPR for each property classification represents all property within the county for that classification.

The CPR is calculated as the following ratio:

Average MAV of unchanged property

CPR =

_________________________________

Average RMV of unchanged property

The average MAV is the total of MAVs for all properties in a class divided by the number of accounts for

that class. Properties with exceptions aren’t included in the calculation of the average MAV.

The average RMV is the total of RMVs for all properties in a class divided by the number of accounts for

that class. Properties with exceptions aren’t included in the calculation of the average RMV.

For properties that are partially specially assessed, only the portions not specially assessed will be

used to calculate the ratio. Property classes may be combined to arrive at a ratio. The resulting ratio

would become the CPR for each property class used to calculate the ratio. Property class 1xx includes all

manufactured structures and floating homes not assigned to other property classes.

Section 3—Changes to property and the

changed property ratio

150-303-438 (Rev. 05-18)

3-2

OAR 150-308-0170 Establishing a Changed Property Ratio (CPR)

(1) The assessor must establish a CPR for property classes -0- through 8 each assessment year. For

determining the ratio of the average maximum assessed value over the average real market value, only the

first digit of the property class needs to be recognized. These ratios must be rounded to three decimals.

(a) Property classes may be combined to arrive at a ratio. The resulting ratio would become the CPR for

each property class used to calculate the ratio.

(b) For specially assessed properties, only the non-specially assessed portion of value will be used to

determine a ratio. For specially assessed properties such as farm or timber, the assessor may use either of

the following methods to arrive at a CPR:

(A) The non-specially assessed portion of the unchanged 5-x-x or 6-x-x property classes may be used to

create the CPR for those classes; or,

(B) The 4-x-x property class values may be combined with the non-specially assessed values from the

5-x-x and/or 6-x-x property classes to calculate the ratio. The resulting ratio would become the CPR for each

property class used to calculate the ratio.

(2) Residential property class (1-x-x) includes all manufactured structures and floating homes not

assigned to other property classes.

(3) For locally and centrally assessed property, the value of the CPR may not be greater than 1.000.

OAR 150-308-0140 Computation of Changed Property Ratio for Centrally Assessed

Property

The ratio of average maximum assessed value to average real market value, also known as the changed

property ratio, shall be rounded to two decimal places for purposes of assessed value calculation. See

also OAR 150-308-0570. Note: Centrally assessed properties are only assessed by the Department of

Revenue.

In addition, for properties that are partially specially assessed, only the portions not specially assessed

will be used to calculate the ratio.

Property classes may only be combined as stated in OAR 150-308-0170 to arrive at a ratio.

In the case of a zone change that actually impacts the first digit of the property class, here is the authority

to utilize the current (new) property type to determine CPR calculations:

OAR 150-308-0100 Determining Maximum Assessed Value when the Property Class is

changed

(1) The single act of changing the property classification, described in OAR 150-308-0310, to better

reflect the highest and best use of the property, doesn’t qualify as an exception to the 3 percent limitation

on growth in the maximum assessed value (MAV), as described in ORS 308.146(1).

(2) Any exception value added to the base MAV after the change is made to the property class will be

calculated by applying the changed property ratio of the current property class to the real market value of

any qualified exception identified in ORS 308.146.

Calculating the CPR—Changed property ratio

To determine the annual CPR ratios for each property class involves a step by step procedure and

is in conjunction with certifying the assessment roll. This may be performed by a data analyst as it

encompasses thousands of properties on the roll.

150-303-438 (Rev. 05-18)

3-3

Once the adjustments to RMV for all properties has been certified, the average MAV and average RMV

are then calculated for all unchanged properties following the rule for establishing CPRs (including the

rounding parameters). The resulting CPR ratio for each property classification has now been completed

and will be utilized for making adjustments to MAV for properties having allowable changes in

exception value.

Step 1—Compute the average MAV: The average MAV is the total of MAV for all properties in a

class divided by the number of accounts for that class. Properties with exceptions are not included in the

calculation of the average MAV.

Step 2—Compute the average RMV: The average RMV is the total of RMV for all properties in a

class divided by the number of accounts for that class. Properties with exceptions are not included in the

calculation of the average RMV.

Step 3—Compute the CPR for the property class and remember: These ratios must be rounded to three

decimals for all property types except centrally assessed:

CPR =

Average MAV of unchanged property in the same area in the same property class.

Average RMV of unchanged property in the same area in the same property class.

Industrial property

Industrial property is generally dominated by real property machinery and equipment. Since machinery

and equipment depreciate over time, they will generally have a CPR of one. However, some industrial

warehouses aren’t significantly different than commercial warehouses. This results in similar types

of buildings receiving significantly different MAVs when they are first constructed, which leads to

protracted litigation.

In 2012, the Oregon Legislature addressed this problem by requiring real property machinery and

equipment to be classified separately. The legislation also classified industrial property, which is

appraised by the department under ORS 306.126 separately. Industrial property, other than machinery and

equipment, appraised by the county assessor is combined with commercial property to calculate the CPR.

The goal of each of the remaining sections will be for the reader to have the ability to:

• Determine if an exception to the 3 percent growth limitation of MAV is allowable by law.

• Calculate exception values correctly for each circumstance.

• Clearly explain the MAV adjustments to tax payers, BoPTA, and others with a need to know.

We will be covering each of the exception events listed in ORS 308.146(3) and at the beginning of this

section. Some of these sections require more complex calculations so we may address them out of the

sequence they appear in statute.

There are procedures for each exception; those will be listed before the actual examples including

calculations take place. Becoming familiar with each nuance is an important part of applying exception

value correctly.

150-303-438 (Rev. 05-18)

4-1

New property and new improvements to property are common exception events. First, we will cover some

definitions and test our knowledge on which definition qualifies in a couple of scenarios. After we are confident

in relating to the definitions, actual math examples will be given in this chapter for ease of application. We will

then show a more complex scenario-that of adding an addition to an already existing improvement. These will

assist in building foundational knowledge for more complex situations that may arise.

Denitions:

New construction: Any new structure, building, addition, or improvement to the land (including site

development).

Reconstruction: Building or replacing the existing structure with one of comparable utility.

Major addition: An addition with an RMV of over $10,000 and that adds square footage to an existing

structure.

Remodeling: A type of renovation that changes the basic plan, form, or style of the property.

Renovation: The process by which older structures or historic buildings are modernized, remodeled, or

restored.

Rehabilitation: To restore to a former condition without changing the basic plan, form, or style of the

structure.

If you build a brand new home on bare land, does this qualify for exception MAV? If so, which definition

supports this conclusion?

• New construction? Yes, this is a brand new structure.

• Reconstruction? No, this did not replace the existing structure.

• Major addition? No, no square footage was added.

• Remodeling? No, this didn’t change a basic plan, form or style of the property.

• Renovation? No, it’s not an older or historic structure being modernized, remodeled, or restored.

• Rehabilitation? No, it wasn’t restored to a former condition.

If you upgrade your kitchen in your 2010 home, which adds $28,000 in value to your home, does this qualify

for exception MAV? Which definition supports this conclusion?

• New construction? No, not a new structure.

• Reconstruction? No, this didn’t replace the existing structure.

• Major addition? No, no square footage was added.

• Remodeling? Yes, the upgrade resulted in a renovation that changed the basic plan, form or style.

• Renovation? No, it’s not an older or historic structure being modernized, remodeled, or restored.

• Rehabilitation? No, it wasn’t restored to a former condition.

Manufactured structures or floating homes

New property and/or improvements exceptions for manufactured structures or floating homes can be

from siting, installation, or rehabilitation.

Section 4—Calculating MAV for new property

or new improvements

150-303-438 (Rev. 05-18)

4-2

Other changes

New property and/or improvements exceptions can also result from the addition of:

• Machinery.

• Fixtures.

• Furnishings.

• Equipment.

• Other taxable real or personal property.

Property moved between tax code areas

Property is considered to be new or improved if taxable property is located in a different tax code area on

January 1 of the current assessment year than on January 1 of the preceding assessment year.

Retirements

Value attributable to new property and/or new improvements may be offset by value loss due to

retirements in the same year. Adjustments to MAV are based on the net increase in RMV after deduction

for retirements, multiplied by the CPR for the property’s class. Offsets due to value loss by retirements in

the same year can’t go below zero.

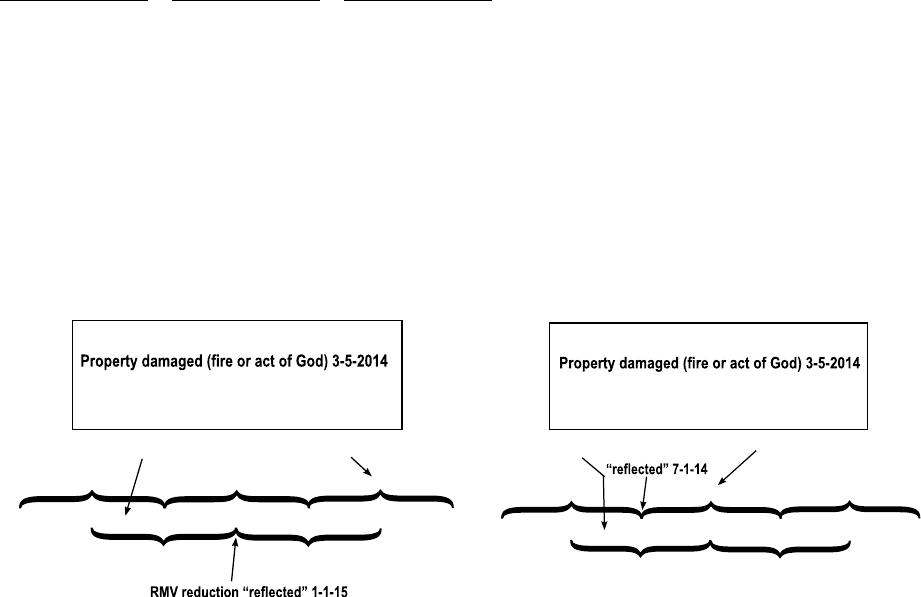

For buildings, if MAV is adjusted as a result of a fire or act of God, or demolition or removal of the

building, it isn’t considered a retirement. For more information on both of these situations, see the

corresponding rules: OAR 150-308-0120 Reduction of Maximum Assessed Value (MAV) When a

Building is Demolished or Removed, OAR 150-308-0110 Reduction of Maximum Assessed Value (MAV)

for Property Destroyed or Damaged by Fire or Act of God.

Integral property

ORS 308.153(3) provides that property that has been continuously in existence since a prior tax year

but wasn’t included in an assessment for any prior tax year shall be considered new property, or new

improvements to property. This provision applies where the property that hasn’t been assessed is an

integral part of the land or improvements on the assessment roll, either on the assessment date or the date

of a site inspection by the assessor for appraisal purposes for any prior tax year. The Oregon Tax Court

has ruled that such property doesn’t constitute omitted property under ORS 308.156 and 311.216.

MAV adjustment

The proper method is to determine the current RMV of the property as it now exists and subtract what the

current RMV of the property would have been as if no new property had been added during the prior year.

This ensures any changes in value over time are eliminated from the calculation.

So, for any new property exception, Exception RMV equals:

RMV of the property as of the current assessment date minus the RMV the property would have

had if the exception didn’t occur as of the current assessment date.

To calculate the adjustment to MAV, the CPR for the corresponding property class is multiplied by the

Exception RMV of only the affected/new property or new improvements. The formula would be:

Exception RMV of new property x CPR = Exception MAV adjustment.

Then we just add together the base MAV and the Exception MAV adjustment to arrive at the new MAV:

Exception MAV adjustment + Base MAV = New MAV (Only one MAV per account).

150-303-438 (Rev. 05-18)

4-3

If the new property consists of stand-alone new construction, such as a new building, its RMV is simply

the RMV of the building. However if the new improvement is a remodel or restoration, the determination

of RMV can be trickier. We will cover some examples so the mathematical calculations are clear.

A common error is to calculate RMV of new improvements as the difference between the RMV of the

property for the current year and the RMV of the property on the tax roll for the prior year. However,

that calculation also includes changes to the value of the existing property due to market fluctuations.

The proper method is to determine the RMV of the property for the year in question and subtract what

the RMV of the property would have been as of that same date if no new property had been added, or

other exception event had occurred, during the prior year. This ensures any changes in value over time

are eliminated from the calculation.

So, for any exception, RMV of the exception equals:

RMV of the property as of the current assessment date minus RMV the property would have had

if the exception didn’t occur.

Calculating the MAV for a new improvement

There are 6 steps in determining the new MAV for a property on which new improvements have been

added. It’s important to note that there is only one MAV per account.

Step 1: Establish base MAV: Always start with the property as if no changes had occurred. Apply the 103

percent test from section 2. This results in the Base MAV.

Step 2: Determine the unaffected RMV: Determine what the RMV of the property would be if property

hadn’t changed (unaffected).

Step 3: Determine the new RMV of the property with the changes (affected portion and possibly unaffected

portion).

Step 4: Calculate the amount of exception RMV:

New RMV—Unaffected RMV = Exception RMV

Step 5: Calculate the exception MAV: this we be the amount we are authorized to add to MAV:

Exception RMV x CPR = Exception MAV

Step 6: Calculate the new MAV:

Exception MAV + Base MAV = New MAV (Only one MAV per account)

New improvement example #1:

During 2015, the homeowner adds a covered porch to the home. RMV for the home increases to $280,000 for

the 2016–17 tax year (due partly to market appreciation). If the homeowner hadn’t added the covered porch,

the RMV for the 2016–17 tax year would have been $268,000.

The home had the following values for the 2015–16 tax year:

RMV = $ 250,000

MAV = $ 180,000

AV = $ 180,000

The CPR for residential 1xx property will be 0.790 for the 2016–17 tax year in that county.

150-303-438 (Rev. 05-18)

4-4

Step 1: Establish base MAV: Start with the property as if no changes had occurred. Apply the 103 percent

test from section 2. This results in the Base MAV.

AV—$180,000 x 1.03 = $185,400 or MAV-$180,000. Which one is greater? = AV x 1.03.

Base MAV = $185,400

Step 2: Determine the unaffected RMV: Determine what the RMV of the property would be if property

hadn’t changed (unaffected).

Unaffected RMV for 2016–17 = $268,000

Step 3: Determine the new RMV of the property with the changes:

RMV for 2016–17 = $280,000

Step 4: Calculate the amount of exception RMV:

New RMV—Unaffected RMV = Exception RMV

$280,000 - $268,000 = $12,000 exception RMV

Step 5: Calculate the exception MAV: this is the amount we are authorized to add to MAV:

Exception RMV x CPR = Exception MAV

$12,000 x 0.790 = $9,480 exception MAV

Step 6: Calculate the new MAV:

Exception MAV + Base MAV = New MAV (Only one MAV per account)

$9,480 + $185,400 = $194,880

150-303-438 (Rev. 05-18)

4-5

New house improvement example #2:

A three bedroom, two bath home was built on a lot. The project was started and was 100% completed in

2016.

The lot had the following values for the 2015–16 tax year:

RMV LAND = $ 87,000

RMV OSD = $ 0

RMV IMP = $ 0

MAV = $ 75,000

AV = $ 75,000

The CPR for residential 1XX property will be 0.790 for the 2016–17 tax year in that county.

150-303-438 (Rev. 05-18)

5-1

New property or new improvements to property don’t include general ongoing maintenance and repair

(GOMAR). GOMAR preserves the condition of the existing improvements. It allows improvements to

achieve a useful life that is typical for the type and quality of the original improvements. Regardless of

the cost, the value of GOMAR may not be included as additions for the calculation of MAV.

GOMAR allows for the replacement of worn out components. A change to the modern equivalent of

original materials for the same class of construction is allowed, such as the replacement of old aluminum

frame windows with new vinyl windows that would be used in the same class of building today.

GOMAR doesn’t include new structures or additions, or any significant changes in the design of

property. It doesn’t include the replacement of original materials with substitutes of a higher quality class

or that increase the useful life of the property beyond what would otherwise be typical. For example,

if the aluminum frame windows discussed above were replaced by triple pane, hurricane-rated vinyl

windows expected only in a higher class of construction, the difference in value between the upgraded

windows and windows that are equivalent to the original material should be considered an exception.

For income producing properties, GOMAR must be part of a regularly scheduled maintenance program.

This can include improvements that occur either on a frequent basis, or for which funds are set-aside in

anticipation of infrequent maintenance activities.

The determination of whether an improvement constitutes GOMAR or an exception is the most

subjective issue relating to MAV. While the examples below are intended to provide some guidance

regarding what is and what isn’t GOMAR, factors in each specific situation must be considered. You must

determine whether the activity maintains the property as it existed when first constructed, or improves

the property beyond what was originally constructed.

For some guidance from the Oregon Tax Court, refer to the decisions in Hoxie v. Department of Revenue, 15

OTR 322 (2001) and Magno v. Department of Revenue, 19 OTR 51 (2006), in the appendix.

Examples which typically qualify as GOMAR include:

• Replacing a worn out composition roof cover on a house with a new one of like quality and material.

• Resurfacing or hot-mopping a 40,000 square foot built-up roof on an industrial structure.

• Replacing defective siding with a non-defective equivalent.

• Replacing a few broken deck boards on a marine pier to maintain normal and constant use.

• Replacing a worn bearing in a board edger (equipment) at the sawmill.

• Replacing worn out kitchen floor covering, appliances, and counter tops in a house.

• Annually repainting the interiors, re-carpeting, and replacing countertops and lavatories in 20 percent

of the rooms of a four-star hospitality property (hotel).

Examples which typically don’t qualify as GOMAR include:

• Replacing a deteriorated composition roof cover with a roof of superior materials, such as tile or heavy shakes.

• Adding a second floor to a house (adds additional square footage).

• Expanding the floor area of a processing plant.

• Replacing all or most decking boards on a pier (constitutes reconstruction).

• Replacing a board edger at the sawmill (the complete replacement of an item isn’t maintenance).

• Replacing kitchen floor covering, appliances, counter tops, and cabinets in a 10-year-old house. (This

wouldn’t be typical for most homes of this age. There may or may not be an increase in RMV. If there

is, then there will be a corresponding increase in MAV. Usually replacing 10-year-old kitchen cabinets

is more than just maintaining the property.).

• Repainting the interiors, re-carpeting, and replacing countertops and lavatories in all of the units of a

motel. Since it impacts a substantial portion of the property, it would qualify as rehabilitation.

Section 5—General ongoing

maintenance and repair

150-303-438 (Rev. 05-18)

6-1

ORS 308.149 Definitions for ORS 308.149 to 308.166

(5) “Minor construction” means additions of real property improvements, the real market value of

which doesn’t exceed $10,000 in any assessment year or $25,000 for cumulative additions made over five

assessment years.

OAR 150-308-0160 Minor Construction

(1) Definition: “Minor construction” is an improvement to real property that results in an addition

to real market value (RMV), but doesn’t qualify as an addition to maximum assessed value (MAV) due

to a value threshold. The value threshold is an RMV of over $10,000 in any one assessment year, or over

$25,000 for all cumulative additions made over five assessment years.

(2) Minor construction doesn’t include general ongoing maintenance and repairs.

(3) When testing the over $25,000 threshold, use the cumulative RMV of all minor and major

construction over a period not to exceed five consecutive assessment years.

(a) Minor and major construction values are not market trended.

(b) Values for retirements are not considered in the threshold test.

(c) Values for minor construction items that are removed or destroyed prior to being an adjustment to

MAV are subtracted from the minor construction cumulative RMV.

(4) Once the over $25,000 threshold is met, use the following steps to calculate the MAV adjustment:

(a) Use minor construction values that are not market trended.

(b) Make adjustments for any retirements from the prior assessment year. The net value of additions

and retirements may not go below zero.

(c) Apply the changed property ratio (CPR) from the year the cumulative RMV becomes an addition

to M AV.

(d) Reset the cumulative RMV for minor construction to zero and restart the 5-year period. The

following examples demonstrate the over $25,000 threshold. RMVs in the following examples are not

market trended and/or depreciated.

Minor construction means additions of real property improvements where RMV doesn’t exceed

$10,000 in one year, and the total accumulated RMV of the improvements doesn’t exceed $25,000 in five

consecutive years.

Minor construction results in an increase in RMV, but doesn’t qualify as an addition to MAV until one of

the valuation thresholds has been surpassed. In the year that minor construction is added to RMV, the

properly trended RMV of the minor construction for that year, is added to the minor construction pool,

which is tracked for five cumulative and consecutive years. Once in the pool, these values aren’t market

trended again.

Values for minor construction items that are removed or destroyed prior to a MAV adjustment are

subtracted from the minor construction pool.

In addition, the RMV of any retirements aren’t considered when determining if either threshold has been

met.

If the RMV of new improvements exceeds the $10,000 threshold in a single year, this would qualify for an

adjustment to MAV as a major construction improvement plus the RMV of those improvements are still

added to the minor construction pool.

Section 6—Minor construction

150-303-438 (Rev. 05-18)

6-2

Minor construction doesn’t include GOMAR.

When the $25,000 threshold is exceeded within a consecutive five-year period, the RMV in the pool

minus the RMV of any new improvements that already resulted in an adjustment to MAV (because

they exceeded the $10,000 threshold) becomes the RMV of the exception. In addition, adjustments for any

retirements for the year that the $25,000 threshold is exceeded must be made prior to calculating the MAV

adjustment. The CPR for the year the cumulative RMV exceeds the $25,000 threshold is used to calculate

the MAV adjustment.

Whenever the $25,000 threshold is exceeded and an adjustment is made to MAV, the cumulative RMV in

the pool is reset to zero, and the five-year period is restarted.

OAR 150-308-0160 provides the following examples to illustrate how RMV is tracked in the minor

construction pool, and how adjustments to MAV are made when the thresholds are exceeded.

150-303-438 (Rev. 05-18)

6-3

Example 1—Over $25,000 not met

Year

New improvement

value

Cumulative

total Comment

1 $8,000 $8,000 Doesn’t qualify as an adjustment to MAV.

Individual year RMV is under $10,001 and

cumulative RMV is under $25,001.

2 None $8,000 No change.

3 $7,000 $15,000 Doesn’t qualify as an adjustment to MAV.

Individual year RMV is under $10,001 and

cumulative RMV is under $25,001.

4 None $15,000 No change.

5 $5,000 $20,000 Doesn’t qualify as an adjustment to MAV.

Individual year RMV is under $10,001 and

cumulative RMV is under $25,001.

RMVs in the following examples aren’t market trended and/or depreciated.

Example 2—Over $25,000 not met, prior years drop off

Year

New improvement

value

Cumulative

total Comment

1 $8,000 $8,000 Doesn’t qualify as an adjustment to MAV.

Individual year RMV is under $10,001 and

cumulative RMV is under $25,001.

2 None $8,000 No change.

3 $5,000 $13,000 Doesn’t qualify as an adjustment to MAV.

Individual year RMV is under $10,001 and

cumulative RMV is under $25,001.

4 None $13,000 No change.

5 $7,000 $20,000 Doesn’t qualify as an adjustment to MAV.

Individual year RMV is under $10,001 and

cumulative RMV is under $25,001.

6 $11,000 $23,000 Year 6 qualies individually as is over $10,000.

Prior years still don’t qualify, as 5 year cumulative

total is under $25,001. (Remember, year 1 has

dropped off the 5 year cumulation.

$11,000 x CPR = adjustment to MAV.)

150-303-438 (Rev. 05-18)

6-4

Example 3—Cumulative RMV reset

Year

New improvement

value

Cumulative

total Comment

1 $8,500 $8,500 Doesn’t qualify as an adjustment to MAV.

Individual year RMV is under $10,001 and

cumulative RMV is under $25,001.

2 $100,000 $108,500 Year 2 qualies individually as RMV is over

$10,000. Year 1 qualies as 5 year cumulative total

is over $25,000. $108,500 x CPR = adjustment to

MAV. Cumulative total and ve year period reset

for the next year.

1 $9,500 $9,500 Cumulative total and ve year period have

reset. Doesn’t qualify as an adjustment to MAV.

Individual year RMV is under $10,001 and

cumulative RMV is under $25,001.

Example 4—Cumulative RMV reset

Year

New improvement

value

Cumulative

total Comment

1 $8,000 $8,000 Doesn’t qualify as an adjustment to MAV.

Individual year RMV is under $10,001 and

cumulative RMV is under $25,001.

2 $5,000 $13,000 Doesn’t qualify as an adjustment to MAV.

Individual year RMV is under $10,001 and

cumulative RMV is under $25,001.

3 $15,000 $28,000 Year 3 qualies individually as RMV is over

$10,000. Years 1 and 2 qualify as 5 year

cumulative total is over $25,000. $28,000 x CPR =

adjustment to MAV. Cumulative total and ve year

period reset for the next year.

1 None $0 Cumulative total and ve year period have reset.

150-303-438 (Rev. 05-18)

6-5

Example 5—Individual year and cumulative year adjustments

Year

New improvement

value

Cumulative

total Comment

1 $5,000 $5,000 Doesn’t qualify as an adjustment to MAV.

Individual year RMV is under $10,001 and

cumulative RMV is under $25,001.

2 None $5,000 No change.

3 $15,000 $20,000 Year 3 qualies individually as RMV is over

$10,000. Year 1 doesn’t qualify as cumulative RMV

is under $25,001. $15,000 x CPR = adjustment to

M AV.

4 $7,000 $27,000 Years 4 and 1 qualify as cumulative RMV is over

$25,000. $12,000 x CPR = adjustment to MAV.

Cumulative total and ve year period reset for the

next year.

1 None $0 Cumulative total and ve year period have reset.

Example 6—Removal of destroyed minor construction

Year

New improvement

value

Cumulative

total Comment

1 $8,000 $8,000 Doesn’t qualify as an adjustment to MAV.

Individual year RMV is under $10,001 and

cumulative RMV is under $25,001.

2 $5,000 $13,000 Doesn’t qualify as an adjustment to MAV.

Individual year RMV is under $10,001 and

cumulative RMV is under $25,001.

3 -$8,000 $5,000 Improvement added in year 1 is destroyed and is

removed from the cumulative RMV pool.

150-303-438 (Rev. 05-18)

7-1

What is zoning and why is it important? Zoning is a tool of urban planning that controls land uses in a

city. Land uses are divided into residential, commercial and industrial areas, now referred to as zones or

zoning districts in cities.

Why do we have zoning? Zoning laws are government restrictions on how a particular piece of land can

be used or developed and is established by a governmental body that regulates zoning.

What does zoning do? Besides restricting the uses that can be made of land and buildings, zoning laws

also may regulate the dimensional requirements for lots and for buildings on property located within the

town and the density of development (floor area ratio and/or site coverage). Zoning can protect the value

of property by assuring that incompatible uses will be kept apart; such as building an industrial plant in a

residential neighborhood. Zoning also provides for more orderly development.

What happens when zoning changes? The governmental body that regulates zoning has the responsibility

of changing zoning and the assessor’s office may or may not receive information on changes from these

governmental bodies. It is still the responsibility of the assessor’s office when performing appraisals to

verify if zoning has changed when questions arise. This can impact the RMV, since RMV is based upon a

property’s highest and best use.

OAR 150-308-0240(1)(e) “Highest and best use” means the reasonably probable use of vacant land or an

improved property that is legally permissible, physically possible, financially feasible, and maximally

productive, which results in the highest real market value.

It is not enough for property to be rezoned to calculate an exception to the 3 percent growth limitation for

MAV. ORS 308.146(3)(c) indicates two requirements must be met to qualify:

1. Property is rezoned, and

2. Property must also be used consistently with the rezoning to qualify for MAV exception value to be

added to the roll.

In the fall of 2016, OAR 150-308-0200, Rezoned property—Calculating maximum assessed value (MAV),

was rewritten to provide more in-depth guidance. Included in the new descriptions are:

• Definitions of necessary terminology have been added at the beginning of the rule and provide signifi-

cant clarification;

• “Primary use” and “Accessory use” are clearly defined;

• Rezoning is described as three distinct, qualifying changes in zone designations or allowed property

use made by the governmental body.

OAR 150-308-0200 (In part) Rezoned property—Calculating maximum assessed value

(MAV)

(1) For the purposes of determining MAV under ORS 308.142 to 308.166 and this rule, the following

definitions apply:

(a) “Primary use” means an activity or combination of activities of chief importance on the site and is

one of the main purposes for which the land or structures are intended, designed, or ordinarily used. A

site may have more than one primary use, such as mixed use buildings with commercial use on the ground

floor and residential use on upper floors.

(b) “Accessory use” means a use or activity that is incidental and subordinate to the primary use of the

property. A use designated as “accessory “or “auxiliary” by an applicable zoning code is presumed to be

accessory unless that designation is clearly inconsistent with the ordinary legal meaning of “accessory,” as

Section 7—Rezoned and used

consistently with rezoning

150-303-438 (Rev. 05-18)

7-2

determined by relevant criteria such as the relative size of the area used and the impact of the use on the

surrounding neighborhood. Accessory uses may include, but are not limited to:

(A) In residential zones, recreational activities, hobbies, home businesses, or pet raising;

(B) In commercial office zones, cafeterias, health facilities, or other amenities primarily for employees;

(C) In commercial retail zones, offices or storage of goods;

(D) In industrial zones, storage, rail spurs, lead lines, or docks;

(E) Parking in any zone, unless commercial parking is designated or allowed as a primary use, such as

for parking structures; and

(F) Accessory structures such as accessory dwelling units limited in size, garages, car ports, decks,

fences, and storage sheds.

(c) “Type of use” means one of the uses defined in OAR 150-308-0310.

(d) “Floor area ratio” means the relationship of the total allowed area of above ground floors of a

building to the total area of the parcel of land on which it is sited.

(e) “Site coverage ratio” means the relationship of the total area covered by the footprint of a building

to the total area of the parcel of land on which it is sited.

(f) “Rezoned” means on or after July 1, 1995, the governmental body that regulates zoning:

(A) Made any change in the zone designation, including but not limited to an overlay, plan district, or

floating zone designation, of the property;

(B) Made a change in one or more of the permitted primary types of use of the property; or

(C) Made a change in:

(i) The number of dwelling units, other than accessory dwelling units, allowed per acre, or other legal

limitation on the number of dwelling units, other than accessory dwelling units, in a given area;

(ii) The allowed floor area ratio; or

(iii) The allowed site coverage ratio.

Additional questions to qualify for rezoned:

In addition to providing clearer definitions, supplementary questions need to be investigated to determine

if a property actually qualifies as rezoned. What appeared to be “a simple two-part qualification”, as

previously indicated in statute, gives rise to these questions:

1. What are the definitions of “Primary” and “Accessory” use?

2. Can new Accessory uses qualify for rezoned?

3. What is “Type of Use”? Can it change? Does it always trigger exception?

4. What does floor area ratio mean and why is this important?

5. What does site coverage ratio mean and why is this important?

6. What is “Rezoned” and why is it date specific?

7. So when has property been rezoned?

8. What does it mean to be used consistently with the rezoning?

9. When a property qualifies for rezone and consistent use Exception…Now what?

a. What does “affected” and “not affected” portions mean?

b. What are the calculations for determining exception MAV?

150-303-438 (Rev. 05-18)

7-3

A “Rezone matrix” is included at the back of this chapter. This one page chart is exclusive to rezoning

questions and their relationship to the expanded guidance in OAR 150-308-0200. Following the Matrix

sequentially should help in determining if rezoning has indeed occurred. Let’s take a look at each question

and answer:

Primary versus accessory uses

1. What are the definitions of “primary” and “accessory” uses?

A primary use is an activity or combination of activities of chief importance on the site and is one of the

main purposes for which the land or structures are intended, designed, or ordinarily used. A site may

have more than one primary use, such as mixed use buildings with commercial use on the ground floor

and residential use on upper floors.

An accessory use is a use or activity that is a subordinate part of a primary use of the property and is

clearly incidental to the primary use under the zoning. A use designated as “accessory “or “auxiliary”

by an applicable zoning code is presumed to be accessory unless that designation is clearly inconsistent

with the ordinary legal meaning of “accessory,” as determined by relevant criteria such as the relative

size of the area used and the impact of the use on the surrounding neighborhood. Accessory uses

include, but are not limited to:

• In residential zones—recreational activities, hobbies, home businesses, or pet raising.

• In commercial office zones—cafeterias, health facilities, or other amenities primarily for employees.

• In commercial retail zones—offices or storage of goods.

• In industrial zones—storage, rail spurs, lead lines, or docks.

• Parking in any zone, unless commercial parking is designated or allowed as a primary use, such as for

parking structures.

• Accessory structures such as accessory dwelling units limited in size, garages, carports, decks, fences,

and storage sheds.

Any change in allowed accessory uses doesn’t constitute “rezoning” for purposes of calculating MAV.

This includes accessory dwelling units, which are specifically excluded from the definition as noted

above.

2. Can “accessory uses qualify for rezoned?

Any change in allowed “accessory uses” won’t constitute “rezoning” for purposes of calculating

Exception MAV. This includes accessory dwelling units (ADU), which are specifically excluded from the

definition as noted above.

Type of use

3. What is type of use? Can it change? Does it always trigger exception MAV?

The definition of “rezoned” includes changes in the allowed primary type of use, which are identified

by the first digit in the property classification system described in section 2. Therefore, changes in the

allowed uses that fall within the same type of use don’t constitute rezoning. For example, if a zoning

ordinance is amended to allow a beauty school in a commercial office zone, property hasn’t been rezoned

as long as the actual zone designation didn’t change. This is because both commercial office use and the

new use of a beauty school are both within the same type of use, which is commercial 2xx.

150-303-438 (Rev. 05-18)

7-4

Floor area ratio (FAR) and Site coverage ratios

4. What is floor area ratio (FAR)?

5. What is site coverage ratio?

“Rezoned” also includes a change to either of these two ratios. They are defined as:

Floor area ratio (FAR): The relationship of the total allowed area of above ground floors of a building to

the total area of the parcel of land on which it’s sited.

Site coverage ratio: The relationship of the total area covered by the footprint of a building to the total

area of the parcel of land on which it’s sited.

Increasing either or both of these ratios also can have a significant impact on the value of property.

A higher ratio allows for more intensive development of the land and changes the nature of the

neighborhood.

Rezoned before July 1, 1995:

6. Why is “rezoned” date specific?

For the purposes of calculating MAV, only property that is rezoned after July 1, 1995, (which is the

assessment date for the RMV that originally established MAV under Measure 50), is considered.

Why? If a property was rezoned before July 1, 1995, the RMV of the property would have already

reflected an adjustment for those considerations and, when MAV was established, those changes would

have already be incorporated in the real market value.

7. So when has property been rezoned?

Jurisdictions can significantly alter the allowed uses of property without actually changing the zoning

designation. As a result, this may seem like a long and complicated definition of “rezoned.” However

it really comes down to asking three questions corresponding to the three paragraphs in OAR 150-308-

0200(1)(f):

1. Has the governing body that regulates zoning, since July 1, 1995, changed the zone designation of the

property? OAR 150-308-0200(1)(f)(A).

2. Has the governing body that regulates zoning, since July 1, 1995, made a change to the zoning ordinances

to allow a new type of use, other than an accessory use, of the property? OAR 150-308-0200(1)(f)(B).

3. Has the governing body that regulates zoning, since July 1, 1995, made a change to the number of

allowed dwelling units (other than accessory dwelling units) per acre or other given area, or changed

the allowed floor area or site coverage ratios? OAR 150-308-0200(1)(f)(C).

If the answer to any one of these questions is yes, then the property has been rezoned. However, the MAV

isn’t affected unless the property is also used consistently with the rezoning.

8. What does it mean to be used consistently with the rezoning?

According to OAR 150-308-0310, all properties have been assigned a property classification which

includes a zone designation as the second digit described in section 2. It is when changes to zoning or

“re-zoning” occurs and the second test, consistent use, align that MAV exception value is required to be

added to the roll.

Property is “used consistently with the rezoning” when it’s put to a newly allowed use. This doesn’t

include situations where the use of the property was an allowed use both before and after the rezoning.

For example, if a vacant parcel is rezoned from single- to multi-family housing, but single-family

dwellings are still allowed under the new zone, when a single-family dwelling is constructed the

property hasn’t been used consistently with the rezoning. Be aware that this example would still qualify

for MAV exception; just not under rezoned. See Section 6—“New Improvements” for how this example

would qualify.

150-303-438 (Rev. 05-18)

7-5

Both tests, rezoned and use consistent with the rezoning, must be met before MAV can be recalculated

as an exception. However it isn’t necessary for the rezoning to occur first. For example, a house in a

residential zone may be used as a commercial office. When the zoning is later changed from residential

to commercial, the property is now used consistently with the rezoning. The commercial use was a

nonconforming use under the prior zoning, and is a now a newly permitted use. Therefore this property

is now used consistently with the zoning and qualifies for exception MAV.

Property qualies as rezoned

When a property or portion of property qualifies as rezoned, now what? Determine if there are “affected”

and “unaffected” portions as defined by administrative rule.

Affected property

OAR 150-308-0180 defines “affected property” as property that “is subject to one or more of the

following events: partitioned or subdivided; added to the account as omitted property; rezoned and used

consistent with the rezoning; disqualified from a special assessment, exemption, or partial exemption.”

When property is rezoned and used consistently with the rezoning, the affected property includes all

improvements that are constructed for or converted to the newly allowed use as described in:

OAR 150-308-0200

(2) For the purposes of calculating maximum assessed value when a property is rezoned and used

consistently with the rezoning, the portion of the property that is “affected” includes:

(a) Improvements that are converted to the newly allowed use; and

(b) All land that supports a newly allowed use, including, but not limited to:

(A) Land under newly constructed or converted improvements put to the newly allowed use;

(B) Ingress and egress related to the newly allowed use;

(C) Access to utilities;

(D) Landscaping;

(E) Yard areas; and

(F) Parking.

In some cases, only a portion of a property tax account may lie within an area (such as a taxing district)

that has been rezoned or only a portion of the property may have been used in a manner consistent with

a zone change. In this case, you would adjust the MAV of only the affected property for the exception.

As discussed in earlier sections, each property tax account has only one MAV. When one of the allowable

exceptions qualifies, MAV must be allocated between the affected and unaffected portions of the property as

the unaffected portion of MAV doesn’t have an exception event.

The allocation of MAV is proportionate to the allocation of RMV between the affected and unaffected portions

of the property.

To begin, an example has been provided for an entire affected property and a second example of the more

complex partial rezone containing “affected” and “unaffected” property follows.

150-303-438 (Rev. 05-18)

7-6

Example #1: Entire property is rezoned and used consistently:

Property was rezoned from residential to commercial two years ago. Last year, the entire property

was developed under one of the new permitted uses:

A one and a half acre lot has been developed into a bicycle sales and service shop. The shop,

including all parking and landscaping, occupies half of an acre and the rest of the land was

developed as an off road bicycle skills course. It’s determined that the entire property qualifies as

rezoned:

Because the rezone affects the entire property, multiply the current year RMV of the entire property

by the CPR. This becomes the new MAV for the entire property.

Current year RMV of the affected portion = $750,000.

Current year CPR for this property type = 0.800.

$750,000 x 0.800 = $600,000 (current year MAV for the affected portion).

New: Current year values:

RMV = $750,000

MAV = $600,000

AV = $600,000

Summary steps:

The entire property is rezoned:

1. Calculate the current year RMV (both land and improvements).

2. Multiply current year RMV by CPR for property class to determine new MAV and AV.

3. Allocate the RMV to the land and improvement portion of the account.

150-303-438 (Rev. 05-18)

7-7

Example #2: Complex: A portion of a property is rezoned and used consistently:

Property was rezoned from residential to commercial in 2015. In 2016–17, a portion of a one and a half

acre lot has been developed into a bicycle sales and service shop. The shop, including all parking and

landscaping, occupies half of an acre. The rest of the land (one acre) remains undeveloped.

In this more complex example, the rezoning and consistent use affects just a portion of the property.

This means some of the MAV remains unaffected and won’t be changed. This requires 6 steps:

For a partial rezoning, we begin with valuing the property as if no changes had occurred:

Prior year 2015–16 values:

RMV = $150,000

MAV = $101,000

AV = $101,000

Current year 2016–17 RMV of affected portion = $700,000 ($20,000 OSD’s and $680,000 shop).

Current year 2016–17 CPR for this property type = 0.800.

Step 1. Establish base MAV. Start with the property as if no changes had occurred (Apply the 103

percent test).

Multiply the prior year AV by 1.03. Compare the result to the prior year’s MAV to determine which

one is greater. This becomes the current year Base MAV as if the account hadn’t changed:

AV $101,000 x 1.03 = $104,030 or $101,000. Which one is greater? = AV x 1.03.

$104,030 = Current year MAV of the unchanged account.

Step 2. Calculate the RMV that remains unaffected using the prior year’s total RMV: (to establish the

value of the “unaffected” portion of RMV).

For this example, we determined that each 0.50 of an acre = $50,000.

Unaffected = 1 acre or 0.50/acre + 0.50/acre.

Result: There is one acre that is unaffected: $50,000 + $50,000 = $100,000 (Prior year RMV of

unaffected portion).

Step 3. Calculate the RMV ratio (to establish the percentage of the “unaffected” portion of RMV).

Divide the prior year RMV of unaffected portion by the prior year’s total RMV for the whole account.

This produces the percentage of the account that is unaffected by the change to the property. The

formula is:

Prior year RMV

of unaffected portion

= Percent of account unaffected

Total prior year RMV

$100,000 Prior year RMV of unaffected portion (one acre).

$150,000 Total prior year RMV of one and one half acres.

Formula applied:

$100,000

= 0.666 or 66.6% (percentage of the account that is unaffected)

$150,000

RMV Ratio = 0.666

Step 4. Calculate the current year MAV for the unaffected portion.

Multiply the base MAV of the unchanged account (from Step 1) by the RMV ratio (Step 3).

This is the current year MAV for the unaffected portion.

$104,030 x 0.666 = $69,283 (current year MAV for the unaffected portion).

150-303-438 (Rev. 05-18)

7-8

Step 5. Calculate the MAV for the affected portion.

Multiply the current RMV of the affected portion by the CPR. This is the MAV for the affected portion.

$700,000 (New RMV) - $100,000 (Unaffected RMV) = $600,000 x 0.800 = $480,000 (current year MAV for

the affected portion).