BY ORDER OF THE

SECRETARY OF THE AIR FORCE

AIR FORCE INSTRUCTION 65-501

29 OCTOBER 2018

Financial Management

ECONOMIC ANALYSIS

COMPLIANCE WITH THIS PUBLICATION IS MANDATORY

ACCESSIBILITY: Publications and forms are available for downloading or ordering on the

e-Publishing website at www.e-Publishing.af.mil

RELEASABILITY: There are no releasability restrictions on this publication.

OPR: SAF/FMCE

Supersedes: AFI65-501, 29 August 2011

AFI65-509, 19 September 2011

Certified by: SAF/FMC

(Ms. Pamela C. Schwenke)

Pages: 22

This Instruction implements Air Force Policy Directive 65-5, Cost and Economics. It gives

specific instructions on economic analysis for Air Force management and financial decisions. This

publication applies to individuals and organizations at all levels of the Regular Air Force, Air Force

Reserve and Air National Guard (ANG), who make resource decisions. Ensure all records created

as a result of processes prescribed in this publication are maintained in accordance with Air Force

Manual 33-363, Management of Records, and disposed of in accordance with the Air Force

Records Disposition Schedule located in the Air Force Records Information Management System.

Refer recommended changes and questions about this publication to the Office of Primary

Responsibility (OPR) using AF Form 847, Recommendation for Change of Publication; route AF

Form 847s from the field through the appropriate functional’s chain of command. This publication

may be supplemented at any level, but all supplements must be routed to the OPR of this

publication for coordination prior to certification and approval. The authorities to waive wing/unit

level requirements in this publication are identified with a Tier (“T-0, T-1, T-2, T-3”) number

following the compliance statement. See AFI 33-360, Publications and Forms Management, for a

description of the authorities associated with the Tier numbers. Submit requests for waivers

through the chain of command to the appropriate Tier waiver approval authority, or alternately, to

the requestor’s commander for non-tiered compliance items.

2 AFI65-501 29 OCTOBER 2018

SUMMARY OF CHANGES

This document has been substantially revised and needs to be completely reviewed. Major changes

include: Air Force Instructions (AFIs) 65-501 and 65-509 have been combined to form one

Instruction; a clarification was added that economic analysis is both an analytical approach to

decision-making and one of many products resulting from the analytical approach; a clarification

was added that all comparative analysis products (e.g., Cost Benefit Analysis, Analysis of

Alternatives, Business Case Analysis, etc.) fit under the umbrella of the economic analysis

approach and are subject to this Instruction (consistent with Department of Defense Instruction

(DoDI) 7041.03). As a result, this Instruction now uses one term, comparative analysis, to refer

to all types of analysis that result from using the economic analysis approach and uses the term

comparative analysis product for the document resulting from a comparative analysis.

AFI65-501 29 OCTOBER 2018 3

Chapter 1

ECONOMIC ANALYSIS.

1.1. Introduction. This Instruction applies when making resource decisions. There are always

more requirements than available resources (e.g., manpower, equipment, fuel, facilities).

Furthermore, typically there are competing alternatives by which an objective (e.g., strong national

defense) can be achieved. As such, a systematic process for making decisions based on costs and

benefits is a valuable tool for government decision-makers.

1.2. Definition. Economic analysis is a systematic approach to the problem of deciding how to

use scarce resources to achieve a given objective. Proper use of the economic analysis approach

yields an impartial comparison of competing alternatives to achieve the objective by weighing the

costs, benefits, and uncertainties (including risks) for each alternative.

1.2.1. Implementing the economic analysis approach results in analyses that are referred to by

a variety of names (e.g., economic analysis, business case analysis, cost benefit analysis,

analysis of alternatives). See Figure 1.1.

1.2.1.1. Consistent with DoDI 7041.03, Economic Analysis for Decision-making, analytic

studies that deal with cost and benefit considerations fit under the definition of “economic

analysis” (even though not specifically titled as such) and must adhere to the policy in this

Instruction. (T-1).

1.2.1.2. For the remainder of this Instruction, all the analyses resulting from implementing

the economic analysis approach will be referred to as “comparative analyses” or simply as

“analyses” unless referring to a specific product whose name has been directed at a higher

level (e.g., Product Support Business Case Analysis, Military Construction Economic

Analysis). The document produced as a result of performing a comparative analysis will

be referred to as the comparative analysis product or document. The conceptual approach

to decision-making and the overall policy, however, will still be referred to as economic

analysis to remain consistent with DoDI 7041.03.

4 AFI65-501 29 OCTOBER 2018

Figure 1.1. Economic Analysis Approach and Comparative Analysis.

1.3. Background. The Department of Defense (DoD) and the Air Force define economic analysis

as the approach to making resource decisions.

1.3.1. Even though the Air Force has a structured framework for performing economic

analysis, the depth to which the framework is implemented may vary, which will be reflected

in analytical products that vary in their level of rigor.

1.3.2. Some factors which may impact the level of rigor at which the economic analysis

approach should be implemented are: the stage a program or project is in its life cycle, the

level of resources consumed in the project, the level of visibility, and the scope/significance of

the objective.

1.3.3. The economic analysis approach can be applied to any type of decision. Economic

analysis may be applied to very narrow decisions such as where to host a system or what type

of flooring to use in a building. Conversely, economic analysis may be applied to large

strategic resource decisions such as the level of investment the Defense Department should

expend on different capabilities (e.g., Special Forces, Airlift, and Aircraft Carriers).

1.3.4. The economic analysis approach does not replace the judgment of the decision maker,

but rather aids that judgment. Using this systematic approach reduces the incidence of serious

omissions or the introduction of bias.

1.3.5. Allocating resources to highly effective uses is critical to the Air Force mission. The

economic analysis approach assists the decision maker in these allocation decisions. When

properly performed and documented, the economic analysis approach provides auditability for

the resource decisions made.

1.4. Roles and Responsibilities

AFI65-501 29 OCTOBER 2018 5

1.4.1. Deputy Assistant Secretary of the Air Force for Cost and Economics (SAF/FMC)

will:

1.4.1.1. Serve as the office of primary responsibility for Air Force economic analysis.

1.4.1.2. Provide Air Force-wide guidance on economic analysis policy and procedures.

1.4.1.3. Approve comparative analysis instructions developed by Secretariat or Air Staff

functional offices and Major Commands.

1.4.1.4. Review comparative analyses for weapon systems that require approval from the

Defense Acquisition Board, the Air Force Review Board, or equivalent body. For

Acquisition Category I programs, Business System Category I programs, and equivalent

Analysis of Alternatives, may advise the Analysis of Alternatives team, assess the

methodology and rigor of the cost estimate, or may perform an independent estimate of

costs of the alternatives.

1.4.1.5. Review comparative analyses requiring Headquarterslevel approval for other

acquisition requirements.

1.4.1.6. As requested, review non-appropriated fund construction and equipment analyses

for projects presented for Air Force Services Board approval and funding.

1.4.1.7. Review all comparative analyses forwarded to the Secretary of the Air Force, the

Chief of Staff of the Air Force, the Under Secretary of the Air Force, or the Vice Chief of

Staff of the Air Force.

1.4.1.8. Review comparative analyses that will be forwarded to organizations outside the

Air Force (e.g., Office of the Secretary of Defense, Congress)

1.4.1.9. Produce comparative analyses as requested by Headquarters Air Force

organizations.

1.4.1.10. Develop, promotes and monitors economic analysis training.

1.4.1.11. Maintain a site on the Air Force Portal that provides current cost factors and other

economic analysis information.

1.4.1.12. Review and approves/disapproves all requests for waivers from comparative

analysis requirements.

1.4.2. Secretariat and Air Staff Functional Offices will:

1.4.2.1. Decide if a comparative analysis is required or advisable before approving new

initiatives, programs or projects. Functional offices may confer with SAF/FMC to

determine if the issue being examined requires a comparative analysis. For Analysis of

Alternatives, notify SAF/FMC of all efforts for Acquisition Category I programs, Business

System Category I programs, Service Category I Programs and equivalent.

1.4.2.2. Serve as initiator and subject matter expert for the development of comparative

analyses initiated at their level involving their functional area.

1.4.2.3. Issue guidance, upon approval from SAF/FMC, for comparative analysis products

in their functional area.

6 AFI65-501 29 OCTOBER 2018

1.4.2.4. Receive comparative analyses from Major Commands, Program Executive

Offices, or Centers. Review the analysis from their functional perspective, and forward

comparative analyses requiring SAF/FMC review.

1.4.2.5. If questions arise from functional or SAF/FMC review, forward these questions

to the Major Command office, Program Executive Office, or Center proposing the project.

Coordinate correspondence between SAF/FMC and the Major Command, Program

Executive Office, or Center.

1.4.2.6. Review and coordinate on, or reject, as appropriate, requests for waivers from

comparative analysis requirements. Forward all waiver requests to SAF/FMCE.

1.4.2.7. For Air Force Military Construction projects submitted in the President’s Budget

that have not processed through AFIMSC (see paragraph 1.4.3.), ensure there exists either

a comparative analysis that has been completed and certified in accordance with AFMAN

65-506, Economic Analysis, or a waiver to a comparative analysis that has been completed

and coordinated in accordance with AFMAN 65-506.

1.4.2.8. NGB/FMA shall ensure that Air National Guard Military Construction projects

submitted in the President’s Budget include either a comparative analysis that has been

completed and certified in accordance with AFMAN 65-506, or a waiver to a comparative

analysis that has been completed and coordinated in accordance with AFMAN 65-506.

1.4.2.9. AF/REC shall ensure that Air Force Reserve Military Construction projects

submitted in the President’s Budget include either a comparative analysis that has been

completed and certified in accordance with AFMAN 65-506, or a waiver to a comparative

analysis that has been completed and coordinated in accordance with AFMAN 65-506.

1.4.3. Air Force Installation and Mission Support Center Resource Management Cost

Division AFIMSC/RMC (formerly the Financial Management Center of Expertise) will:

1.4.3.1. Provide support in completing non-acquisition comparative analyses for Air Force

Major Command and installation Financial Management offices.

1.4.3.2. Function as a resource for comparative analysis on-the-job training, as requested,

to installation and Major Command Financial Management offices and functional offices.

1.4.3.3. Submit requests for Resource Management Cost Division support.

1.4.4. Financial Management Offices at the Major Command Level and Center Level

will:

1.4.4.1. Serve as the office of primary responsibility for the economic analysis program

within the Major Command.

1.4.4.2. Manage the Command's economic analysis program, including, but not limited to,

providing Command guidance to subordinate organizations and liaison with SAF/FMC.

1.4.4.3. Review and certify comparative analysis products and review and coordinate on

requests for waivers in accordance with AFMAN 65-506 (for products produced below the

Major Command Level, the Major Command or Center FM)

AFI65-501 29 OCTOBER 2018 7

1.4.4.3.1. For programs governed by the DoDI 5000 series (i.e., Weapon System

Acquisition), Center financial management organizations will review and certify

comparative analysis products, and review and coordinate on requests for waivers.

1.4.4.3.2. For programs or projects not governed by the DoDI 5000 series (i.e.,

Weapon System Acquisition), Major Command financial management organizations

will review and certify comparative analysis products, and review and coordinate on

requests for waivers.

1.4.4.3.3. AFMC/FMC may perform this review role in lieu of another Major

Command Financial Management office if both parties have agreed to this arrangement

in a memorandum of understanding.

1.4.4.4. For comparative analysis products required by this instruction and originating at

the Major Command and Center-levels, the Financial Management Office will serve as the

office of primary responsibility for the effort. In this case, the Major Command-level or

Center-level Financial Management Office is fulfilling the role as the Financial

Management Office supporting the requirement originator (see paragraph 1.4.8.).

1.4.4.5. At the request of the Major Command Functional Office, perform comparative

analysis in support of Strategic Basing efforts. The support may be provided organically,

or the Major Command Financial Management office may seek assistance through another

organization (e.g., the Installation and Mission Support Center’s Resource Management

Cost Division).

1.4.4.6. Prepare and forward the Annual Economic Analysis Report (see paragraph 1.8).

1.4.5. Functional Offices at Major Command Level and Center Level will:

1.4.5.1. Follow comparative analysis review and certification procedures as defined in

AFMAN 65-506.

1.4.5.2. Review and coordinate on, or reject, as appropriate, requests for waivers from

comparative analysis requirements and forward approved requests to Secretariat or Air

Staff counterparts for routing to SAF/FMCE for approval.

1.4.5.3. Serve as initiator and subject matter expert for the development of comparative

analyses initiated at their level involving their functional area. Functional offices should

confer with their servicing Financial Management Office to ensure the issue being

examined requires a comparative analysis. For comparative analyses not required by this

Instruction, the Functional Office may serve in place of the Financial Management Office

as the office of primary responsibility.

1.4.5.4. When designated lead Major Command in a Strategic Basing effort, coordinate

with their Major Command Financial Management Office to accomplish Military

Construction, facility repair, or other required comparative analyses during the Site

Activation Task Force process.

1.4.6. Headquarters Air Force Installation and Mission Support Center will:

1.4.6.1. Ensure that each facility project likely to be funded in the budget year has an

approved comparative analysis or a waiver to a comparative analysis prior to the

documentation deadline contained within the respective facility project business rules (e.g.,

8 AFI65-501 29 OCTOBER 2018

Military Construction; Unspecified Minor Military Construction; Facilities Sustainment,

Restoration, and Modernization). At a minimum, this must occur before the Air Force

Board decides to include the project in the Air Force’s President’s Budget submission.

1.4.7. Office requiring a comparative analysis. [Typically this is an Installation and Major

Command Functional Offices, Program Executive Office Program Offices or Sustainment

Offices, but can be any organization.]

1.4.7.1. Will determine the need for a comparative analysis. (T-3). The criteria in

paragraph 1.5. and its subparagraphs must be followed in determining when a formalized

analysis is required. (T-1). The need may also arise from an upcoming decision where a

decision-maker would benefit from the analytical rigor provided from using the economic

analysis approach even though the analysis is not required by this Instruction. Major

Command and Installation Functional Offices should confer with their servicing Financial

Management Office or the Installation and Mission Support Center’s Resource

Management Cost Division to ensure the issue being examined requires an Installation-

initiated comparative analysis. For acquisition-related analyses, Program Executive Office

Program Offices and Sustainment Offices should confer with SAF/FMCE. A Headquarters

Air Force office requiring a comparative analysis should confer with SAF/FMCE.

1.4.7.2. As soon as possible after determining a comparative analysis is required, shall

formally request a comparative analysis from the Financial Management office. (T-3).

1.4.7.3. Should provide support to the comparative analysis preparation process, to include

providing the problem definition, alternatives identification, scope of analysis, needed data

and evaluating the reasonableness of estimated costs and benefits.

1.4.7.4. Should serve as initiator and subject matter expert for the development of

comparative analyses involving their functional area. For comparative analyses not

required by paragraph 1.4.1 of this Instruction, the Functional Office may serve as the

office of primary responsibility in place of the Financial Management Office.

1.4.7.5. Will review the comparative analyses and certify on the Certificate of Satisfactory

Comparative Analysis in accordance with the process in AFMAN 65-506. (T-1). Forward

to the Major Command functional office, as required. (T-1).

1.4.7.6. Will prepare a request for waiver from the comparative analysis requirement when

needed. (T-1).

1.4.7.6.1. Will send written requests for waivers from comparative analysis

requirements to the installation or center level Financial Management Office. (T-1).

Waiver requests must adequately explain and document the reason why a comparative

analysis is not necessary according to paragraph 1.5. (T-1).

1.4.7.6.2. Once the appropriate Financial Management Office coordinates on the

waiver request, the functional office will forward the request for a waiver to their Major

Command functional counterparts (T-1).

1.4.7.7. Shall retain approved comparative analysis products and approved waivers on file

(T-1).

1.4.8. Financial Management Office supporting the requirement originator

AFI65-501 29 OCTOBER 2018 9

1.4.8.1. Will serve as the office of primary responsibility for preparing comparative

analyses required by this Instruction. (T-1). The Force Support Squadron is the office of

primary responsibility for preparing Non-appropriated Funds comparative analyses.

1.4.8.2. The Installation and Mission Support Center’s Resource Management Cost

Division, the Major Command Financial Management Office and SAF/FMCE should be

used as resources for comparative analysis questions and assistance.

1.4.8.3. Should work with the requesting functional office to name those organizations

necessary to formulate alternatives, make assumptions, evaluate benefits, assess

uncertainties (including risks), and provide operational or cost data.

1.4.8.4. The local Senior Financial Manager will sign the Certificate of Satisfactory

Comparative Analysis (see paragraph 1.7) and forwards to the local Functional Office (T-

1).

1.4.8.5. Review and coordinate on, or reject, as appropriate, requests for waivers from a

comparative analysis requirement (T-1).

1.4.8.6. For comparative analysis products required by paragraph 1.5. of this Instruction,

financial management officials should provide an interpretation of the results (which can

include a recommendation) that is consistent with the costs, benefits, and uncertainties

described in the analysis.

1.5. Requirements. The economic analysis approach must be formalized through the creation

of a comparative analysis product and submitted, as required, for higher level review when:

1.5.1. Unless subject to another threshold, deciding whether to commit resources to a new

project, program or initiative where estimated required budget authority over the Future Years

Defense Program exceeds $50,000,000. (T-1). This dollar threshold also applies to a group of

projects which are so closely related that they are logically considered a single entity. (T-1).

1.5.2. Required for Clinger Cohen Act certification. (T-0).

1.5.3. Required for Working Capital Fund Capital Improvement Program projects with

investment costs in excess of $1,000,000 (then-year dollars of the years of the project

investment). (T-0).

1.5.4. Required for the Life Cycle Sustainment Plan Annex of an acquisition program. (T-0).

1.5.5. Required as an Analysis of Alternatives in accordance with DoDIs 5000.02, Operation

of the Defense Acquisition System, 5000.75, Business Systems Requirements and Acquisition,

and 5000.74, Defense Acquisition of Services, and/or other applicable DoD and Air Force

guidance. (T-0).

1.5.6. Proposing real property new construction or repair projects with an estimated

investment cost in excess of $2,000,000 (then-year dollars of the years of the project

investment). (T-0). Note: DOD Financial Management Regulation (FMR) Volume 2b

requires economic analyses for all new construction or renovation projects over $2M. In

accordance with Title 10, USC Section 2811, “renovation” falls under the umbrella term

“repair.” Real property repair projects above the threshold in this paragraph , but below

$20,000,000 (then-year dollars of the years of the project investment), only have to provide a

10 AFI65-501 29 OCTOBER 2018

formalized comparative analysis if estimated repair costs are equal to or exceed 75 percent of

the estimated cost of a feasible new facility that meets the objective. (T-0).

1.5.7. Acquiring temporary facilities to satisfy interim facility requirements. (T-0). A

leasepurchase analysis may be used to satisfy this requirement if there are no feasible non-

relocatable alternatives.

1.5.8. Proposing a housing privatization project or utilities privatization project, regardless of

the amount of the investment cost. (T-0).

1.5.9. Proposing a community partnership project with a value of over $2,000,000 in fiscal

year 2018 constant dollars (either appropriated, non-appropriated, or in-kind). (T-0).

1.5.10. Required by Non-Appropriated Funds policy or guidance, see AFI 65-107,

Nonappropriated Funds Financial Management Oversight Responsibilities, paragraph 1.2.2.5.

(T-0).

1.5.11. Directed by Secretariat or Air Staff, or a commander of field units. (T-1).

1.5.12. Otherwise directed by law or superseding regulation. (T-0).

1.5.13. Proposed changes will push project costs over any of the above dollar threshold

requirements (if no comparative analysis was previously provided). (T-0).

1.5.14. Since requirements can change from legislation, Office of Management and Budget

guidance, and DoD guidance, check the SAF/FMCE site on the Air Force Portal for updated

threshold requirements.

1.6. Economic Analysis Waivers

1.6.1. Waiver Criteria. Unless otherwise prohibited, the requirement to produce a

comparative analysis may be waived if:

1.6.1.1. The Office of the Secretary of Defense or higher authority directs a new or

modified program that specifies how to accomplish program goals.

1.6.1.2. Legislation specifically exempts the project from a comparative analysis, or

specifically directs the method of accomplishment.

1.6.1.2.1. Approval of a specific project in legislation, by itself, is not evidence of

legislative direction. Legislative language may be based on an Air Force submission

in the budget justification books, or other documentation, and may presume a

comparative analysis or waiver was already completed and approved. In this case, the

legislation is insufficient justification for a waiver.

1.6.1.2.2. If the project and method of accomplishment was a Congressional add (e.g.

not requested by the Air Force), then legislative language is sufficient justification for

a waiver.

1.6.1.3. The project corrects problems or violations involving health, safety, fire

protection, pollution, or security which are serious, urgent and hazardous.

1.6.1.4. The costs of formalizing the analysis clearly outweigh the potential informational

benefits accruing to the decision maker. This does not apply to military family housing

projects.

AFI65-501 29 OCTOBER 2018 11

1.6.1.5. There is only one method possible to accomplish the objective. If this criterion is

used, the waiver justification must describe all reasonable alternatives and why they are

not viable. (T-1).

1.6.1.6. A Capital Investment Program project is for environmental, hazardous waste

reduction, or regulatory agency (state, local, or Federal) mandated requirements. The latter

includes action directed by a higher DoD or Component authority that precludes a choice

among alternatives, and DoD instruction or other directive that waives the requirement

(e.g., based on equipment age or condition replacement criteria).

1.6.2. Economic Analysis Waiver Approval Process

1.6.2.1. Waivers to the requirement for a comparative analysis product (per paragraph

1.5.) must be approved by appropriate authorities before proceeding with a project. (T-1).

Waiver requests must adequately explain and document the reason why the analysis is not

necessary or cannot be accomplished. (T-1).

1.6.2.2. With assistance from Financial Management, the functional office will prepare

waiver requests based on the criteria in paragraph 1.5.1., using the format in AFMAN 65-

506. (T-1).

1.6.2.3. All waiver requests must be approved by SAF/FMCE.

1.6.2.4. The activity must coordinate the waiver with the financial management office

responsible for the economic analysis program. (T-1).

1.6.2.5. Headquarters Air Force-level (whether Secretariat or Air Staff) functional office

must also coordinate on waiver requests prior to submission to SAF/FMCE for approval.

1.6.2.6. For Air Force Reserve Command and Air National Guard requests for waiver, Air

Force Reserve Command (AF/REC) and National Guard Bureau Financial Management

Analysis (NGB/FMA), or their delegated Air Staff three letter organization, coordination

is required.

1.7. Certification. All comparative analyses required by paragraph 1.5. of this Instruction must

have a Certificate of Satisfactory Comparative Analysis approved at the appropriate level as

described in AFMAN 65-506. (T-1).

1.7.1. Purpose: The Comparative Analysis Certification Process is the Air Force’s

standardized method of assuring policies and guidance outlined in this Instruction and

AFMAN 65-506 are followed and both functional and financial management reviewers at each

stage of the review coordinate on the assumptions made and techniques used to produce the

analysis results. Certification does not necessarily mean the functional and financial

management reviewers agree with the results of the analysis.

1.7.2. Every Certification shall adhere to the guidance in AFMAN 65-506, to include the

required format, Comparative Analysis Review Guide, and a Comparative Analysis

Certification Checklist. (T-1).

1.7.3. Major Commands and SAF/FMCE must certify a comparative analysis prior to the

analysis being forwarded outside the Air Force (e.g., Congress, DoD, etc.).

1.8. Annual Economic Analysis Report

12 AFI65-501 29 OCTOBER 2018

1.8.1. Each Major Command, Direct Reporting Unit, Field Operating Agency, and similar Air

Force organization will prepare and forward a copy of an annual report concerning their

economic analysis activity to SAF/FMCE by 1 December annually (T-1).

1.8.2. This report will provide information on economic analysis activity in the previous fiscal

year (T-1). For Report Format, see AFMAN 65506.

AFI65-501 29 OCTOBER 2018 13

Chapter 2

SPECIALIZED ANALYSES.

2.1. Introduction

2.1.1. The economic analysis approach is sufficiently flexible to accommodate a number of

different types of decisions. This section introduces some areas with special requirements.

2.2. Preliminary Comparative Analyses

2.2.1. Comparative analysis must be part of program planning when a project is first

considered. (T-3). A preliminary comparative analysis is a first, less detailed effort of

performing a comparative analysis such as an economic analysis, business case analysis or a

cost-benefit analysis, etc.

2.2.2. See AFMAN 65-506 for guidance on performing a Preliminary Comparative Analysis.

2.3. Product Support Business Case Analyses

2.3.1. A Business Case Analysis is a statutory requirement for all major weapon systems based

on Title 10, United States Code (USC) Section 2337. DoDI 5000.02, Operation of the Defense

Acquisition System, states the Business Case Analysis will be included as an annex to the Life

Cycle Sustainment Plan. (T-0).

2.3.2. AFMAN 65-506 provides primary guidance for performing Business Case Analyses.

See Air Force Pamphlet 63-123, Product Support Business Case Analysis, for additional

guidance on performing a Product Support Business Case Analysis.

2.4. Clinger Cohen Act Economic Analyses

2.4.1. 40 USC 1401, Clinger Cohen Act of 1996, requires “criteria related to the calculation

of a Return on Investment” when considering whether to undertake an investment in

information systems. The Return on Investment requirement will be met through either an

Economic Analysis or a Life Cycle Cost Estimate. (T-0).

2.4.2. See AFMAN 65-506 for when to perform an economic analysis for compliance with

the Clinger Cohen Act and for specific guidance.

2.5. Energy Projects

2.5.1. Special instructions apply to energy projects to include those projects under the Energy

Conservation Investment Program.

2.5.2. See AFMAN 65-506 for guidance on performing an economic analysis on energy

projects.

2.6. Lease-Purchase Decisions

2.6.1. After the decision to acquire the services of an asset has been made, the Air Force often

has the option of either purchasing the asset or leasing it. In lease-purchase analyses, benefits

are often essentially the same. In this situation, only a lease-purchase analysis is required (i.e.,

a comparative analysis with two alternatives, lease and purchase).

2.6.2. See AFMAN 65-506 for guidance on performing a lease-purchase analysis.

14 AFI65-501 29 OCTOBER 2018

2.7. Warranty Cost-Benefit Analysis

2.7.1. Some contactors offer a warranty on the performance of their product for an additional

cost. A warranty cost-benefit analysis attempts to determine if the benefits of the warranty are

worth the cost.

2.7.2. See AFMAN 65-506 for guidance on performing warranty cost-benefit analyses.

2.8. Analysis of Alternatives

2.8.1. An Analyses of Alternatives is required to analyze weapons systems according to DoDI

5000.02 and related instructions.

2.8.2. Refer to the USAF Office of Aerospace Studies (OAS) Analysis of Alternatives

Handbook for information on performing an analysis of alternatives.

2.9. Program Evaluation. A Program Evaluation is an economic analysis of on-going operations

to ensure established goals and objectives are being attained in the most cost-effective manner. A

program evaluation compares actual performance with stated program objectives. A program

evaluation must be performed when directed by the program’s leadership or higher authority, or

when prescribed by functional directives. (T3).

2.9.1. Responsibilities Assigned. The official who implements a program, or a higher

authority, should determine the completion date for the program evaluation. The functional

manager, with the assistance of the financial management staff, should establish a plan to

collect and maintain the cost and benefit data necessary for the evaluation.

2.9.2. See AFMAN 65-506 for guidance on performing program evaluations.

2.10. Real Property Construction and Repair

2.10.1. Do a preliminary economic analysis after an installation Facilities Board has

established a requirement for a project, but before the installation Facilities Board has selected

an alternative (T-1). Develop the analysis as the engineers develop the DoD Form 1391. (T-2).

See section 2.2 of this Instruction and AFMAN 65-506 for guidance on preliminary economic

analyses.

2.10.2. For each facility project likely to be funded in the budget year, do a full economic

analysis or a waiver to an economic analysis prior to the documentation deadline contained

within the respective facility project business rules (e.g., Military Construction; Unspecified

Minor Military Construction; Facilities Sustainment, Restoration, and Modernization). (T-1).

2.10.2.1. For Military Construction projects, at a minimum, approval of the economic

analysis or waiver must be complete before the Air Force Board decides to include the

project in the Air Force’s President’s Budget submission. (T-1).

2.10.2.2. For Unspecified Minor Military Construction or repair projects, at a minimum,

approval of the economic analysis or waiver must occur before the project is forwarded to

Headquarters Air Force for approval and notification. (T-1).

2.10.3. For Strategic Basing proposals with construction or real property repair requirements

expected to exceed the minimum threshold for a comparative analysis, an economic analysis

will be performed as part of the Site Activation Task Force process. (T-2).

AFI65-501 29 OCTOBER 2018 15

2.10.4. See AFMAN 65-506 for additional guidance on Real Property Construction and

Repair to include the design phase of construction.

16 AFI65-501 29 OCTOBER 2018

Chapter 3

ESTIMATING MANPOWER COSTS.

3.1. Introduction

3.1.1. This chapter provides guidance on DoDI 7041.04, Estimating and Comparing the Full

Costs of Civilian and Active Duty Military Manpower and Contract Support, which establishes

business rules to be used in estimating and comparing the full costs of DoD manpower (military

and civilian) and contract support. It applies to all Air Force appropriated fund activities. The

full costs of manpower include current and deferred compensation costs paid in cash and in-

kind, as well as non-compensation costs.

3.2. Costs to Include

3.2.1. Manpower Costs. When answering questions about the costs of manpower for a

specific unit, organization, function, mission, or defense acquisition program, analysts should

report the full costs of both military and civilian DoD manpower. For example, analysts should

account for the full costs of manpower when developing independent cost estimates for defense

acquisition programs. Manpower cost estimates normally address costs to the DoD. However,

in certain cases, analysts may be asked to report full manpower costs to the Federal

Government. The business rules in DoDI 7041.04 address both kinds of requests.

3.2.2. Economic Analysis. Economic analyses are intended to assist with decision making.

Therefore, Air Force analysts should follow the principles contained within DoDI 7041.04,

while continuing to apply only those burdened costs that are applicable to the decision at hand

and for which data exists. All costs that are incremental (i.e., marginal) to the decision at hand

should be included in the analysis.

3.2.3. Program and Budget Submissions. Policies and procedures for calculating DoD

civilian and military manpower costs for programming and budgeting purposes are established

through separate guidance issued by the Under Secretary of Defense (Comptroller), Title 10,

USC Section 2461, DoD, and the Director of Cost Assessment and Program Evaluation, as

part of the annual integrated program and budget review process. The DoD composite rates,

as published by the Under Secretary of Defense (Comptroller), typically directed for use to

calculate manpower costs for program and budget submissions do not account for the full costs

of military or DoD civilian personnel.

JOHN P. ROTH

Assistant Secretary of the Air Force

(Financial Management and Comptroller)

AFI65-501 29 OCTOBER 2018 17

Attachment 1

GLOSSARY OF REFERENCES AND SUPPORTING INFORMATION

References

AFI 33-360, Publications and Forms Management

AFMAN 33-363, Management of Records

AFPD 65-5, Cost and Economics, 5 Aug 08 (certified current 3 Oct 2013)

DoDI 7041.03, Economic Analysis for Decision-making, 9 Sep 2015, Change 1, 2 Oct 2017

AFMAN 65-506, Economic Analysis, 29 Aug 2011

40 USC Section 1401 et seq, Clinger-Cohen Act of 1996

DoDI 5000.02, Operation of the Defense Acquisition System, 7 Jan 2015

DoDI 5000.75, Business Systems Requirements and Acquisition, 2 Feb 2017

DoDI 5000.74, Defense Acquisition of Services, 5 Jan 2016, Change 1, 5 Oct 2017

AFI 65-107, Nonappropriated Funds Financial Management Oversight Responsibilities, 13 Jun

2018

DoDFMR Volume 2B, Budget Formulation and Presentation, Nov 2017

10 USC Section 2811

10 USC Section 2337

AFPAM 63-123, Product Support Business Case Analysis, 1 Jun 2017

OAS Analysis of Alternatives Handbook, http://afacpo.com/AQDocs/AoAHandbook.pdf

10 USC Section 2461

DoDI 7041.04, Estimating and Comparing the Full Costs of Civilian and Active Duty Military

Manpower and Contract Support, 3 Jul 2013

Adopted Forms

AF Form 847, Recommendation for Change of Publication

DoD Form 1391, Military Construction Project Data

Prescribed Forms

None

Abbreviations and Acronyms

AF—Air Force

AFI—Air Force Instruction

AFMAN—Air Force Manual

AFPAM—Air Force Pamphlet

18 AFI65-501 29 OCTOBER 2018

AFPD—Air Force Policy Directive

DoD—Department of Defense

DoDFMR—Department of Defense Financial Management Regulation

DoDI—Department of Defense Instruction

FM—Financial Management

NIST—National Institute of Standards and Technology

NISTIR—National Institute of Standards and Technology Interagency Report

OAS—Office of Aerospace Studies

OMB—Office of Management and Budget

USC—United States Code

Terms

Acquisition Category (ACAT)—Categories established to facilitate decentralized decision

making and execution and compliance with statutorily imposed requirements. The categories

determine the level of review, decision authority, and applicable procedures.

Alternative—An approach or program that is another possible way of fulfilling an objective,

mission, or requirement. The status quo, and/or an upgrade to the status quo, is usually included

as an alternative to a proposed course of action.

Analysis of Alternatives—Assessment of potential materiel solutions to satisfy validated

capability needs. It focuses on identification and analysis of alternatives, Measures of

Effectiveness, cost, schedule, concepts of operations, and overall risk, including the sensitivity of

each alternative to possible changes in key assumptions or variables. An Analysis of Alternatives

is a specialized version of a comparative analysis.

Benefits—Results expected in return for costs incurred under a specific alternative. It includes

measures of utility, effectiveness, and performance. Benefits focus on the purpose and the

objective of a project. These may be quantitative or qualitative.

Business Case Analysis—See Comparative Analysis.

Business System—A business system is an information systems that is operated by, for, or on

behalf of the DoD, including: financial systems, financial data feeder systems, contracting systems,

logistics systems, planning and budgeting systems, installations management systems, human

resources management systems, and training and readiness systems.

Capital Investment Program—The goal of the Capital Investment Program within the Defense

Business Operations Fund (DBOF) is to establish a capability for reinvestment in the infrastructure

of business areas in order to facilitate mid and long term cost reductions.

Certificate of Satisfactory Comparative Analysis—A cover sheet on the comparative analysis

that provides verification that the analysis has been coordinated and adheres to the requirements

in this AFI and AFMAN 65-506.

AFI65-501 29 OCTOBER 2018 19

Community Partnership—Either a Public-Public Partnership or a Public-Private Partnership that

enables the mutually beneficial provision of goods or services and the leveraging of resources and

best practices to achieve cost efficiencies or risk reductions.

Comparative Analysis—An impartial analysis that uses the economic analysis approach to

support a decision on how to allocate scarce resources. A comparative analysis identifies

alternative methods of solving a problem or accomplishing a stated objective, and compares them

by weighing the costs, benefits, and uncertainties (including risks) for each alternative.

Comparative analyses are referred to by a variety of names including, but not limited to, economic

analysis, business case analysis, cost benefit analysis, lease vs. purchase, and analysis of

alternatives.

Comparative Analysis Product—The document produced as a result of performing a

comparative analysis. It identifies the competing alternatives for solving a problem or

accomplishing a stated objective, and presents the costs, benefits and uncertainties (including

risks) for each alternative. It interprets the results of the comparative analysis and presents

arguments in favor of and against each alternative. It can include a recommendation, but one is

not mandatory.

Constant—Year Dollar – The value or purchasing power of a dollar in any specific year, which

may or may not be the Base Year. Constant-Year Dollars do not contain any adjustments for

inflationary changes that occurred or are forecast to occur outside of the Base Year. Constant-

Year Dollars are not influenced by Outlay Profiles (Expenditure Patterns). Also known as Real

Dollars.

Cost Benefit Analysis—See Comparative Analysis.

Economic Analysis—A systematic approach to the problem of choosing how to use scarce

resources to meet a given objective. It includes consideration of costs, benefits, and uncertainties

(including risks) associated with all alternatives under consideration. At times, the term economic

analysis is used in reference to the product/document that results from applying the economic

analysis systematic approach. This resulting document is also referred to as a comparative

analysis.

Economic Analysis Document—See Comparative Analysis Product.

Future Years Defense Program—A DoD database and internal accounting system that

summarizes forces and resources associated with programs approved by the Secretary of Defense

(SECDEF). Its three parts are the organizations affected, appropriations accounts (Research,

Development, Test, and Evaluation (RDT&E); Operation and Maintenance (O&M); etc.), and the

11 major force programs (strategic forces, mobility forces, Research and Development (R&D),

etc.).

Investment Costs—Costs associated with the acquisition of equipment, real property,

nonrecurring services, nonrecurring operations and maintenance (start- up) costs, and other one-

time outlays.

Lease-Purchase Analysis—An analysis of the decision whether to lease or purchase the services

of an asset. After the decision to acquire the services of an asset has been made, there may be a

need to analyze the decision whether to lease or purchase those services.

20 AFI65-501 29 OCTOBER 2018

Life-Cycle Sustainment Plan—Documents life cycle sustainment planning initialized during the

Materiel Solution Analysis (MSA) Phase and the evolution of sustainment planning through the

other acquisition phases and throughout the system’s life cycle to disposal. The LCSP addresses

how the Program Manager (PM) and other organizations will acquire and maintain oversight of

the fielded system.

Product Support Business Case Analysis—The business case analysis required by 10 USC

Section 2337.

Resources—Any and all factors used in producing a good or service. This includes, but is not

limited to, human resources/manpower, natural resources, capital goods (durable equipment, such

as assembly line equipment, facilities, vehicles, aircraft), and disposable items (e.g., fuel,

lubricants).

Risk—The probability of a loss or injury.

Scarce (Scarcity)—When needs and wants exceed the resources available, requiring people to

make resource allocation decisions. Almost all resources are scarce.

Site Action Task Force (SATAF)—A team of MAJCOM functional experts chartered to travel

to an installation to identify all the actions necessary to ensure a beddown at that installation is

successful. SATAFs are led by a MAJCOM, and provide periodic, on-scene assistance to unit-

level agencies to accomplish a program objective. It employs appropriate members of the

MAJCOM, staff and may include HAF functionals. The SATAF structure is comprised of

headquarters team members and representation from the affected unit(s), which are organized into

functional working groups. Each working group has an assigned chairperson, who functions under

the auspices of the SATAF Team Chief. A SATAF may be convened to support bringing a

program, system, equipment and/or site to operational readiness. SATAFs are also conducted to

facilitate unit activations, inactivations, relocations, and conversions from one weapons system to

another.

Strategic Basing—The AF Strategic Basing Process provides an enterprise-wide transparent,

defendable, and repeatable process for decision making to ensure all strategic basing actions

involving AF units and missions support AF mission requirements and comply with all applicable

environmental guidance. SAF/IEIB is the AF single point of contact (POC) and clearinghouse for

all strategic basing processes and actions.

Then-Year Dollar—Reflects the amount of funding needed (expected to be needed) when the

expenditure for goods and services were (are expected to be) made. All Planning, Programming,

Budgeting, and Execution System (PPBES) documents use Then-Year Dollars to properly reflect

the Total Obligation Authority (TOA) that must be appropriated during a specific fiscal year if

sufficient funds are to be available to pay for the goods and services when received. For Air Force

Comptroller purposes, Then-Year Dollars are identical to current dollars; they are known as

nominal or budget dollars. If Then-Year Dollars are written with a specific year (e.g., TY11$),

then those dollars reflect the amount of funding needed if the funds for all goods and services were

obligated in the year specified (e.g., FY 2011 for TY11$).

Uncertainty—The indefiniteness about the outcome of a situation. Uncertainty includes both

risks (i.e., the probability of a loss or injury) and opportunities (i.e., favorable events or outcomes).

AFI65-501 29 OCTOBER 2018 21

Working Capital Fund—Revolving funds within DoD that finance organizations that are

intended to operate like commercial businesses. WCF business units finance their operations with

cash from the revolving fund; the revolving fund is then replenished by payments from the business

units’ customers.

22 AFI65-501 29 OCTOBER 2018

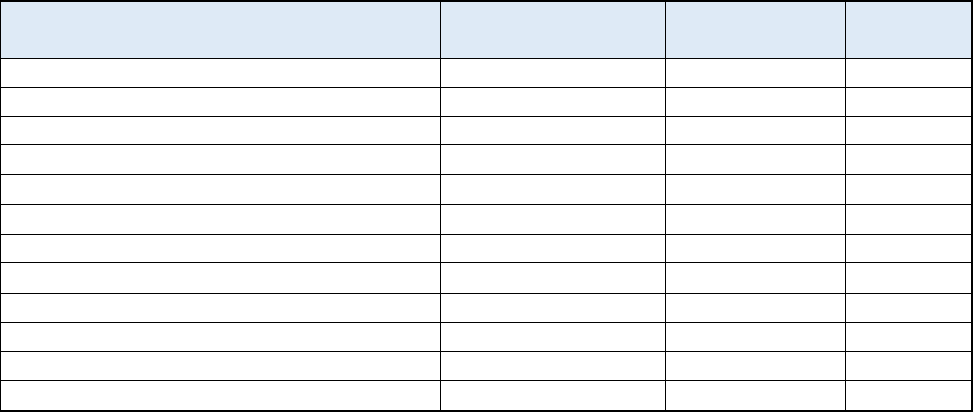

Attachment 2

MATRIX OF RESPONSIBILITIES FOR COMPARATIVE ANALYSES INVOLVING

REAL PROPERTY CONSTRUCTION AND REPAIR OR MILITARY FAMILY

HOUSING AS A POSSIBLE COA.

The matrix below provides a list of responsibilities. The most effective comparative analyses

will be developed as a close collaboration between the user, the engineer, and the financial

analyst. Some of the tasks have multiple Offices of Primary Responsibility (OPRs) and Offices

of Collateral Responsibility (OCRs). In these cases, the asterisks indicate the division of

responsibilities within the task. The responsibilities in the matrix are for both comparative

analyses and waivers to comparative analyses.

TASK

FINANCIAL

MANAGEMENT*

ENGINEER**

USER***

Identify Need

OPR

Determine if Analysis Required

OPR

OCR

OPR

Initiate Analysis

OPR

Develop Objective

OCR

OCR

OPR

Develop Scope

OCR

OPR

OPR

Develop Ground Rules and Assumptions

OPR

OPR

OPR

Develop Alternatives

OCR

OPR

OPR

Identify and Collect Required Data

OPR

OPR

OCR

Data Analysis

OPR

Interpret Results

OPR

OCR

OCR

Documentation

OPR

OPR

OCR

Certification

OPR

OCR

OCR

NOTE: Where multiple OCRs and OPRs are listed for a task:

* Financial Management is responsible for cost and economic aspects (compliance, data, etc.)

** Civil Engineering is responsible for engineering aspects (alternatives, data, etc.)

*** The user is responsible for non-real property aspects (alternatives, data, etc.)

FM retains overall responsibility for the Comparative Analysis and for ensuring the analysis is

performed in accordance with this AFI and with AFMAN 65-506.